Bare Metal Banking

The Neobank Moment

Between December 2025 and March 2026:

Coinbase filed for a national trust charter.

NuBank received conditional approval from the OCC to establish a US national bank.

PayPal applied to create PayPal Bank

Revolut, after years of regulatory limbo, obtained its full UK banking license and is pursuing a US national banking charter.

Kraken became the first crypto company to secure a Fed master account.

Four of the world’s largest fintechs made the same bet at the same time.

For the past 15 years, the story of neobanking has been the unbundling of the financial services stack. In the US, the playbook was simple: excel at one thing and hand off the regulatory complexity to sponsor banks. SoFi excelled at student loans, PayPal at online payments, Kraken and Coinbase at crypto trading. Now they are rebundling and going after the full stack.

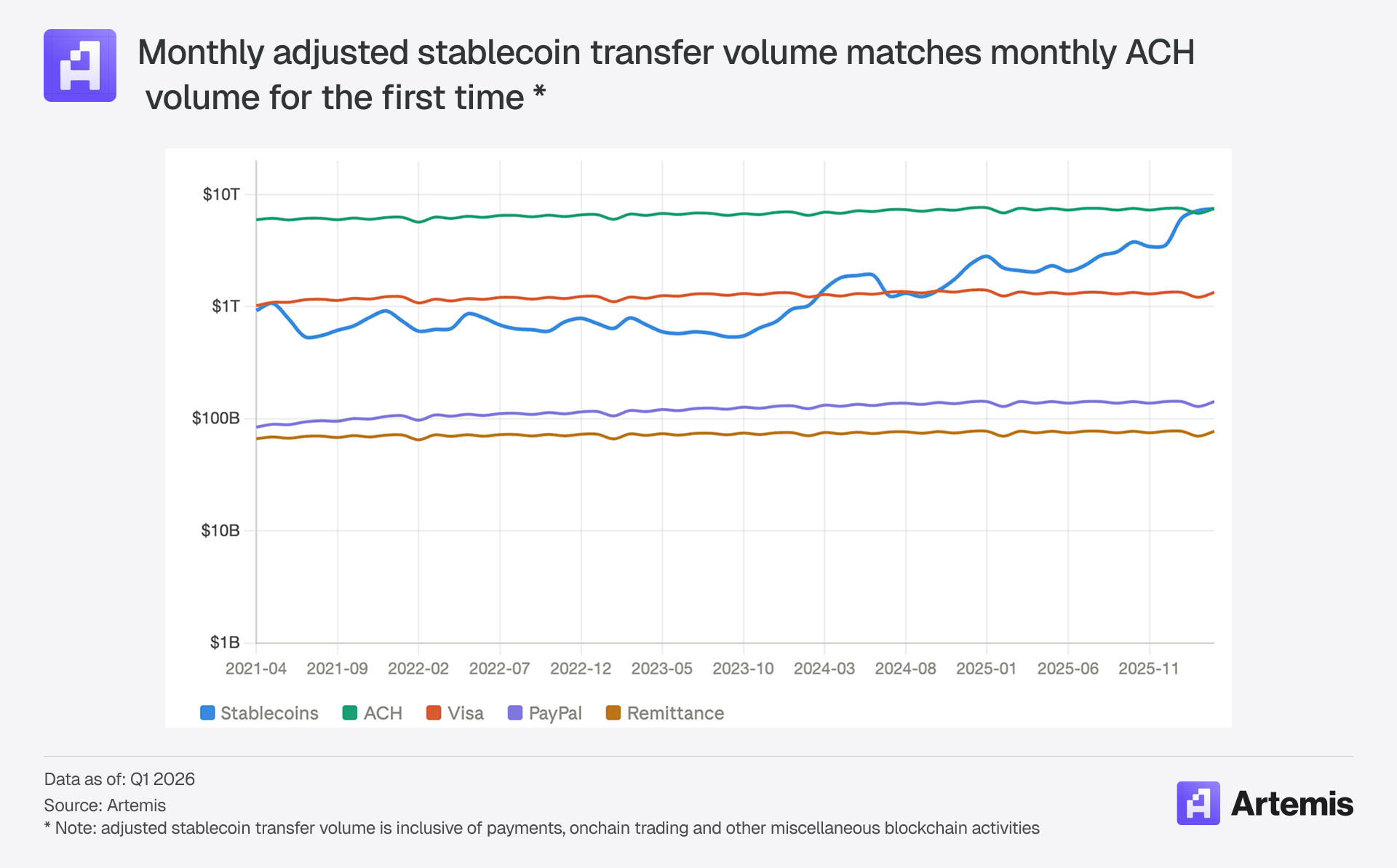

Meanwhile, a second shift is underway. In 2025, there was $33 trillion in adjusted stablecoin transfer volume on public blockchains, rivaling major payment systems like ACH and Visa (Artemis). Decentralized finance lending protocols like Aave have surpassed $1 trillion in cumulative loans originated. NYSE, NASDAQ, and CME are partnering with crypto firms to build tokenization infrastructure.

The neobank stack is undergoing a dual compression that is changing what it means to be a bank. From the top, neobanks are vertically integrating by acquiring charters, and collapsing the middleware layers that have historically collected rent. From the bottom, public blockchains are exposing permissionless financial plumbing that lets any developer build money movement and financial products without a banking relationship. The neobanks that own both the legacy stack and the emergent blockchain stack will define the next decade of finance.

In our 2030 Digital Finance Manifesto, we introduced Steven, a 25-year-old whose entire financial life runs through a neobank: investing, saving, earning yield, receiving payments, and managing credit, all in one place. We identified neobanks as one of five pillars of digital finance. This is our deep dive into that pillar.

The first trillion-dollar standalone neobank is within reach.

The Stack

What is a neobank?

A neobank offers banking products without being a bank (at least historically). They partner with sponsor banks for deposits, FDIC insurance, and payment network access, and build the customer-facing product on top. This lets them move fast, but it also means the most valuable economics of the banking relationship sit with the sponsor, not the neobank.

