The Lending Stack Has Flipped - Who Owns the New Chokepoints?

The $348T credit market is being quietly rebuilt — from vertically integrated banks to a modular stack where AI underwriting and blockchain rails capture the economics

Global debt hit a record $348 trillion at year-end 2025, according to the Institute of International Finance. Government borrowing accounts for roughly $107 trillion, corporates another $101 trillion, households $65 trillion, and the financial sector $76 trillion. Digital and fintech lending platforms represent somewhere between $590 billion and $680 billion of that total, aka less than 20 bps.

The largest credit market in human history is still running on infrastructure designed decades ago (FICO 1989, MERS 1995). The average cost to originate a single mortgage in the United States is somewhere around $11k, according to the Mortgage Bankers Association. This is double what it was in the early 2010s despite massive technological improvements and the advent of AI.

Source: Freddie Mac

Settlement on a standard wire transfer still takes roughly 28 hours, and credit decisions at most banks still route through committees applying black box scoring models built on 20 to 30 variables. None of this is a secret, but what is less obvious is how the fix is actually happening.

Lending is not being disrupted in romantic Silicon Valley fashion with a single startup replacing GSIBs like JPMorgan. What is happening is subtler and more structural: the vertically integrated bank lending stack — where origination, distribution, underwriting, funding, and infrastructure all lived under one roof — is decomposing into a horizontal, modular stack where specialists own individual layers.

This is the same architectural shift that happened in cloud computing when monoliths gave way to microservices, and in media when the studio system gave way to the streaming and creator stack. This shift is finally happening in credit.

The winners in this rebundling are not the companies with the largest balance sheets. They are the companies that own the chokepoints, the layers that other participants cannot route around. Two positions matter more than anything else: the intelligence layer, where AI underwriting and risk scoring decide who gets capital and on what terms, and the settlement rail, where blockchain infrastructure is collapsing origination costs and settlement times by orders of magnitude. If you own one of those two picks-and-shovels positions, other lenders pay you rent. If you own neither, you are competing on price in a commodity market with $3.5T in private credit looking for yield.

At Artemis, we mapped 40 companies across 15 sub-categories organized into five layers to understand where structural value is accumulating.

The Five Layers of the New Lending Stack

Layer 1: Origination

The origination layer is where loans are born. These include consumer loans, mortgages, small-business lending, and crypto-backed loans. It is also increasingly a commodity. The ability to originate a loan today is not a moat, it is table stakes/the bare minimum. What separates winners from the rest is origination cost and approval rate. SoFi, valued at ~$24B, and Rocket Companies (Rocket Mortgage) at $48B boast large origination figures, but their margin stories are about how cheaply they can originate. Figure ($6B) is originating HELOCs and first-lien mortgages natively on its Provenance blockchain, cutting out the layers of intermediaries that made traditional mortgage closing slow and expensive. On the crypto side, Aave at $2.7 billion in market cap and MakerDAO/Sky at $1.6 billion are blurring the line between fintech and DeFi origination entirely.

Layer 2: Distribution

Distribution is where demand aggregation happens, and it is being rewritten by embedded finance and BNPL. The embedded finance market is projected to grow from $156B in 2026 to $454B by 2031, a 24% CAGR. BNPL is projected to cover 13% of all digital transactions, up from 6% in 2021. Affirm at $15B and Klarna at $5B are the visible names, but the real structural story is that lending is embedded inside checkout flows, software platforms, and merchant experiences. Both AFRM and KLAR are down significantly from ATH but are not the picks and shovels names poised to win mass share. The lender the borrower never sees is often the lender that wins. Every major software company is now adding financial products. Shopify, Amazon, Square, Stripe all need the API infrastructure layer, and whoever provides it collects a toll on every new dollar of volume.

Layer 3: Underwriting and Risk

This is the first chokepoint in the stack. The company that scores the borrower controls the economics of the entire lending chain. The credit bureau oligopoly consists of three juggernauts: Experian, TransUnion, and Equifax. Collectively they generate roughly $18 billion a year in revenue scoring borrowers on 20 to 30 variables. AI underwriting models evaluate over 1,600 (data from Upstart). UPST also publishes data showing 44% more approvals at the same loss rate as traditional models, with 53% fewer defaults and 36% lower APRs. At a time where mortgage rates have skyrocketed close to 7%, every basis point matters for the consumer borrowing for a first time home.

92% of Upstart loan decisions are now fully automated, made in minutes versus three to five days for traditional underwriting. The CFPB is pushing for less discriminatory alternatives to FICO, and the EU AI Act classifies credit scoring as high-risk, requiring transparency. Both of these are regulatory tailwinds supporting explainable machine learning models over legacy bureaus using a black box. This layer is disproportionately valuable, because whoever owns the scoring engine owns the yield curve of the entire stack above it. Nonetheless, it is one where moats have to be proven, as rapid advancements in AI mean “anyone” can spin up a scoring model with enough resources and time.

