The 2030 Artemis Digital Finance Manifesto

What 2030 looks like for a high agency investor. Here's who wins and loses in digital finance.

Context

Citrini offered 2 lines on what the future of agentic payments looks like.

“Agents went looking for faster and cheaper options than cards. Most settled on using stablecoins via Solana or Ethereum L2s, where settlement was near-instant and the transaction cost was measured in fractions of a penny.” - THE 2028 GLOBAL INTELLIGENCE CRISIS

However, this was written before the launch of Tempo Mainnet on March 18th and misses a chunk of what the new financial system looks like for investors.

Artemis is a digital finance research / data platform used by firms like McKinsey, Visa, Sequoia, and Paypal. Our team comes from BlackRock, Citadel, Whale Rock, Insight and Ribbit Capital. We are a data partner to Tempo and believe we have the best window into what the future of investing, payments and finance looks like and how blockchains impacts that future. We share our view of what 2030 looks like in the essay below.

It’s October 30th, 2030.

S&P just hit another all-time high and broke 10,000. 10.1% of the US population lacks formal employment — AI-induced job displacement led to the rise of millions of humans starting small businesses and becoming creators.

Investors who love fundamentals have seen 50% drawdowns in once “blue chip” names, turning them into contrarian value investments. Dispersion, which began to increase in late 2025 with the advent of advanced AI, continues to skyrocket.

Nvidia is a $20T company and now makes up over 20% of the S&P 500. OpenAI and Anthropic make up over 10% of the S&P 500. While broad beta has done well, buoyed by individual stocks in the index like these, stock picking has done even better.

It’s never been a better time to be an investor.

Steven, a 25 year old graduate from Georgia Tech, wakes up before going to his $90,000/year job at an AI robotics company in Atlanta. He was laid off from Intuit where he was a PM – more companies started moving towards using agents to manage their accounting books – but Steven found his job at the robotics startup shortly after given the immense demand for product talent.

It’s 8am ET. The US markets aren’t open yet, and as Steven prepares for work, he gets pinged by his macro agent “Stan” who advises him to long oil and gold given Polymarkets odds of another conflict in the Middle East surged to 60%.

Steven accepts “Stan’s” suggestion and the agent deploys $5k longs on oil and gold on the HIP-3 market on Hyperliquid. Another agent, the L/S analyst which he calls “Brad” recommends he execute a long / short strategy to long Microstrategy and short BTC given MSTR just started trading below <1 mNAV. Steven asks Brad to execute the trade on Robinhood.

An hour later, he’s at his desk figuring out how to best optimize the new fleet of autonomous farming robots they just launched in Georgia. At lunch, he gets a ping from Artemis that a leading Silicon Valley firm is interested in digging into the autonomous mobility space. Trying to stay anonymous, Steven logs into his Phantom wallet with his PFP of his favorite NBA player Cam Boozer and hops on a Zoom link with a Listen Labs agent that grills him on his view on the competitive landscape for autonomous robots in the US.

After the call, he receives $1,000 from the VC firm in his Phantom Wallet – his agent then off ramps to USDC, and that then routes to Kalshi where his funds are deposited into markets with 95%+ odds. His wealth manager agent that he calls “Charles” has been allocating a majority of his savings to his neobank, where half of his funds are in STRC paying him 10%/year and the rest are earning him 5% on his USDC.

This is the day in the life of a high agency investor in 2030. Steve’s annualized returns far outpace SPY and QQQ and regularly beat benchmarks by double digits.

And he’s not even done yet.

Steven goes home after work to his apartment to be with his partner and decides he wants to write a piece on why he thinks Stripe will be a $10T conglomerate by 2035.

He logs into Artemis and pulls the relevant financials, news, and market maps to put out a long form piece on his thesis. Steven’s fundamental analyst agent “Warren” pays $2.50 via Stripe’s Machine Payment Protocol (MPP) to a sell-side analyst to get their financial model. He then tweaks the assumptions to publish a price target and model. He publishes his long piece and model on X, LinkedIn, and Artemis and immediately gets paid $250 for publishing – GPs and other agents inquire to chat with him about his thesis. Steven responds to these agents and he continues to get paid in his Phantom wallet via Tempo’s MPP for expert advice. Stripe inches up 2% after his post as hedge funds, agents and retail buy into Steven’s thesis. Stripe now has a market cap of over $2T. Steven wakes up the next day with another $1,000 in his wallet. 5 GPs pinged Steven on Artemis if they could invest in his personal fund.

Steven is not unique and is one of hundreds of millions of people in the world who love investing and are taking their financial future in their own hands in 2030. They didn’t have to go to Stanford, some fancy business school or work at Goldman Sachs to have the same tools and investing strategies as the best investors.

Steven now has access to financial tools that didn’t exist 10 years ago – his funds live in a US based fintech founded in 2026 that uses Aave to earn him 4-5% APR for his idle USDC, he primarily uses Phantom (founded in 2021) to interact with HIP-3, Hyperliquid (founded in 2023) to execute trades, and Openclaw (founded in 2025) and Anthropic (founded in 2021) to power his investing agents. The prediction markets he uses to trade and invest in hadn’t existed even 5 years prior. The payments he receives from hedge fund managers for his research go through Tempo, which didn’t even exist 5 years ago.

This brave new world that Steven lives in allows him to be a world class investor, despite no “formal” investing experience.

Steven, who doesn’t come from wealth, now has “Charles”, “Brad”, “Stan” and other analysts at his fingertips and is able to support himself, his partner and his parents financially. At age 25, Steven is now effectively a solo PM managing the 6 figures he’s been able to save and earn. He now has a technical analysis analyst, a macro analyst, a fundamental analyst, a quant analyst, and a prediction analyst who ping him on Telegram on suggestions on what he should do next.