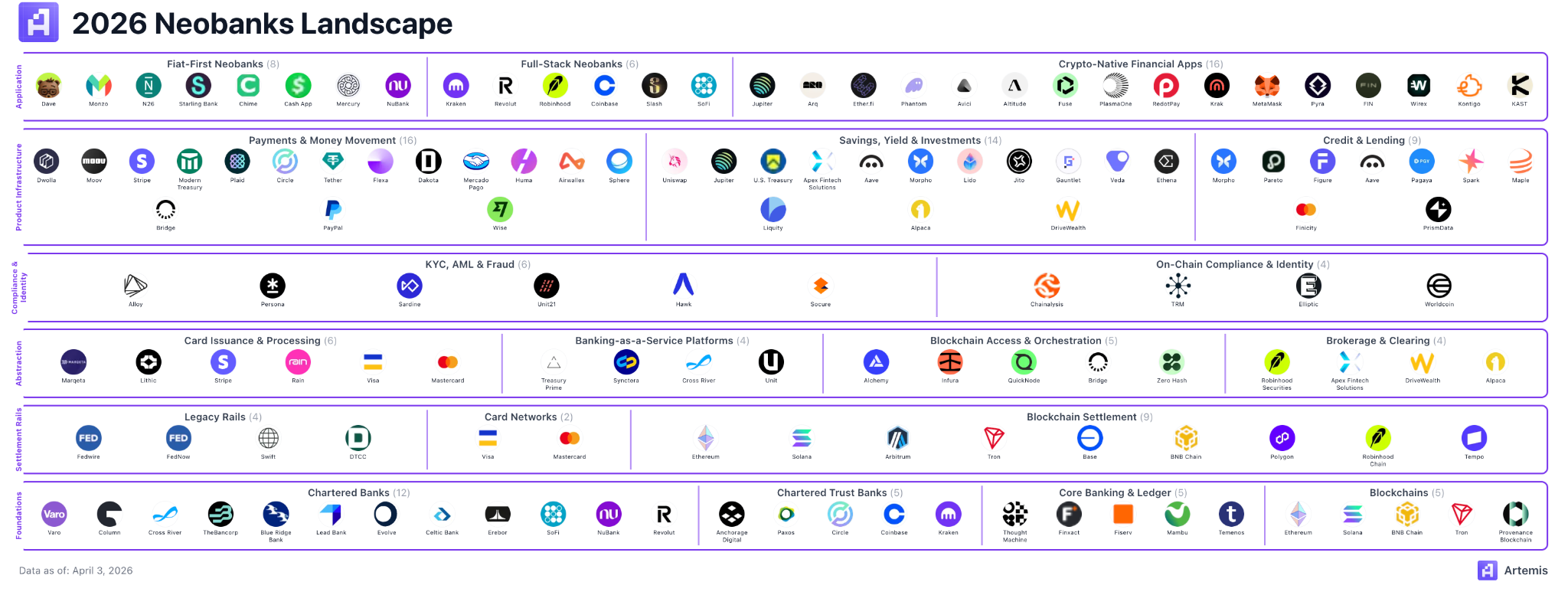

Every existing legacy bank is vertically integrated across the stack, or at least significant portions of it. Neobanks stripped it apart and rebuilt each component on modern infrastructure. Marqeta focused on card issuance, Alloy on KYC, and Plaid on account connectivity. This created a modular ecosystem, where new players could pick and choose their stack as if they were picking ingredients off a shelf. We’ll break down the stack into 6 layers:

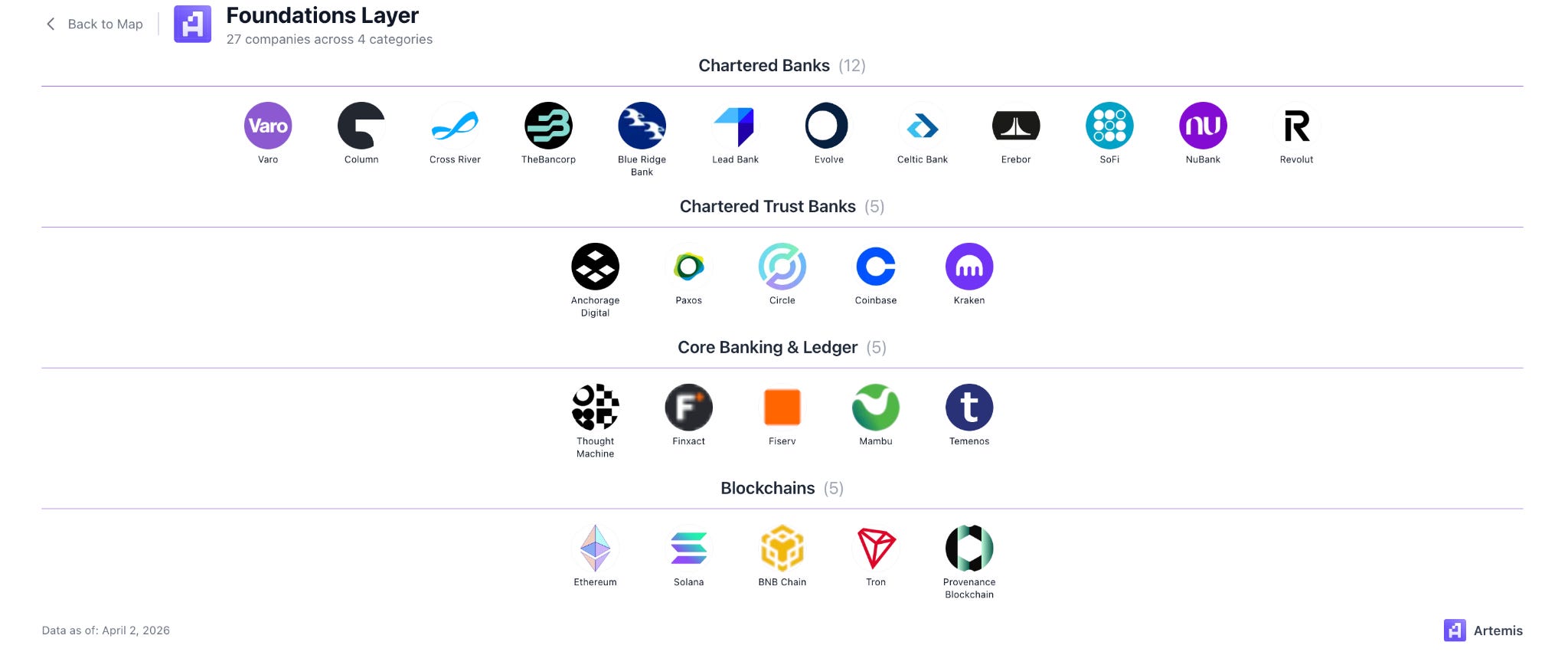

Layer 1: Foundations

This layer is the bedrock on which everything else is built. This is the layer that holds assets and does the ledgering. In the legacy financial system, companies in this layer follow the most stringent regulations, but they also have access to the very core of the financial system: the Fed and the payment networks. In the modern stack, blockchains play this role as the core ledgering system that holds financial assets.

Traditionally, a neobank seeking to take on customer deposits would partner with a real chartered bank, known as a sponsor bank. The sponsor manages the regulatory overhead, the relationship with the FDIC for deposit insurance, as well as access to payment networks. Since the deposits sit on the sponsor bank’s balance sheet, they can use them to fund loans and generate net interest income. That’s interest income neobanks are foregoing as rent.

Now, the biggest neobanks are bypassing sponsor banks entirely and going after their own full banking charter in order to own the economics themselves. At a certain scale, the rental relationship stops making economic sense.