Layer 4: Capital and Funding

Capital post-COVID is abundant. Private credit has swelled to $3.5T in AUM, and is projected to reach $5T by 2029 according to Morgan Stanley, despite current challenging conditions. DeFi lending TVL sits between $5B and $78B, and represents roughly half of all DeFi activity. Non-traded perpetual BDCs grew from 0 in 2021 to over $200B. In this era of plentiful capital, what is most important is the ability to direct money intelligently. This is why the capital layer, despite its enormous size, is structurally subordinate to the intelligence layer above it and the infrastructure layer below it.

Private credit shops like Ares, Blue Owl, and Golub are significant allocators, but they depend on upstream scoring and downstream rails to deploy efficiently. On the DeFi side, Aave commands the dominant liquidity position, with more than half of lending borrows, while protocols like Maker, Morpho, Maple and Kamino compete for what remains.

Layer 5: Infrastructure

Infrastructure is the second chokepoint in the stack. If you own the charter or the settlement rail, everyone pays you a toll. According to management, SoFi’s bank charter reduced its cost of funds by 170 bps, reducing its annualized interest expense by over half a billion. Figure has processed over $50B in total transactions on its Provenance blockchain at an origination cost below $1,000 per loan, compared to the ~$11k average on traditional rails. Blockchain settlement finality clocks in at a few seconds versus roughly 28 hours for traditional wires

SoFi’s Galileo and Technisys stack and platforms like Blend Labs provide the remaining lending-as-a-service plumbing. Cross River Bank, the invisible partner bank behind dozens of fintechs, has originated over $140B across more than 96 million partnership loans.

The companies that win durably will either own one chokepoint layer and be indispensable to everyone else, or span multiple layers vertically in a way that creates compounding advantages. The companies that lose will be stuck in commodity layers with no structural leverage, competing on price until their margins go to zero.

The Winners: Chokepoint Owners and Multi-Layer Compounders

SoFi — The Full-Stack Compounder

SoFi is the only company that operates across four of the five layers:

It originates consumer and mortgage loans directly.

It distributes lending infrastructure to third parties through Galileo, which powers roughly 160 million enabled accounts.

It underwrites loans using proprietary risk models focused on willingness to pay, ability to pay, and stability.

It sits on a bank charter plus has the Galileo and Technisys core banking stack at the infrastructure layer.

SoFi reported record revenue of $3.6B in 2025, up 38% from 2024, with 13.7 million members and 20.2 million financial products on the platform. Management guided 2026 to $4.7B in revenue and $1.6B in EBITDA. The business is not just growing topline but is doing so very profitably with 34% margins. The charter alone saves 170 bps on funding costs by allowing SoFi to fund loans with deposits rather than wholesale markets.

SoFi is building something that resembles the AWS of lending, aka a platform that both competes with and enables other lenders. Galileo is being positioned as a billion-dollar revenue engine in its own right. Technisys, which was acquired for $1.1B in 2022, provides the core banking layer that third-party institutions run on. The charter is the structural moat that most fintech lenders cannot replicate, though they are trying: the OCC received 14 de novo charter applications in 2025 alone, signaling that the race to own the infrastructure layer is accelerating.

Upstart and Pagaya — The Intelligence Layer

Ironically, you do not have to be a lender to win in lending. Upstart and Pagaya are two companies that serve as the underwriting engine that lenders cannot outperform in-house, instead of relying on their own balance sheet. This is the picks-and-shovels thesis applied to credit decisioning.

Upstart’s models approve 44% more borrowers at the same loss rate compared to traditional FICO-based underwriting, generate 53% fewer defaults, and produce meaningfully lower APRs for borrowers. Nearly all new originations on the platform are now fully automated, reducing the need for human involvement. That is a different operating model entirely to legacy consumer credit underwriting.

Pagaya occupies the same layer but faces a harder market reality. Rather than originating loans, Pagaya licenses its AI underwriting engine to banks. Since its founding in 2016, the company has assessed roughly $2.6T in cumulative loan applications across 31 bank partners. The structural positioning is sound: Pagaya does not need borrowers to know its name, it needs banks to depend on its scoring. But the market is not rewarding the thesis today. Q4 2025 network volume grew just 3 percent YoY, revenue missed consensus, and forward guidance came in below expectations. The stock lost nearly a quarter of its value in a single session. The intelligence layer is only as valuable as the credit cycle allows it to be, and when partner networks see rising defaults, even good AI cannot outrun deteriorating collateral.

The broader point still holds though – FICO is a single snapshot derived from a narrow set of historical variables. As consumers’ financial situations get more complex and multifaceted, AI underwriting systems will become even more mission critical. Unlike FICO these systems learn and improve with every loan they score.

Figure — The New Rails

Origination costs $11k per loan on traditional rails and through MERS. Origination through Figure’s stack, which includes the Provenance Blockchain and DART, reduces that to $717. These new rails are the infrastructure that made lending an order of magnitude cheaper.