He’s able to trade / invest and earn in his day job to provide for his family and loved ones just from being high agency and curious.

Investing has changed because of digital finance.

Digital Finance in 2030

At Artemis we believe neobanks, lending, agentic payments, prediction markets and trading are the most enduring markets enabled by blockchains and completely changes investing in 2030.

We call these the 5 core pillars of Digital Finance:

Neobanks changes because individual investors now have one interface and system of record that can interact with all their finances whether assets on blockchains like stablecoins or fiat currency and can send money through any payment rail (ACH, Wire, RTP, Stablecoins, etc)

Lending changes because humans will always need capital to do things and borrow lend protocols allow anyone access to world class savings yield or access to credit.

Agentic payments changes investing because our agents will need to pay for resources at machine speed, and the current internet has no way to monetize the explosion of non-human traffic. There will be a new class of merchants in this agentic web.

Prediction markets changes because investors can finally express beliefs in the world that they previously couldn’t with just spot / equities.

Trading changes because investors can now express their beliefs in the world without staring at charts when agents can and tap into 24/7/365 markets on perpetual exchanges and trade on their behalf.

Today we share our thesis and our winners / losers in these new markets of finance. Here’s a teaser of what’s to come research at Artemis:

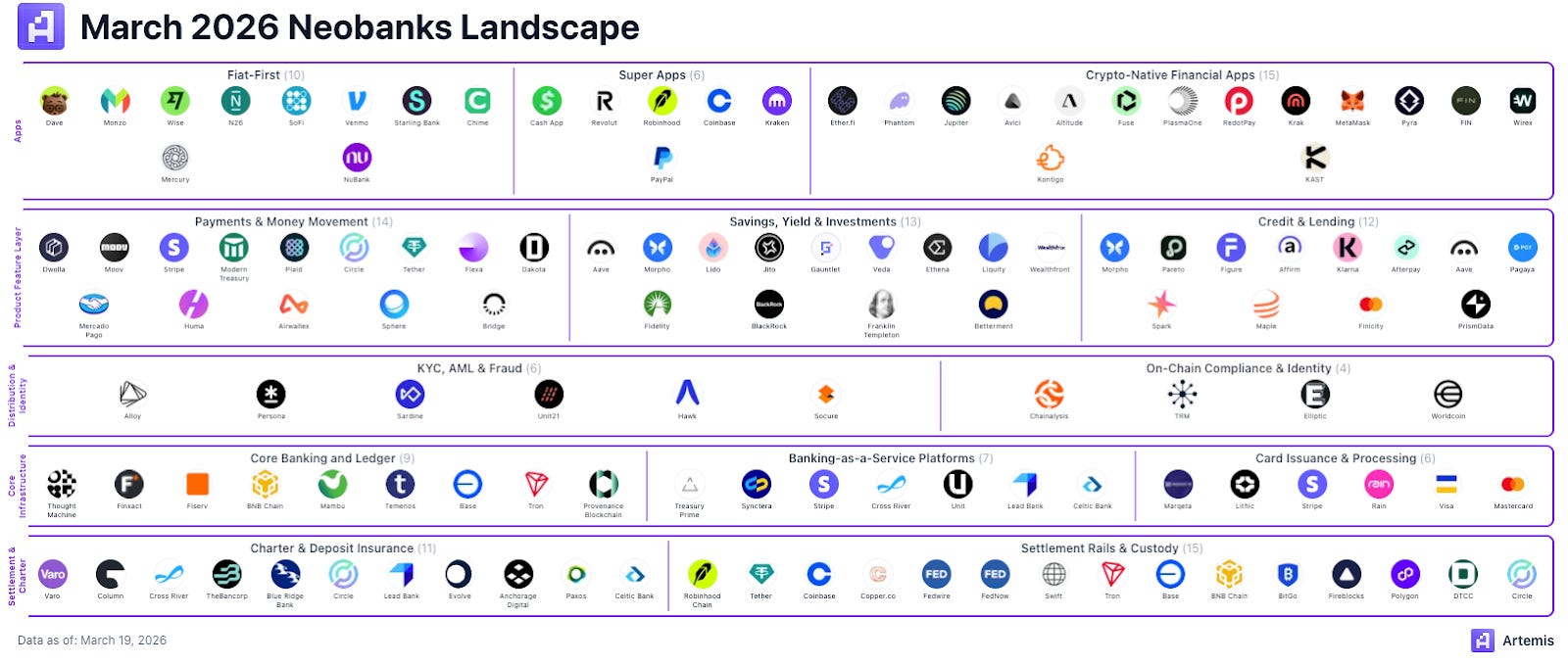

Neobanks - Alex Weseley

Steven’s neobank is where his entire financial life exists. It is the single financial surface that aggregates investing, saving and getting yield, obtaining credit, and sending money globally. This was only made possible because public blockchains allow developers to interact directly with bare metal financial plumbing, while legacy rails like ACH and Fedwire remain the connective tissue to the existing economy. Permissionless finance means Steven can receive an ACH direct deposit straight into his stablecoin account, and immediately lend it on Morpho to get 5%.

We are seeing this shift happen today in real time: Kraken has a Master Account at the Fed, NuBank is establishing a chartered bank in the US, and Coinbase has applied for a bank charter. Neobanks are attacking from two sides: integrating vertically across the legacy stack while building on the emerging permissionless stack. A neobank that owns both the legacy rails and the emergent stack can offer financial products that firms existing in only one stack cannot offer.

What changed at the infrastructure level has had a profound impact on Steven at the surface. It has unlocked access to financial products previously reserved for the wealthy and connected: yield on cash, credit against assets, 24/7 asset management and global money movement. Access to more sophisticated tools means a savvy person like Steven can afford to support his family because his money is always working. Wealth used to compound for the wealthy - tomorrow’s neobanks will make it compound for everyone.