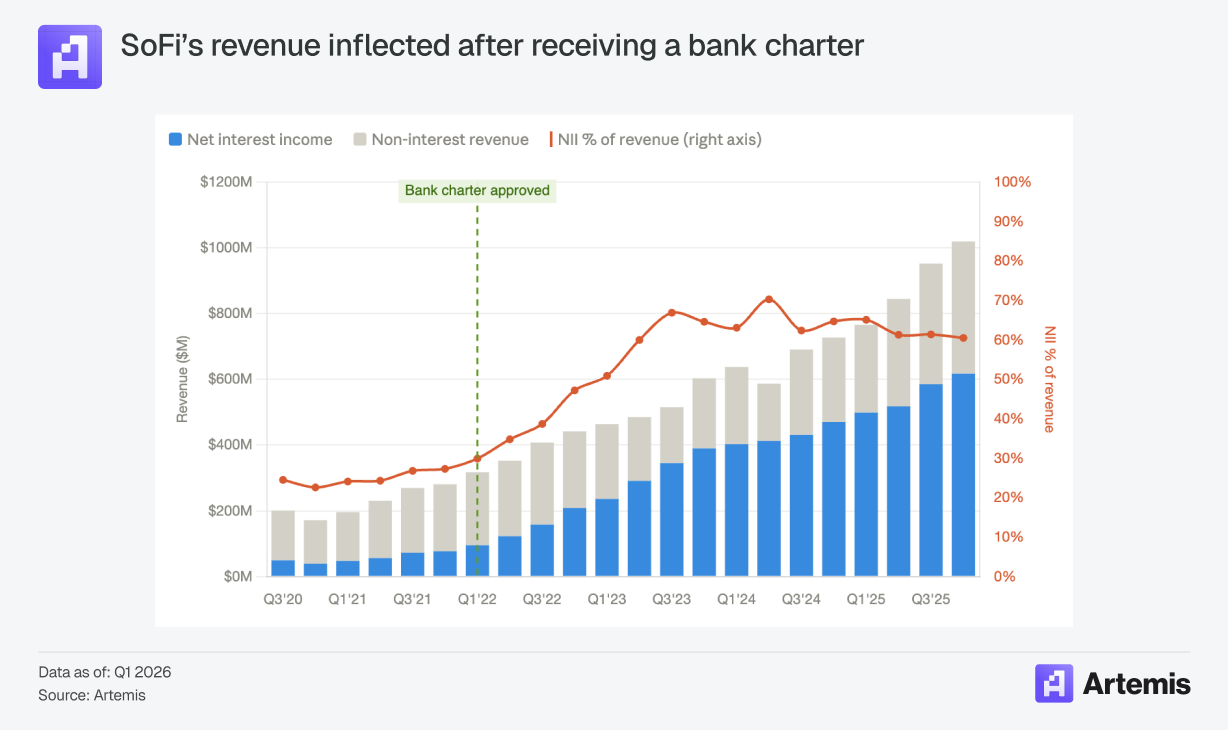

NuBank, already a chartered bank in Brazil, received conditional approval for a US national banking charter by the OCC in January 2026, while Revolut applied for a full banking charter in March 2026 (immediately after receiving its UK banking charter). SoFi has been a chartered bank since 2022 and the effect on its business has been dramatic, growing quarterly net interest income from $94.9M to $617M in four years.

Crypto companies are also pushing into this layer: Kraken has a trust charter and a Fed master account, and Coinbase is going after its own trust charter. As Jason Mikula of Fintech Business Weekly put it: “what it means to be a bank is rapidly changing” (Substack).

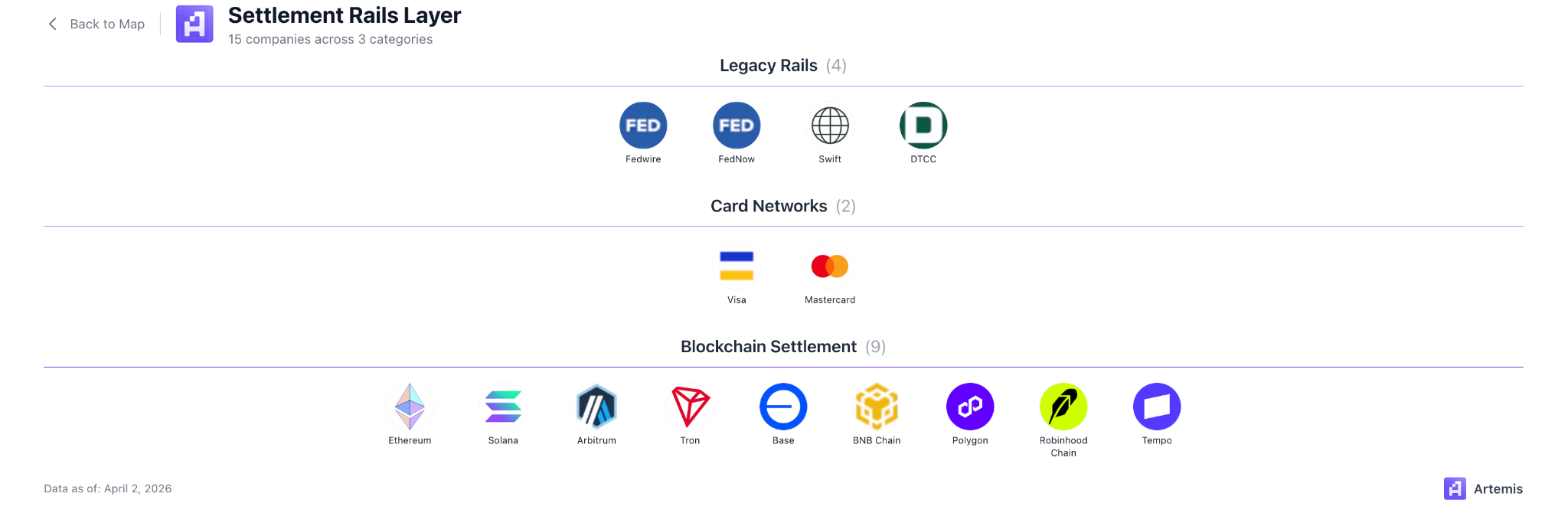

Layer 2: Settlement Rails

This layer glues the foundations together. These rails enable banks to coordinate and settle assets between them, and are where real value movement happens. In the US, there are several key systems that settle and move value:

FedWire, a real-time gross settlement system (only during business hours)

FedNow, a new, 24/7/365 public-sector instant payment system

DTCC, infrastructure for securities clearing, trading, settlement and more

Swift, a messaging system for global inter-bank payments

Every one of these networks is gated. Connecting to FedWire, requires having a Master Account at the Federal Reserve, which means you have to be a chartered bank or trust. Touching the ACH network, requires being a member of NACHA, which requires being a federally insured depository institution.

