Why Circle Had Its Worst Day Ever

A proposed shift in U.S. stablecoin regulation triggered a sharp repricing, highlighting how changes to yield, distribution, and policy expectations can impact Circle’s business model.

CRCL plunged 20% on Tuesday, its steepest intraday drop since going public, erasing $5B in market cap in a single session. Volume hit 56.4 million shares, nearly 4x its 90D average. Coinbase fell 11% in sympathy.

The entire stablecoin trade got repriced in hours. The catalyst was a new draft of the Clarity Act that would effectively kill passive stablecoin yield.

The story goes deeper than a single red day, though. There’s a regulatory fight, a business model vulnerability, and a wallet freeze that poured gasoline on an already burning stock.

The Clarity Act Bombshell

On March 20, Senators Thom Tillis (R-NC) and Angela Alsobrooks (D-MD) announced an agreement in principle on stablecoin rewards, with White House backing. The full text was reviewed by crypto industry leaders in a closed-door Capitol Hill session on Monday.

The key provision: passive stablecoin yield, earned simply for holding a dollar-pegged token, is banned. Exchanges, brokers, and their affiliates would be prohibited from offering yield directly or indirectly on stablecoin balances, or in any manner “economically equivalent to interest.”

Activity-based rewards tied to payments, transfers, or platform usage would still be allowed. The SEC, CFTC, and Treasury would jointly define permissible rewards and anti-evasion rules within one year. Note the SEC and CFTC recently announced a historic memorandum between the agencies, ending years of interagency fighting and discord.

Congress just put in writing the line the banking lobby has been drawing for two years. Stablecoins can be payment instruments, but they cannot be deposit substitutes.

One industry leader at the closed-door session, reported via an internal stakeholder email obtained by Eleanor Terrett, described the text as a “departure” from what had been previously discussed with the White House. They warned that the “economic equivalence” standard is deliberately vague and could be interpreted far more restrictively by future regulators.

This Hits Circle Harder Than Anyone

95.5% of Circle’s revenue currently comes from interest income on USDC reserves, which explains the sell-off.

CRCL issues USDC, holds the reserves in short-duration Treasuries and overnight repos, and earns the spread. In Q4 2025, reserve income was $711MM, up 60% YoY, driven by 97% growth in average USDC supply. FY2025 revenue was $2.7B, up 64%.

The Clarity Act doesn’t directly attack Circle’s reserve income (CRCL earns that yield itself) but it is a direct attack on its demand engine. Platforms like Coinbase currently pass stablecoin yield through to users as an incentive to hold USDC. Coinbase’s stablecoin revenue hit $1.35B in 2025, up from $910MM in 2024. If exchanges can no longer offer yield on USDC balances, the incentive for users to hold USDC over a traditional bank deposit weakens considerably.

Less yield-sharing means less USDC adoption means less reserves means less interest income for Circle.

The timing makes it worse. Reserve yields already declined from 4.49% in Q4 2024 to 3.81% in Q4 2025 as the Fed cut rates. While the market is no longer pricing in cuts this year, Circle’s interest income was already under pressure before this bill showed up.