Winners: Robinhood, Revolut, Coinbase, Nubank, Ethereum, Solana, Morpho, Hyperliquid

Losers: Legacy financial institutions unable to innovate and acquire young customers

Who to look out for: Column, Lead Bank, IBKR, Stripe

Neobank Market Map: March 2026 Neobank Market Map

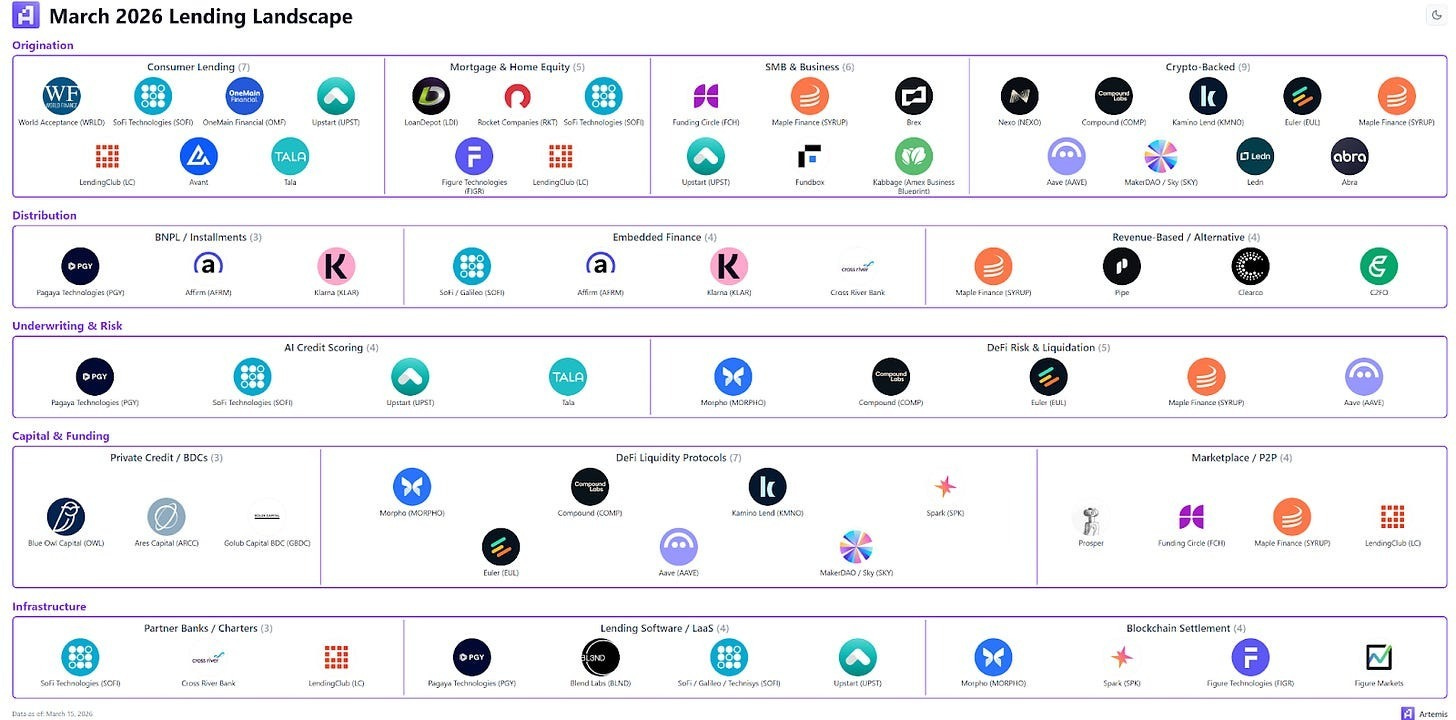

Lending - Mario Stefanidis

Lending in 2030 is going to be a story of blockchain rails and AI risk assessment. The old model of human loan officers, rigid FICO scores and slow approval cycles was built for a world where assessing risk was expensive and moving capital was slow. AI makes underwriting cheap while the blockchain makes settlement instant.

The entire lending stack, from origination to capital funding, is being rewritten by software that prices risk faster, distributes credit through embedded channels and settles on programmable rails. The winners are picks and shovels names that own the intelligence layer or the settlement rail rather than those that rely hose rely on their balance sheet.

This is arguably the sector where new technology hits hardest. The core function of deciding who gets capital and on what terms is pure decision-making, and that is exactly what gets cheaper as AI scales. But the other half of the equation is equally important: moving that capital efficiently once the decision is made.

The old lending stack was vertically integrated inside banks. GSIBs had a moat because they could originate, underwrite, service and fund the loan all under their roof, maximizing margin. They were in bed with regulators and their cumbersome manual processes made their stack extremely difficult to reproduce.

What is happening now is a full unbundling and rebundling of that stack across five layers: origination, distribution, underwriting and risk, capital and funding, and infrastructure.

At the origination layer, digital-native lenders like SoFi, Upstart and Affirm have already pulled volume away from legacy incumbents by offering faster, fully digital experiences across consumer, mortgage, SMB and crypto-backed lending.

At the distribution layer, BNPL and embedded finance are pushing credit to the point of purchase. Affirm and Klarna are lending distribution networks sitting inside checkout flows.

At the underwriting layer, AI credit scoring from Upstart and Pagaya is expanding the addressable borrower pool by evaluating thousands of variables legacy models ignore.

At the capital layer, DeFi protocols like Aave (which has surpassed $1 trillion in cumulative loans), Morpho (now partnered with Apollo Global) and Maple Finance ($3.2B TVL, up from $500M) are creating permissionless, 24/7 capital markets that fund loans without a bank in the middle. Liquidity protocols allow lenders and borrowers to transact in stablecoins and to earn interest on pledged assets.