Public blockchains show up again in this layer. They are the first financial rails in history that are public and permissionless, allowing any developer to plug into them. If you want to send $10,000 worth of USDC on Ethereum, you call a smart contract function. You don’t need a charter or a sponsor bank. Modern blockchains settle in milliseconds, never shut down, and charge sub-cent fees.

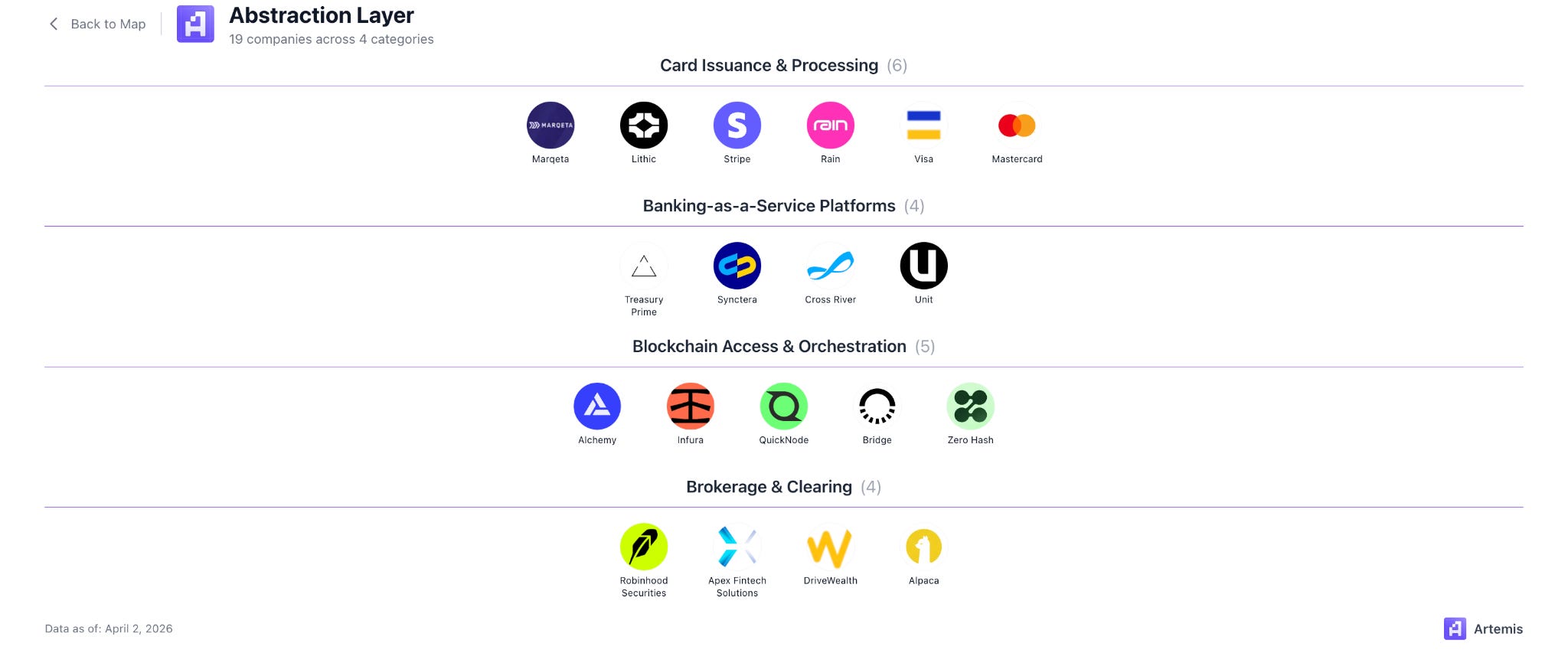

Layer 3: Abstraction

The raw rails are where value moves, but they are complicated and often gated. Most companies don’t want to get bank charters in order to integrate directly with Fedwire, and they don’t want to manage Ethereum node infrastructure. The abstraction layer exists to solve this. These are the companies that sit on top of the rails and make them usable.

For card payments: Marqeta and Lithic provide card issuing infrastructure. You tell them what kind of card you want, and they handle the Visa/Mastercard integration. Stripe and Adyen offer a single interface that abstracts away the complexity of moving money across ACH, card networks, and more.

For blockchains: Bridge (acquired by Stripe for $1.1 billion in February 2025) lets businesses accept stablecoin payments without managing wallets. Zero Hash provides trading, custody, and settlement infrastructure across 80+ digital assets. Alchemy, Infura, and QuickNode all offer APIs and tools that enable developers to build on blockchains without worrying about managing nodes.

Unit, Treasury Prime, and Synctera sit under Banking-as-a-Service, middleware that connects non-bank fintechs to sponsor banks. A now infamous BaaS provider, Synapse, went bankrupt in April of 2024 after internal ledgers failed to reconcile with their partner bank ledgers, resulting in up to $95 million unaccounted for or frozen across more than 100,000 customers (banking.senate.gov). This incident didn’t kill BaaS, but it did show the limits of the model and led to increased regulation in this part of the stack such as the “Synapse Rule” (American Banker). It signaled to major neobanks that they shouldn’t trust their entire deposit base to a middleware layer out of their control.

Brokerage and clearing firms like Apex, Alpaca and Drivewealth enable neobanks to offer securities trading without having to build their own clearing and settlement infrastructure. For example, Coinbase and Cash App use Apex, while Revolut uses Drivewealth. One logo stands out here: Robinhood. They decided to vertically integrate and own the economics instead of paying a fee to a third party provider for a service so core to their business.

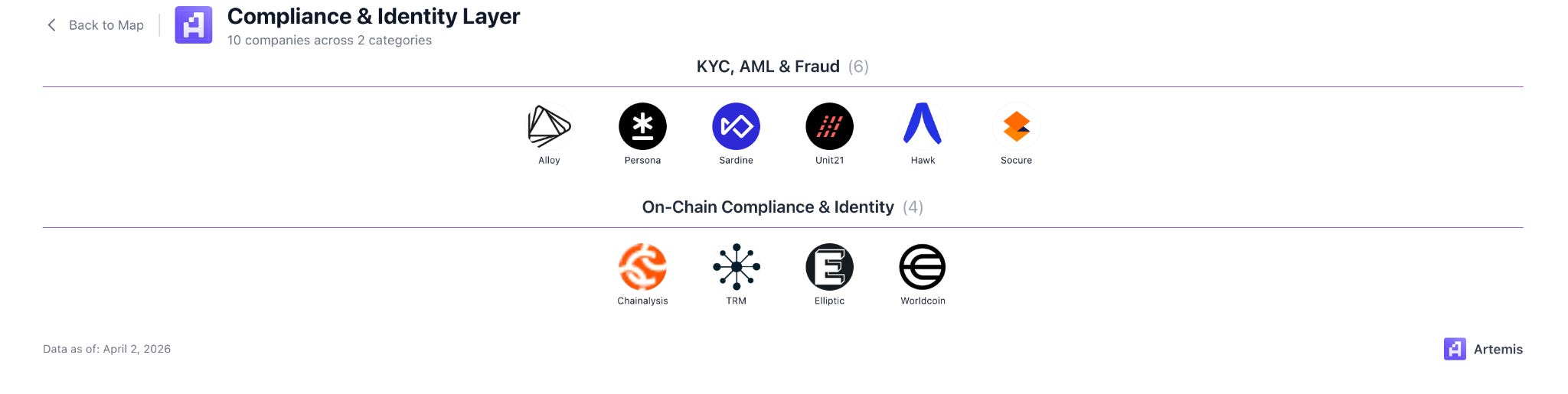

Layer 4: Compliance and Identity

Every financial transaction requires knowing who’s on the other end. KYC (know your customer), AML (anti-money laundering), and fraud prevention form an entire industry.