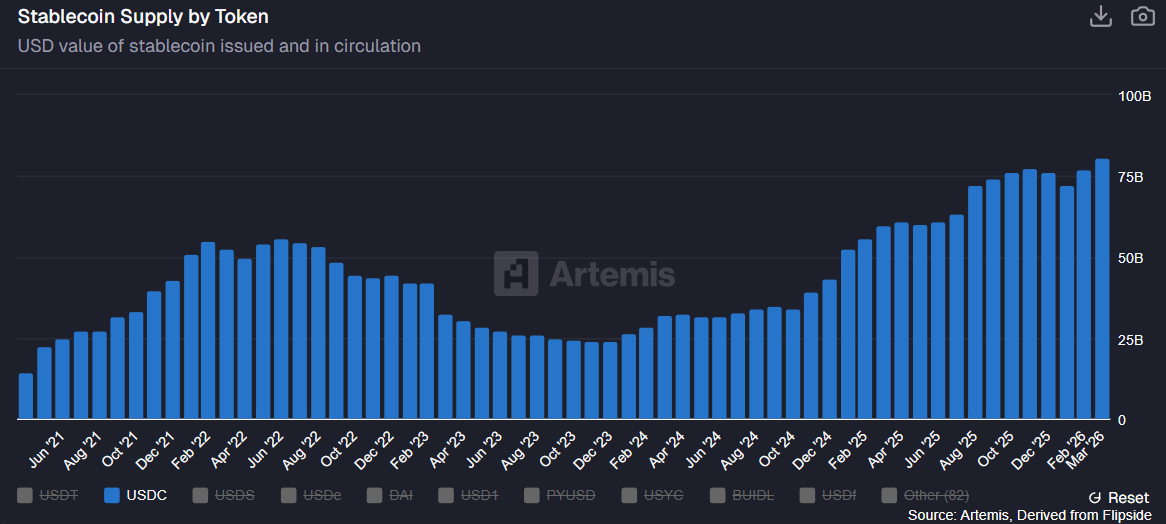

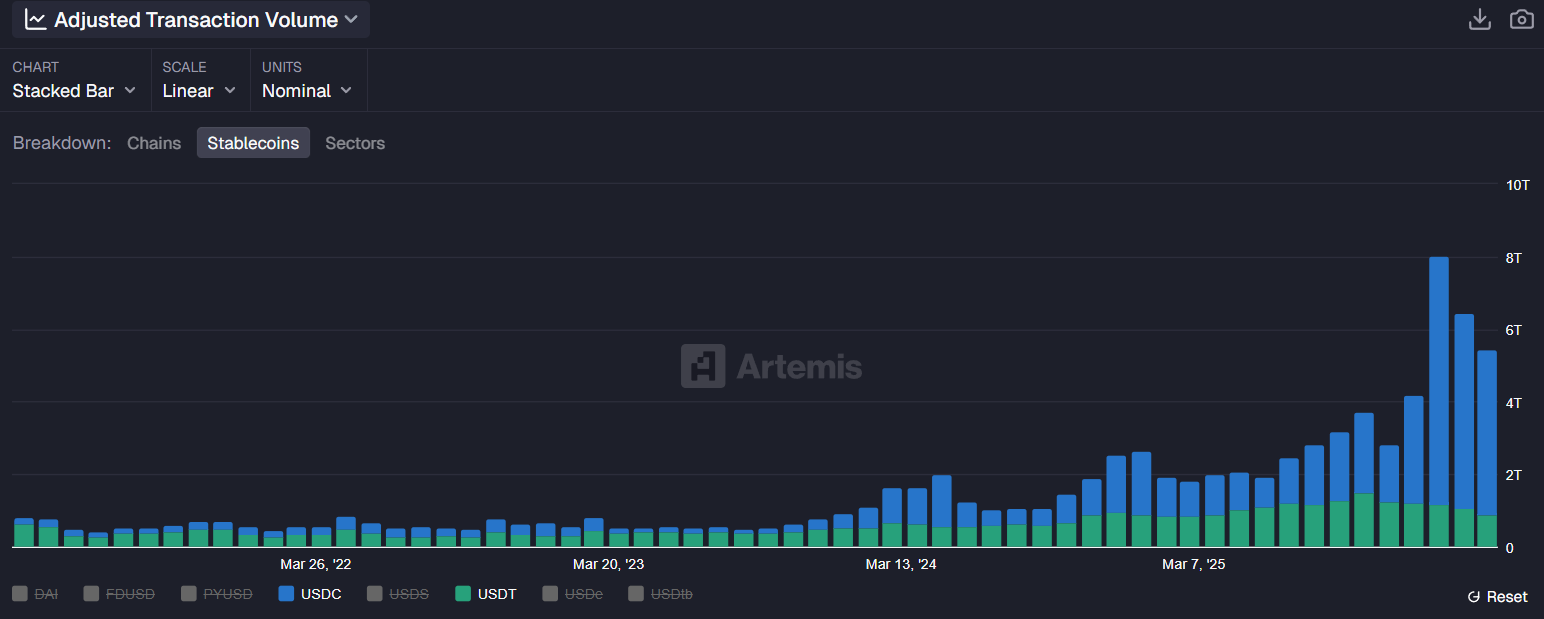

USDC Fundamentals Have Never Been Stronger

The stock cratered on a day when USDC’s underlying metrics are at all-time highs:

Circulating supply: $81B as of late March, up from $76B at year-end 2025.