On the infrastructure side, blockchain settlement is collapsing what used to take days into seconds. Figure Technologies is originating HELOCs and first-lien mortgages natively on-chain, cutting out the layers of intermediaries that made traditional mortgage closing slow and expensive. SoFi’s Galileo/Technisys stack and lending-as-a-service platforms provide the remaining plumbing.

Winners: SoFi, Upstart, Aave, Figure, Affirm

Losers: Legacy banks, failed CeFi lenders that blew up in 2022, declining DeFi protocols that never found product-market fit, TrueFi stagnating at minimal TVL

Who to look out for: Creditas, Morpho, Fluid, Ledn, Figure (new loan products)

Lending Market Map: March 2026 Lending Market Map

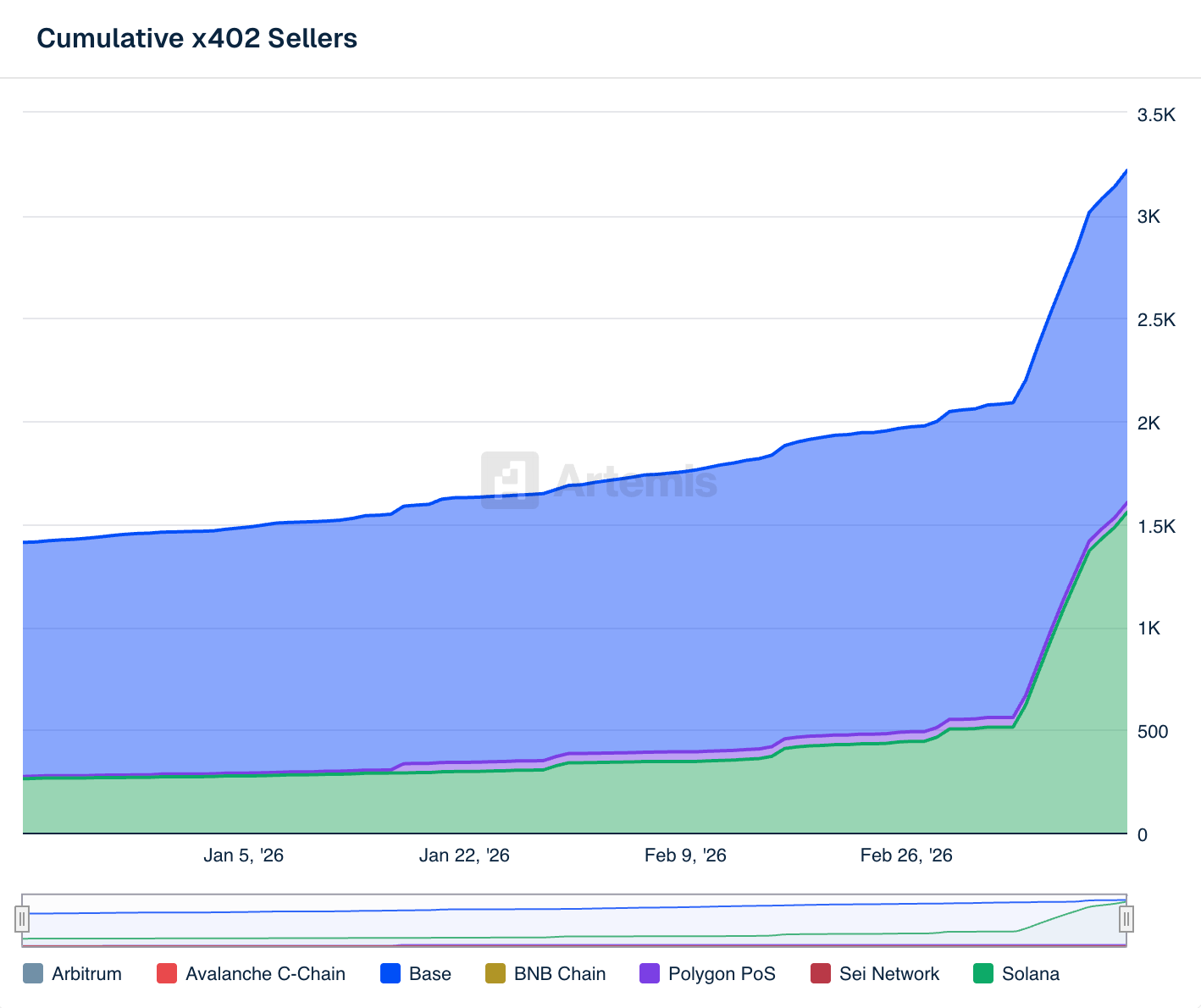

Agentic Payments - Lucas Shin

As it currently stands, the internet is built for humans. It uses rate limits, CAPTCHAs, and API keys to filter out non-human activity, and monetizes human users with ads. But with the proliferation of autonomous agents, the economics break. More traffic – fewer eyeballs. Servers that have historically been subsidized by ad revenue will face orders of magnitude more requests from users who will never be influenced by ads. Agentic payments solve this naturally, with micropayments as the access key. Pay-to-crawl.

As our trust in AI accelerates, our agents will begin making hundreds of sub-cent API calls per hour on real-time data and tooling, buying what they need to carry out the goals we’ve prompted them with. Unlike humans, agents won’t be limited by speed, and they won’t ever need to rest. If even a fraction of the world’s billion knowledge workers utilize agents spending a few dollars a day on their behalf, we’ll see an agent-initiated transaction surface measured in the hundreds of billions annually. When agents start selling to each other — packaging already-solved problems as cheap endpoints for other agents — that number will quickly compound.

We see all of that value concentrating to the user interface, the payment infrastructure, and the merchant ecosystem.