On the traditional side, Alloy, Sardine, Persona and others provide identity verification, transaction monitoring, and fraud detection. These companies sit between the application and the financial products, ensuring every neobank customer is who they say they are.

On the blockchain side, firms trace onchain transactions to flag illicit activity. As stablecoins become more regulated, onchain compliance becomes more important — you need to know that the USDC flowing through your neobank didn’t originate from a North Korean wallet.

This layer isn’t where the value accrues, but these firms provide a critical service to their clients, ensuring a more safe, compliant and trustworthy financial system.

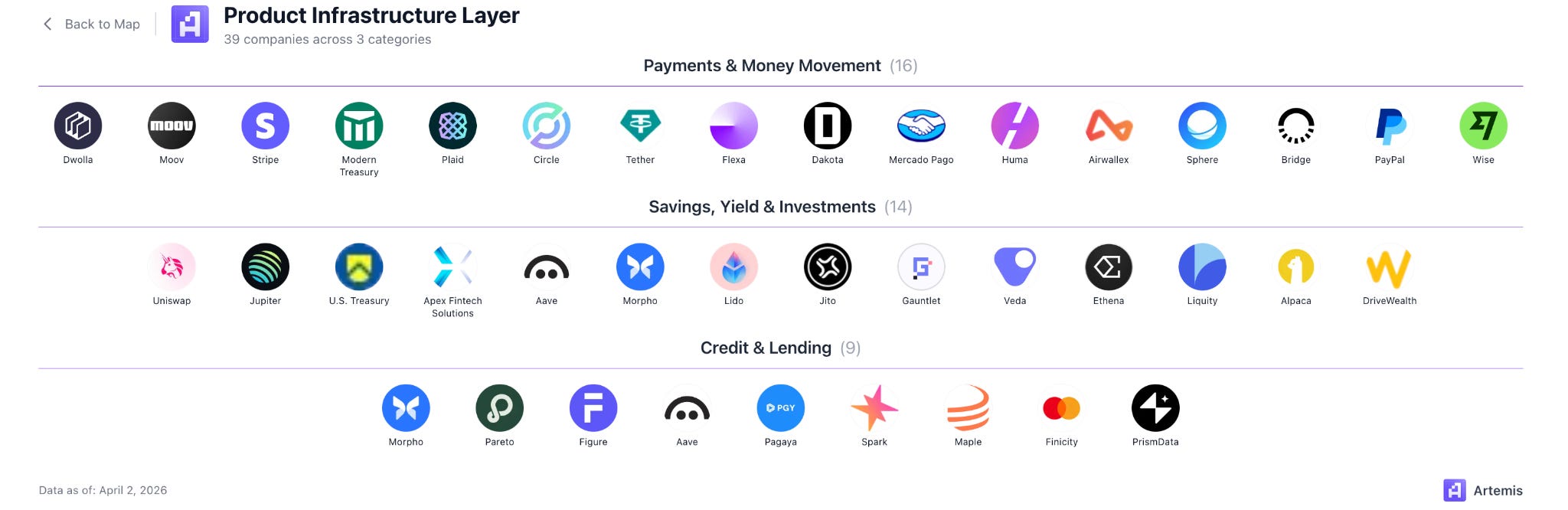

Layer 5: Product Infrastructure

This is the layer that answers the question: what products can neobanks plug into so they don’t have to build them from scratch?

Money movement companies allow neobanks to embed payments and other money movement features directly into their products. For example, a neobank looking to issue a stablecoin would use Bridge, while a neobank looking to offer international transfers could work with Airwallex or Sphere.