Onchain transaction volume: $6.8T (adjusted) in Q4 2025 alone, up >2x YoY.

Market share vs USDT: USDC volume has surpassed Tether’s USDT every month since August 2025, now capturing >80% share in 2026.

Q4 earnings beat: $770MM in revenue vs. $745MM expected. EPS of $0.43 beat Street consensus by 23%.

Circle also just announced an expansion into Africa through a Sasai Fintech partnership and secured a major Intuit integration.

The Wallet Freeze Poured Gasoline on the Fire

Circle froze the USDC balances of 16 business hot wallets late Monday, disrupting operations at several exchanges, casinos, and ForEx platforms including FxPro, Pepperstone, AMarkets, and HeroFX.

The freeze reportedly stemmed from a U.S. civil case whose details haven’t been disclosed. @zachxbt raised pointed concerns, noting that anyone with basic onchain tools could identify these were operational business wallets processing thousands of transactions. He warned that opaque freezes based on undisclosed civil actions risk turning USDC into “a politicized gatekeeping tool.”

The power to blacklist and even wipe frozen addresses is explicitly coded into USDC’s smart contracts.But on a day when the market was already questioning centralized stablecoin risk, the optics could not have been worse.

There’s Still a Bull Case

The sell-off prices in a worst-case reading of the Clarity Act. There are a few things worth considering on the other side.

Activity-based rewards survive. The bill draws a line between passive yield (banned) and transaction-based incentives (allowed). Coinbase and others are already exploring workarounds: marketing incentives, activity-based payments, issuer partnerships that blur the line between interest and rewards. The “economic equivalence” standard is vague, which means it will get lawyered.

Coinbase’s P&L may not change much. Coinbase largely passes stablecoin yield through to users, so the revenue is often offset by expenses. Analysts argue the direct earnings impact is limited. The bigger question is whether restrictions slow long-term USDC adoption.

This bill isn’t law yet. The committee markup isn’t expected until the second half of April, after the Easter recess. There’s still time for lobbying, amendment, and negotiation. Brian Armstrong has been notably silent on the latest text, but his previous positions suggest Coinbase will fight hard on the “economic equivalence” language.

Non-reserve revenue is growing fast. Platform services, transaction processing, and other non-reserve income grew >15x YoY to $37 million in Q4, with full-year other revenue reaching $110 million. Still small relative to interest income, there is now a diversification story.

The Setup From Here

CRCL was up 170% from its February lows before today. The stock rallied from $50 to $127 on blockbuster earnings, the USDC/USDT flippening, and the Intuit partnership. However, the valuation had already priced in flawless execution on interest income, AI-driven payments, and tokenization, leaving zero room for regulatory disappointment.

At $101 now, CRCL trades at roughly 9x annualized revenue. The contention now is whether the Clarity Act kills the USDC growth flywheel or forces it to evolve. If stablecoin adoption keeps accelerating on the back of payments, cross-border settlement, and institutional use (onchain data is still positive), then Circle’s reserve income engine stays intact regardless of whether Coinbase can offer yield on idle balances.

Disclosure: This material is provided for informational purposes only and does not constitute investment advice, financial advice, trading advice, or any other form of advice. The views expressed are those of the authors and should not be relied upon as a recommendation to buy, sell, or hold any asset. The authors or affiliated entities may hold positions in the assets discussed. You should conduct your own research and consult appropriate financial professionals before making any investment decisions.