The interface layer includes search engines, aggregators, and the user-facing surfaces that humans actually interact with. Unlike the ad-supported web, where Google aggregated free content and monetized through ads, the agent web will be transactional by default. Whoever controls the user has the leverage, ultimately controlling how agents discover, choose, and pay for resources.

Payment infrastructure spans the stablecoins, blockchains, and facilitators that will process every agent-initiated transaction. Circle and Tether will provide the currency. Stripe, Visa, and Coinbase are building the bridges between these new rails and existing financial infrastructure. Whoever can build the most seamless financial experience for agents will sit directly in the flow of funds and capture the value created by this emerging market.

The merchant layer will be made up of both existing products that become accessible to agents and entirely new categories of products and services that have yet to emerge. With companies like Stripe and standards like x402 lowering the barriers to monetization, any developer, business, or agent will be able to offer paid services. Over time, agent-driven demand will give rise to entirely new markets, much like the internet did.

The tools for this new internet are already being built.

Winners: Circle, Visa, AWS, Cloudflare, Stripe

Losers: Google, Meta, Salesforce, Phantom, Apollo, ZoomInfo, Worldcoin

Who to look out for: Tempo, Arc, Merit Systems

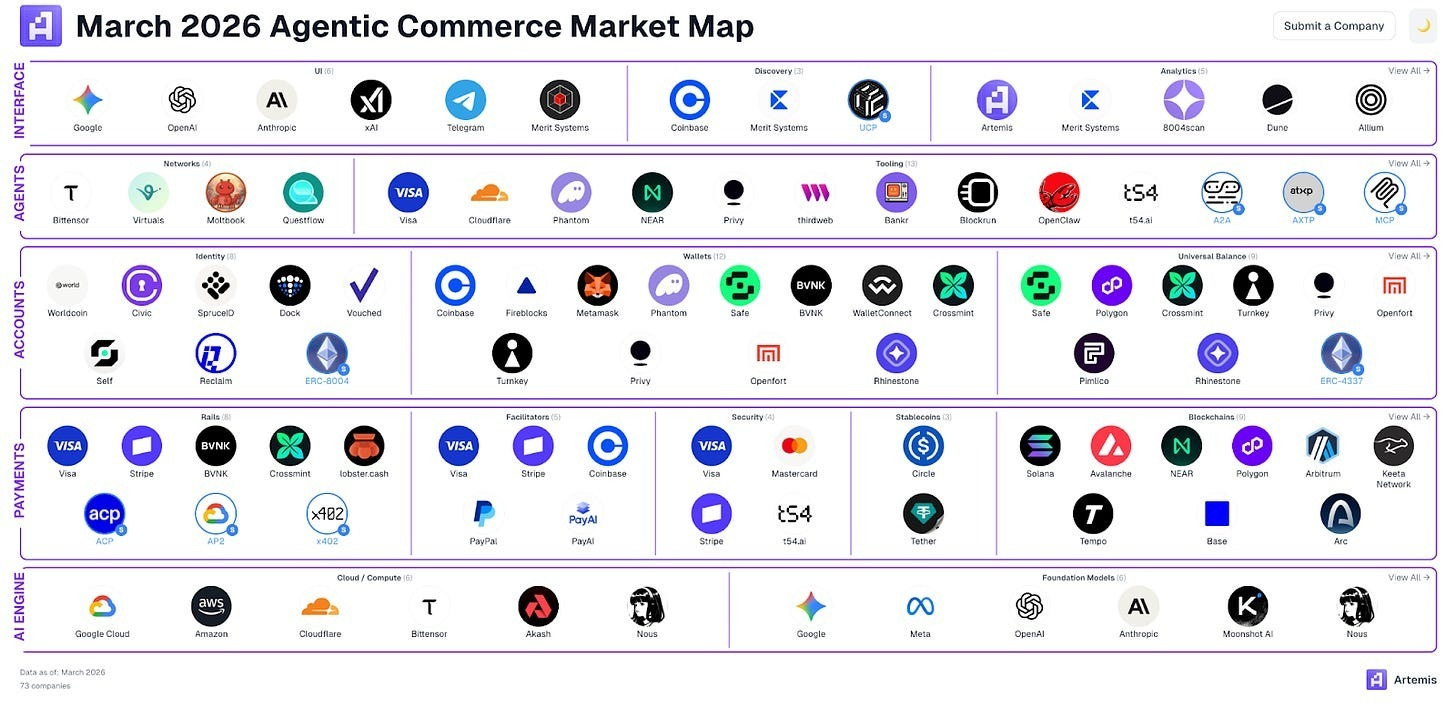

Agentic Commerce Market Map: March 2026 Agentic Commerce Market Map