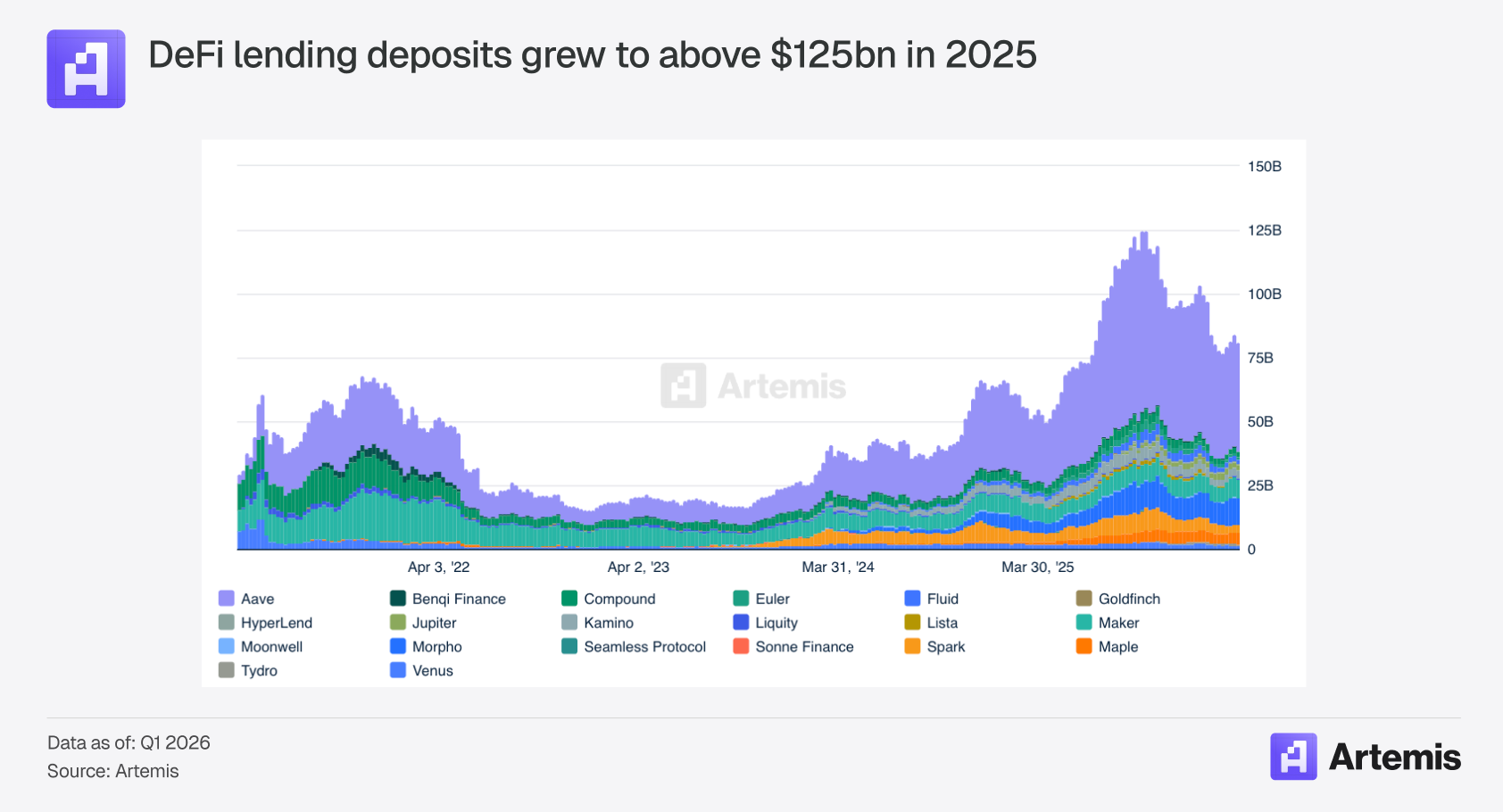

Savings, Yield and Investment is where DeFi shines. Neobanks can use Aave or Morpho on the backend to generate yield, no loanbook required. Or, they could offer a yield via staking products like Lido or Jito, which expose users to the native issuance and fee rewards of the Ethereum and Solana networks. Uniswap and Jupiter provide APIs enabling trading of thousands of assets including tokens, perps, and soon, RWAs. The US Treasury shows up in this layer as they are the issuers of risk-free rate assets.

Lastly, DeFi protocols like Aave and Morpho don’t just offer yield, they allow users to borrow against their capital. Coinbase launched crypto backed loans using Morpho and bitcoin backed mortgages with Better. Maple offers institutional grade borrowing and lending facilities. Figure offers white label lending infrastructure that apps and partners can plug into.

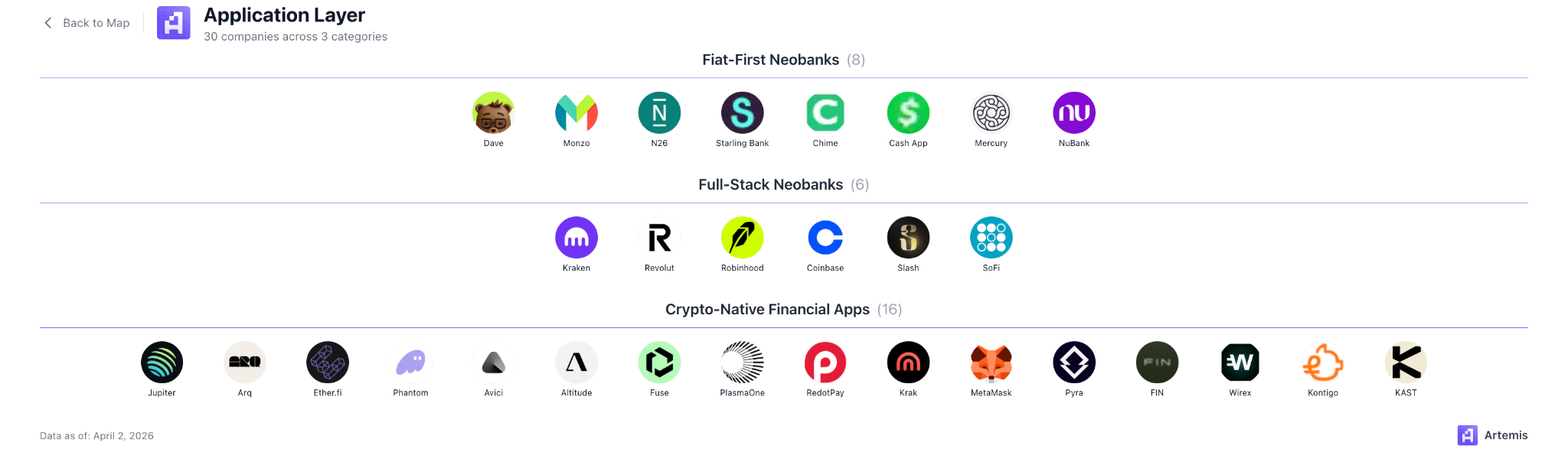

Layer 6: The Application Layer

This is where neobanks thrive and where the customer actually interfaces with the stack described above. The application layer breaks loosely into three categories, though the lines are blurring fast.

The Full-Stack Neobanks are Revolut, Robinhood, Coinbase, Kraken, SoFi, and Slash. These are all platforms that offer a suite of products that spans both the traditional financial stack and the blockchain stack. SoFi has a banking charter and is now issuing its own stablecoin SoFiUSD. Coinbase and Kraken each have their own public blockchain and are integrating more deeply with the US financial system via charters and Fed master accounts.

In the Fiat-First sector we have Nubank, Chime, Monzo, N26, Starling, Dave, and Mercury. These started from traditional banking products and are expanding through traditional rails and products.

Lastly, there are the Crypto-Native Financial Apps like EtherFi, RedotPay, Kast, and Phantom. These are firms born from public, permissionless blockchains, that take advantage of the lower operating costs that stablecoins provide. They integrate with onchain financial products, allowing users to pay in stablecoins, access DeFi yields, and trade onchain assets.

The pattern emerging across all three sectors is rebundling. Every successful neobank started with an initial wedge, and is expanding toward a single surface that handles a user’s entire financial life. The winning app is the one that is able to offer both the best of traditional banking and the emerging global onchain economy.

Business Models

Renting the Stack

Under the traditional model, a neobank partners with a sponsor bank and issues cards through a program manager, which structurally limits its ability to capture core banking economics. A traditional neobank’s primary revenue source is interchange, the 1-2% fee merchants pay on card transactions. The neobank may add a subscription tier (Chime’s SpotMe, Dave’s membership fee) or earn some referral fees, but interchange is the core. This business model allows neobanks to get off the ground, but it doesn’t scale into high-margin, durable businesses. Interchange is a thin margin that scales linearly with transaction volume. The most lucrative parts of the financial relationship are the net interest margin (NIM) on deposits, the lending income, and the investment yield. All of those economics flow to the sponsor bank. The neobank has the customer relationship, but not the balance sheet or the economics.

Owning the Stack

The economics change significantly when a neobank gets its own charter. A chartered bank can take customer deposits and use them to fund loans, or invest in interest-bearing assets, while keeping the spread. A traditional incumbent bank today typically offers less than 0.5% yield on savings accounts while making 6% on a mortgage and pocketing the 5.5% difference (FDIC). Since obtaining its bank charter in 2022, SoFi has grown net interest income tenfold, from $252M in 2021, to $2.2B in 2025 (Artemis).

A chartered bank also gains access to the core payment and settlement systems in the US. It connects directly to Fedwire, ACH, FedNow, avoiding per-transaction fees that intermediaries typically charge.

Stablecoin-First Banks

Neobanks that build using blockchains and stablecoins as the backend will have a few ways to generate revenue.

The first and most powerful is generating net interest income, a model reserved for stablecoin issuers like Circle, or SoFi. The second is interchange. All neobanks will have cards, and they will collect interchange on payments. Cards are a consumer’s favorite payment modality, and that isn’t changing any time soon. Stablecoin-first neobanks can also charge fees on trades, or take a portion of the DeFi yield they generate on the backend. The design space for a stablecoin neobank is wide open, which is why hundreds of millions of funding dollars have poured into backing startups in the space in the past year.

The Blockchain Thesis

The Stablecoin Inflection

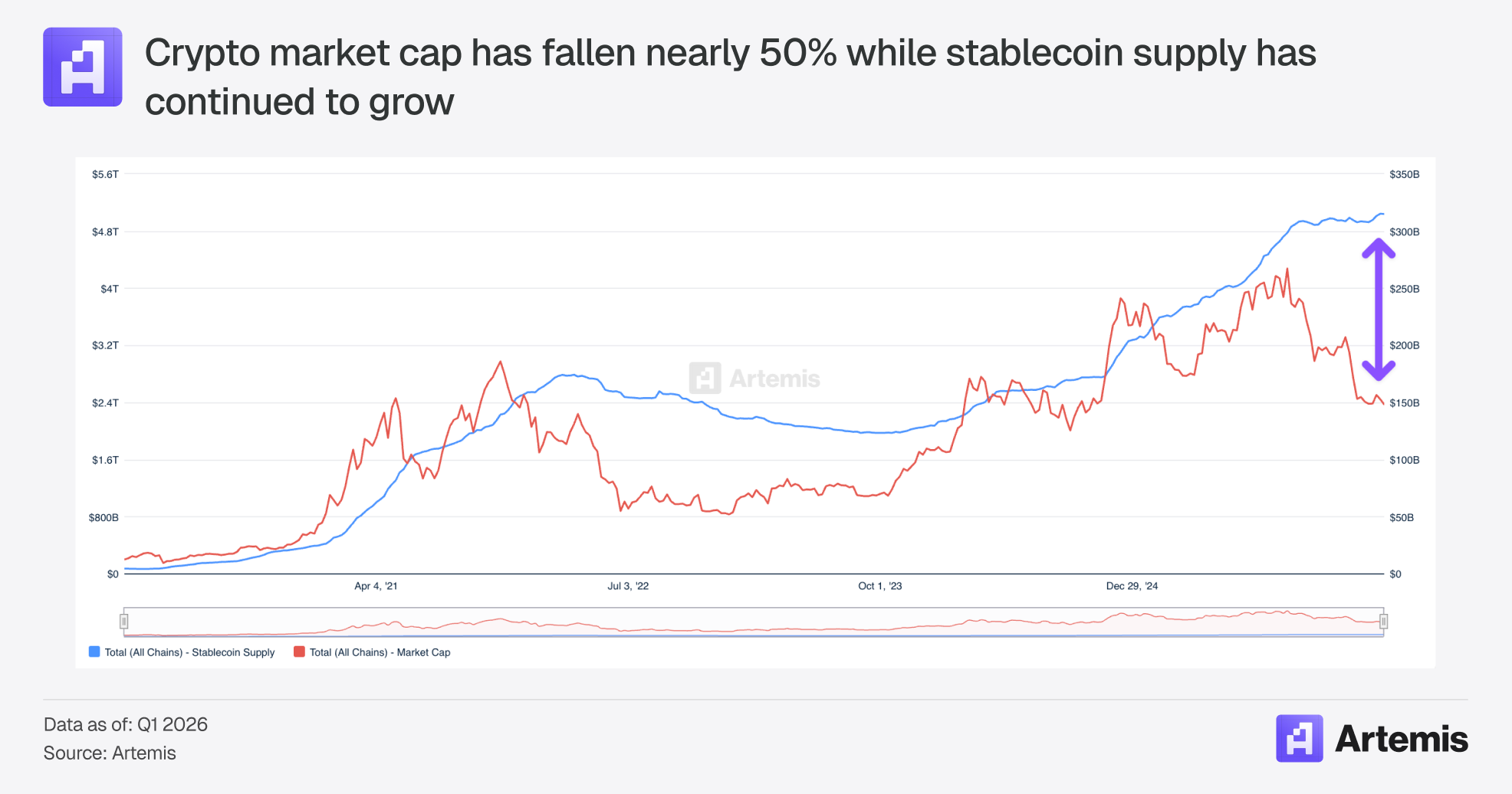

Stablecoins are at an inflection point. They are the first use case of blockchains that has found non-speculative product market fit. The proof is in the numbers: stablecoin payment volumes doubled in 2025 to $390 billion annualized, with key sectors like B2B payments growing 733% YoY (Artemis, McKinsey). While stablecoin payments still represent < 1% market penetration in key payment verticals, the growth is undeniable. 2025 was also a watershed year for stablecoins from a regulatory perspective. Passage of the GENIUS Act provided stablecoin issuers a regulatory framework for operating in the US. The result is that even though crypto market cap has fallen about 50% since 2025 highs, stablecoin supply has actually continued to grow, reaching $313bn by March 2026 (Artemis).

Stablecoins bring dollars onto blockchains. Those dollars will seek to be productive, flowing into decentralized finance protocols to earn yield or provide liquidity.

For years, decentralized finance was the territory of crypto-natives exploring the frontier of the onchain economy. While the world looked the other way, they created composable building blocks for global financial products. Aave has facilitated >$1 trillion in loans, making it the de facto place to borrow against your crypto. Morpho has built the infrastructure for curated, risk-isolated lending vaults that have attracted institutional capital, including a partnership with Apollo Global. Yield-bearing stablecoins like Sky’s sUSDS, Ondo’s USDY, and Ethena’s sUSDe grew 80% in 2025, outpacing growth of non-yield-bearing stablecoins (Artemis). These tokens allow holders to earn yield generated by lending activities, treasury yields or trading strategies.

Neobanks that build using stablecoins instantly get a vast set of financial products that they can simply plug into with a few smart contract calls. Public, open source protocols mean developers don’t have to negotiate with anyone, or sign any contracts to integrate a product. This creates a major opportunity for builders attacking the stack from below.