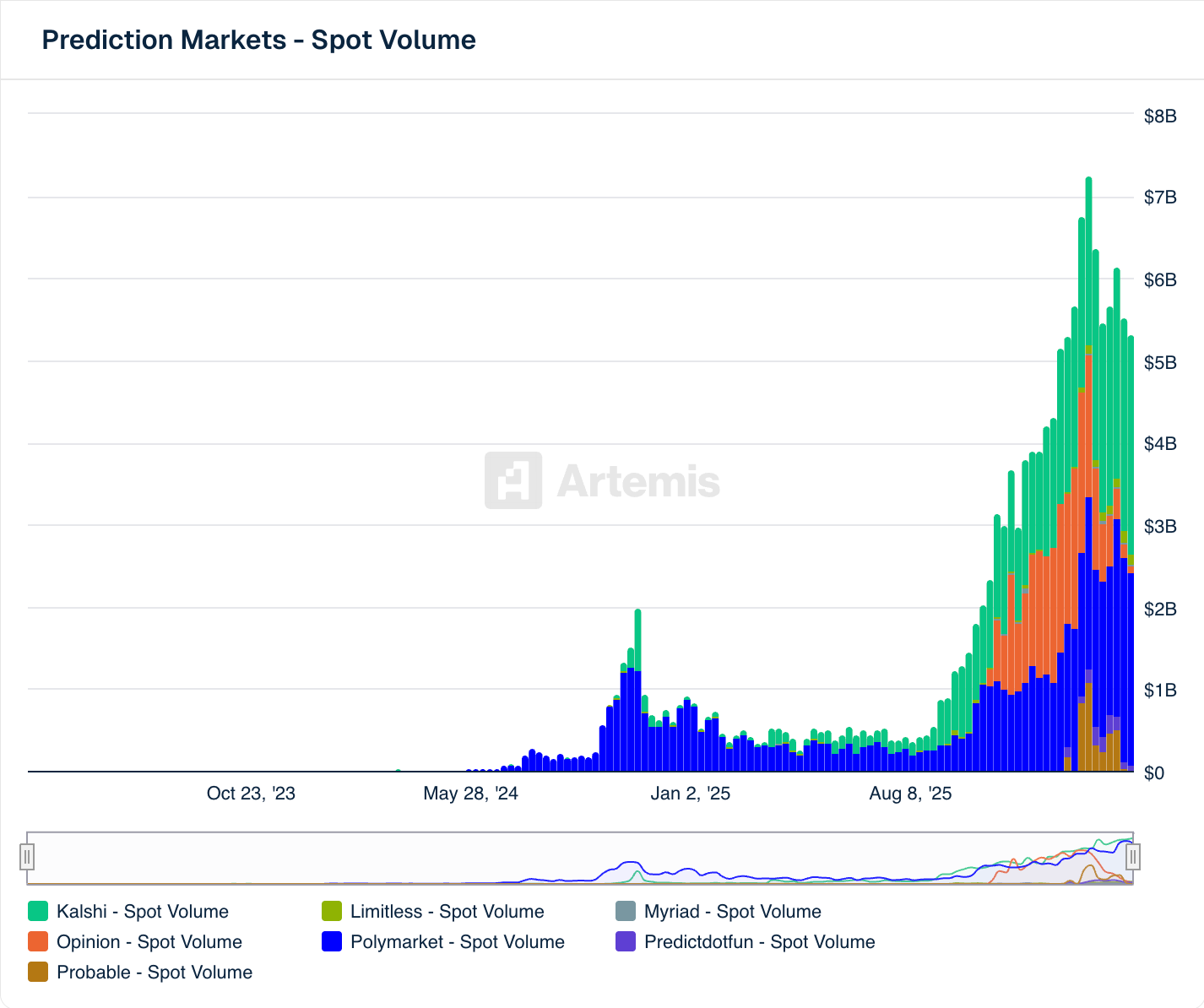

Prediction Markets - Kaviish Sethi

Prediction markets sit at the intersection of finance and information. Their core function is to simply convert beliefs about future or certain outcomes into prices. When participants risk capital on an outcome, they reveal what they truly believe. The resulting price of an outcome isn’t just a probability; it’s a live signal of the collective belief.

The internet is full of predictions, but none are properly incentivized. There is no cost of being wrong so simply looking at opinions is very shallow. Prediction markets fix this by attaching financial consequences to forecasts. Accuracy is awarded and inaccuracy is penalized, overtime creating a signal which is far more reliable than polls or other static models. This turns prediction markets into an infrastructure that continuously aggregates information.

Prediction markets were historically constrained by poor distribution, low liquidity, and slow settlement, which prevented them from becoming reliable information systems.

The path forward is more crypto native systems. Crypto removes these barriers by enabling global participation, permissionless market creation, and composability allowing liquidity and users to aggregate in ways regulated platforms cannot. As AI agents and automated systems demand real time, reliable forecasts, prediction markets become the primary source. This convergence is what turns prediction markets from a niche to a core infrastructure.

By 2030, prediction markets evolve from niche venues into core financial infrastructure for pricing uncertainty.