Where This Is All Going: The Neobank of 2030

Charter Convergence

In the next 5 years, any neobank hoping to win at scale will either hold its own banking charter or be in the process of acquiring one. Beyond a certain scale, the economic gains far outweigh the risks(recall what happened to Synapse). More importantly, the regulatory environment has been constructive in recent years. The OCC is approving bank/trust charters (NuBank), the Fed is opening master accounts (Kraken), and state regulators are competing to attract fintechs (Wyoming SPDI).

That said, the sponsor bank model will not die. Column and Lead Bank provide a modern version of a useful and necessary service. But for neobanks scaling to tens of millions of users, the economic loss is too significant not to go after a charter.

Stablecoin-Native Accounts Become the Default

By 2030, the default neobank will offer stablecoin powered digital wallets, savings and yield powered by DeFi protocols, and exposure to tokenized real world assets. Neobanks will bridge the legacy and onchain worlds. Paychecks will arrive by ACH and automatically be converted to USDC where it will earn the risk free rate.

This is Steven’s world from the Manifesto. His neobank is the single financial surface that aggregates investing, saving, getting yield, obtaining credit, and sending money globally. The money moves on whatever rail makes sense: ACH for the landlord, USDC on Solana for paying an international employee, stablecoin on Morpho for savings yield.

By 2030, the distinction between a “bank account” and a “crypto wallet” will have dissolved, leaving in its wake a far superior banking product.

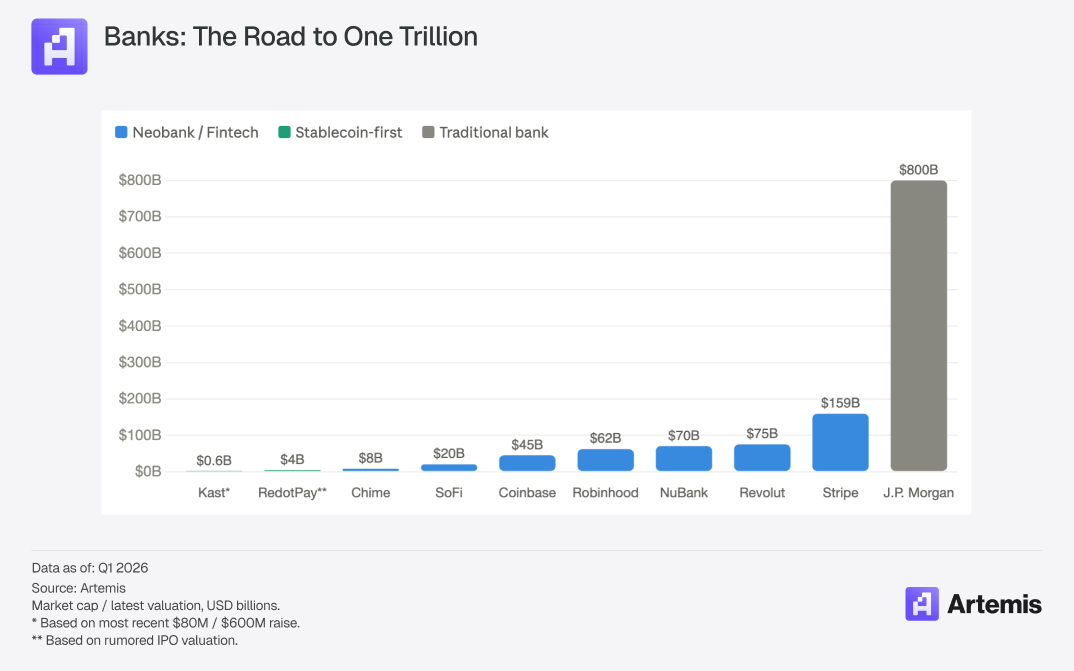

The First Trillion-Dollar Neobank

NuBank is valued at $70B, Revolut $75B, and Stripe $159B. J.P. Morgan, the world’s most valuable bank, has a market cap of about $800B, ten times that of NuBank or Revolut. JPM’s business model is meaningfully different including physical branches, corporate banking, investment banking, asset management. But the comparison is illuminating. A full-stack neobank with NuBank’s efficiency ratio (<20%), Revolut’s product breadth, and Coinbase’s blockchain integration (stablecoin yield, onchain rails, DeFi access) would have a revenue-per-user and margin profile that traditional banks cannot match.

Winners and Losers

Winners:

NuBank: they are already a leader in LatAm with 130m users and have conditional approval to establish a US bank

Revolut: established leader in the EU expanding in the US with a bank charter application

Robinhood: leading the wave of retail investing and financial literacy, their distribution is undeniable, and their product velocity is to be envied

Ethereum: More crypto assets by value sit on Ethereum than any other chain, it has strong Lindy effects, it seems every major exchange is building an Ethereum L2 (Ink, Base, Robinhood Chain)

Solana: Second most value locked in DeFi applications, third most value in RWAs and stablecoins, significantly more performant than Ethereum

Morpho: Indications that it is the protocol that institutions are choosing for onchain asset management and vaults

Circle and Tether: defacto stablecoin winners due to existing distribution and liquidity

The Federal Reserve System: stablecoins will generate more demand for US dollars

Losers:

Cross-border remittance providers like MoneyGram or WesternUnion will have margins crushed

Correspondent banks will lose billions in revenue as margins for cross border payments

Middleware dependent neobanks that never invested in their own infrastructure

Who to watch:

Column: chartered bank built from the ground up for developers

Lead Bank: charter + modern infrastructure

Coinbase: could be a winner with differentiated blockchain-based products

Kraken: challenger in the US, Fed master account, coming after Coinbase

Stripe: Going all in on blockchain tech with Bridge + Privy + Tempo

Phantom: already have millions of users for their wallet product, expanding into neobanking services, wallet is very trading focused

Hyperliquid: Will have the deepest onchain liquidity and best asset offering, enabling neobanks to offer any trading functionality on top

Conclusion

The neobanking stack is compressing from two sides. From the top, neobanks are seeking charters and collapsing the layers between them and the rails that move value. From the bottom, blockchains are removing layers of traditional intermediaries and exposing the bare metal rails to any developer.

Neobanks will drop the “neo” and just become “banks”, while blockchains and stablecoins allow anyone to build a global, self-custodial financial services product at a much lower cost. Assets and capital must flow between the legacy and blockchain financial systems. The banks that win will be those that straddle both worlds, capturing more users, creating better, stickier products and building the first trillion dollar bank.

Explore the full Artemis Neobank Market Map to see every player across all six layers.

To get in touch, please reach out to @x0wes on X, or team-all@artemisanalytics.com

Disclaimer: The authors of this content, as well as affiliates of Artemis Analytics, may have financial interests in the equities or tokens mentioned. This does not constitute investment advice or a recommendation to buy, sell, or hold any asset. The information provided is for educational purposes only and should not be relied upon for financial, legal, or tax decisions. Readers should assess their own circumstances before making any financial choices. Views expressed may change without notice, and Artemis Analytics is not liable for any losses resulting from the use of this content.*