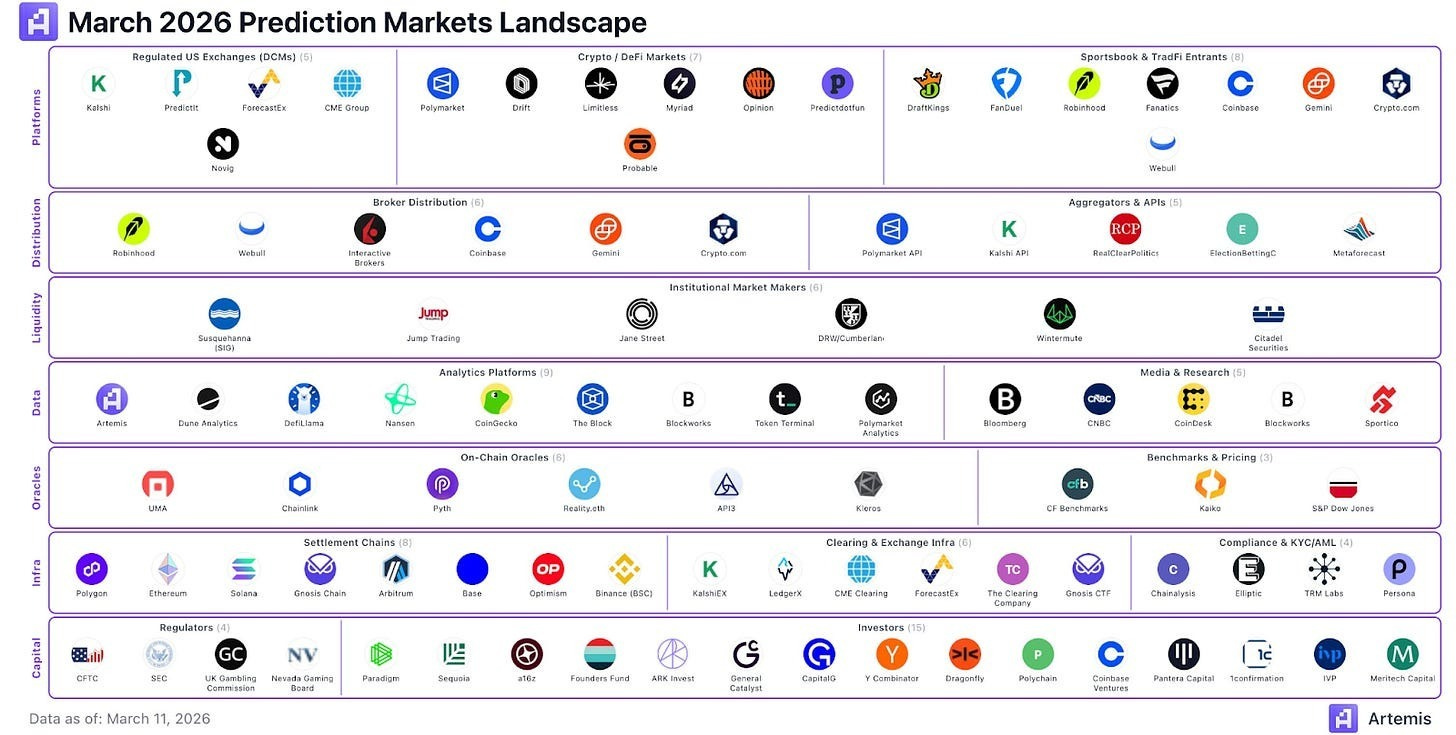

At the platform layer, activity spans regulated exchanges like Kalshi and CME, crypto native markets like Polymarket and sportsbook or tradfi entrants like DraftKings, Robinhood and Coinbase. What began as fragmented venues converges into a unified surface for trading probabilities.

At the distribution layer, brokerages such as Robinhood, Interactive Brokers and Coinbase, alongside aggregators and APIs like Polymarket API and Kalshi API, embed prediction markets directly into financial interfaces. Forecasting becomes native to consumption, not a separate destination.

At the liquidity layer, institutional market makers including SIG, Jump, Jane Street, DRW, Wintermute and Citadel provide continuous two sided pricing. Probabilities become a new asset class with tight spreads and scalable depth.

At the data layer, analytics platforms like Artemis, and Dune, alongside media and research such as Bloomberg and CoinDesk, standardize and distribute prediction signals. Market implied probabilities become core inputs for decision making across finance, media and AI systems.

At the oracle layer, systems like UMA enable reliable resolution of real world events, while benchmarks and pricing providers further formalize probability as a measurable financial signal.

At the infrastructure layer, settlement chains such as Polygon, Base and Solana, alongside clearing systems and compliance rails, form the backbone. On chain rails tie the entire stack together, unifying market creation, liquidity, settlement and data into a single global system. Capital moves permissionlessly, markets operate 24/7 and probabilities become portable financial primitives that can be traded, embedded, collateralized and integrated across applications.

At the capital layer, regulators including the CFTC and SEC, along with investors such as a16z, Paradigm and Sequoia, provide the oversight, capital and legitimacy required for markets to scale globally.

In this structure, prediction markets resemble a derivatives system built not on prices, but on likelihoods. Their importance is not just in the contracts themselves, but in the continuous signal they produce, a globally accessible, financially backed probability that becomes the most efficient way to aggregate and price information about the future.

Winners: Kalshi, Polymarket, Robinhood

Losers: Traditional polling and forecast models, small prediction platforms without liquidity or distribution, and sportsbooks that stay limited to sports betting

Who to look out for: Robinhood and other platforms building in house prediction markets

Prediction Markets Market Map: March 2026 Prediction Markets Market Map

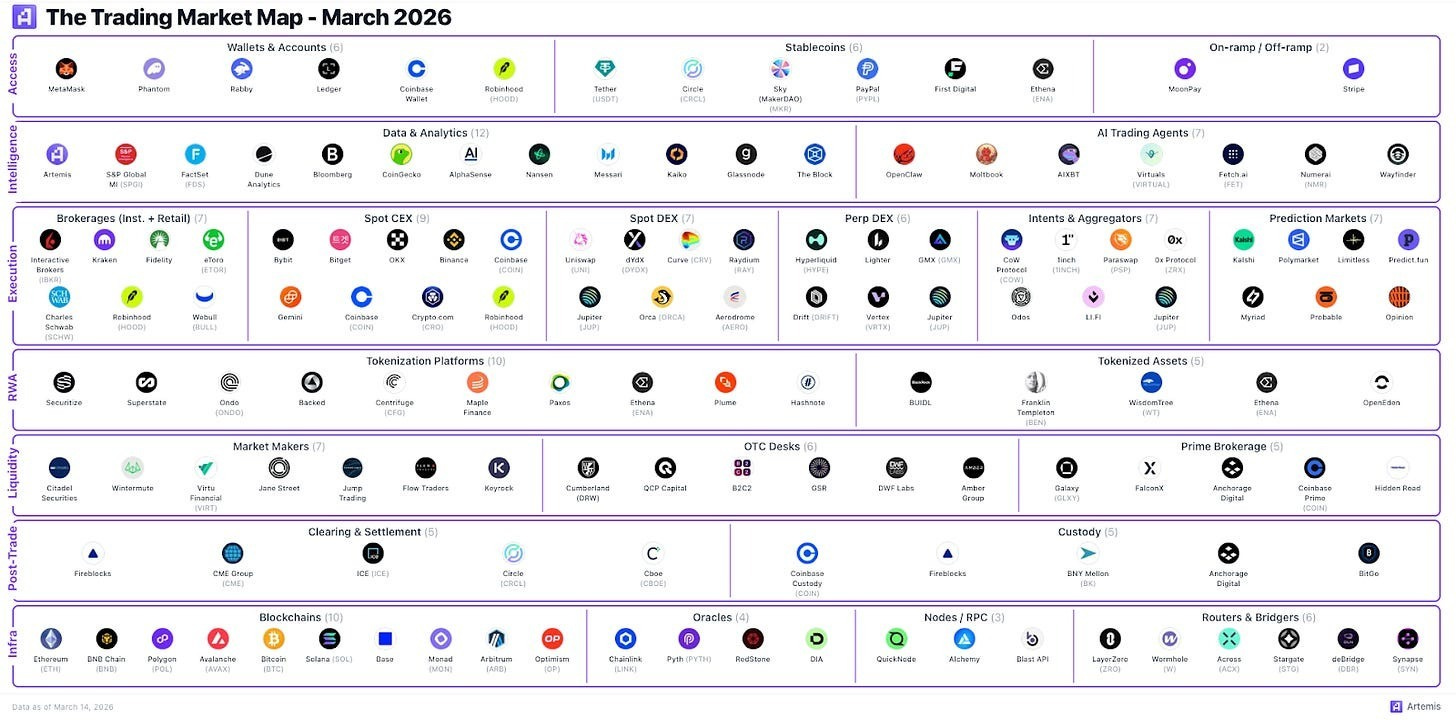

Trading - Zheng Jie Lim

Trading in 2030 becomes huge for a dark reason: more people will feel behind and cannot afford to be passive. The old brokerage model was built for a world where investing was slower, more intentional and separate from the rest of a person’s financial life. Previously, we had one account for banking, investing and maybe another for crypto. The market had fixed hours. Product menus were narrow. Acting on a view took more steps.

That world is changing.

AI compresses work. AI will widen the knowledge gap first, then the execution gap and eventually the wealth gap. The people with the best tools, data and distribution will learn faster, act faster and compound faster. For everyone else, the pressure shows up as a feeling: the gap is widening faster than salary can close it. Social media makes that impossible to ignore. Other’s people upside becomes your benchmark. Patience starts to feel less like wisdom and more like a slow way to fall behind.

That is why trading gets bigger. Trading platforms become the place where users hold cash, react to news, express macro views and turn information into action.

The old trading stack was fragmented across banks, brokerages, exchanges, and crypto apps. Each owned one narrow part of the user journey. That separation made sense when products were siloed and users tolerated more friction.

What is happening now is a rebundling of that stack across four layers: the access layer, the execution venue, the liquidity layer, and the market infrastructure underneath.

At the access layer, platforms like Robinhood, Coinbase, Webull, and eToro are trying to become much more than brokerages. Robinhood already combines equities, options, prediction markets, cards and cash features in one app. Coinbase is moving beyond spot crypto into stablecoin yield, payments and broader financial access. The company that owns the interface owns the habit.

At the execution layer, product breadth will matter. Hyperliquid shows what a fast, crypto-native trading venue looks like. Robinhood is widening access across asset classes. Coinbase remains a key venue for retail crypto activity. The winners are the one that let users move across products without leaving the ecosystem.

At the liquidity layer, market makers, internalizers and order routers determine whether users get tight spreads and reliable execution. This layer is less visible and matters as trading volume grows and more products become tradable.

At the infrastructure layer, exchanges, clearinghouses, custody and settlement systems still matter because trusted matching and settlement is needed. ICE remains important because if more of the world becomes tradable, the owners of key market infrastructure still capture value.

In 2030, a 29-year-old college graduate might get paid via direct deposit into Coinbase, Robinhood, or Hyperliquid. They keep part of their cash in a yield-bearing stablecoin and use the same platform to buy US equities, express macro views, and trade crypto perps.

Trading will become a cultural outlet for the ambitious and insecure that need to catch up. Some may still call it investing but for many users, it is about trying to close the wealth gap before it widens further. The platforms that win will understand this clearly: they are selling speed, hope and the feeling that you still have a shot to make it to the upper middle class.

Trading will keep growing exponentially 2030 and beyond

Winners: Robinhood, Coinbase, ICE, Kraken

Losers: Legacy Brokerages - as they are slower, less native and harder to innovate

Who to look out for: Interactive Brokers, Webull, SoFi, eToro, Hyperliquid

Trading Market Map: March 2026 Trading Market Map

Conclusion

Today we shared a brief window into what the world looks like for the high agency investor — we look forward to continuing to share deep dives in the core sectors by our world class analysts.

Who wins in the future of trading: Hyperliquid or Robinhood?

Who wins in the future of prediction markets: Kalshi or Polymarket?

Who wins in the future of neobanks: Phantom or Nubank?

Who wins in the future of lending: Aave or SoFi?

Who wins in agentic payments: x402 or MPP?

We tackle these questions in a series of essays in the coming weeks.

Disclaimer: The authors of this content, as well as affiliates of Artemis Analytics, may have financial interests in the equities or tokens mentioned. This does not constitute investment advice or a recommendation to buy, sell, or hold any asset. The information provided is for educational purposes only and should not be relied upon for financial, legal, or tax decisions. Readers should assess their own circumstances before making any financial choices. Views expressed may change without notice, and Artemis Analytics is not liable for any losses resulting from the use of this content.

Special thank you to Son Do, Wei Guo, Vincent Jow for the feedback on our piece. Thank you Freda Duan for inspiring how investing unfolds.

| A guest post by

|

by the way most of what Steve does on this 2030 scenario is already feaseble today. the difference you emphasize i believe is on the popularization of those plataforms, and with that i could not agree more.

Last but not least... tks for this report. always good to dive into organized thinking as it has. Congrats and thx

"It’s 8am ET. The US markets aren’t open yet, and as Steven prepares for work," - Sure you are talking about 2030 and Tradfi still works on 80´s banking time?