Figure has originated over $21B in home equity products (mostly HELOCs) on Provenance, with more than $50B in total transactions processed on the chain. Q4 2025 origination hit $2.7B, up 131% YoY. The company holds over 180 lending licenses and SEC broker-dealer registration, giving it the regulatory surface area to operate at scale. It also has >300 white label lending partners and has added them at a 1/day cadence since its S-1 last September. Revenue has increased from a $28.5M quarterly run rate in 1Q23 to $146.8M today

Figure’s core business doesn’t have much to do with crypto, yet the stock trades like Bitcoin. Its settlement is a cost-structure narrative, with finality in seconds versus over a day. Origination is a fraction of the traditional cost. Securitization savings of >100 bps across the loan lifecycle, which at the scale of the $3T annual securitization market means over $30B in potential cost reduction.

Aave — The DeFi Chokepoint

Aave commands more than half of the DeFi lending market. Liquidity begets liquidity and borrowers continue to skew towards where the deepest pools are (network effect). It has surpassed $1 trillion in cumulative loans originated. The protocol crossed $1T in cumulative loan volume last month.

What makes Aave structurally interesting beyond its DeFi dominance is Horizon, its institutional lending arm. Horizon has attracted $580M in deposits and is targeting over $1B in 2026. This is the bridge between DeFi liquidity and traditional credit demand. If Aave can channel on-chain capital into institutional-grade lending products, it becomes a funding layer for traditional lenders, unlocking a much larger TAM than retail DeFi alone.

DeFi lending also has a structural risk advantage that gets underappreciated. Overcollateralization ratios in DeFi run between 150%-180%, compared to 50%-70% in traditional peer-to-peer lending. Bad debt in DeFi comes primarily from oracle or technical failures, not creditworthiness defaults.

Affirm — Distribution Lock-In

Affirm has won BNPL by becoming embedded in merchant checkout infrastructure. Its detractors focus on consumer credit risk, but that misses the structural point. Affirm is not really a consumer lender in the traditional sense. It is a distribution rail for credit at the point of sale. The merchant integration is the moat. Given BNPL is projected to cover 13% of all digital transactions, the platform embedded in checkout at scale captures a structural toll on commerce itself.

The Losing Positions: Four Structural Failure Patterns

We are deliberately not naming the companies that fit these patterns. If you are an investor or operator in lending, you already know who they are. What matters more than the names is understanding why these structural positions are losing, because the same patterns will claim new casualties in the next cycle.

The Balance-Sheet-Only Lender

These are companies whose only competitive advantage is access to capital. They originate loans using traditional underwriting, fund them on their own balance sheet, and have no proprietary technology layer. They are dumb pipes for money.

In a world where private credit AUM has reached $3.5T and is heading toward $5T, capital is not scarce. Intelligence and infrastructure are. These companies compete on price alone, which compresses margin to zero in every rate cycle and causes them to take outsized risk. These lenders inevitable start extending credit to very risky companies, causing them to suffer when the cycle turns.

Players here tend to be legacy consumer lenders, sub-scale banks, and fintech lenders that never built a technology moat beyond their initial loan product. When capital is commoditized, lending on your own balance sheet without a technology edge is just a slow way to give your equity to borrowers.

The CeFi Casualty

The centralized crypto lending platforms that imploded in 2022 were not victims of a bear market. They were victims of the oldest failure mode in lending: running maturity mismatches, commingling customer funds, and lending against illiquid collateral without transparent risk management.

DeFi protocols that enforce collateral discipline programmatically (through smart contracts with visible on-chain collateral ratios) did not blow up. CeFi platforms like that relied on human judgment and opaque balance sheets did. Any lending platform — crypto or traditional — that asks you to trust its balance sheet instead of showing you the collateral is making the same structural bet that already failed once.

The Ghost Protocol

There is a category of DeFi lending protocol that is technically alive and structurally dead. They launched, attracted initial total value locked through token incentives, and then stagnated as the incentives faded. Their code works. Their TVL floors are nonzero. But their usage curves are flat or declining, and they have no clear path to organic demand.

The reason is that DeFi lending exhibits extreme power-law dynamics. Liquidity concentrates around network effects — Aave’s commanding market share is proof of this. Protocols that cannot reach escape velocity get stuck in a structural no-man’s land: too small to attract organic liquidity and the integrations that come with it, too large to shut down gracefully. Their TVL decays slowly as yield-seekers migrate to dominant platforms, but the decay is constant and irreversible. These are zombie protocols sustained by the sunk cost of governance tokens.

The Originator Who Missed the Platform Shift

Some companies built strong origination businesses in a previous cycle but never developed platform capabilities. They do not possess API distribution, no embedded finance partnerships, no technology licensing. They originate well but cannot export their capabilities.

As lending becomes modular, the ability to be a component in someone else’s stack is as important as direct origination. Companies that can only lend directly to end borrowers are capped by their own distribution reach. Companies that can also power lending for others have uncapped TAM. The pure originators often have good unit economics but flat growth curves, because their addressable market is limited to their own brand and channels. In a modular stack, being a great lender is necessary. Being a great lender that other lenders plug into is the actual winning position.

The Ones to Watch

The winners above are consensus or near-consensus. The companies below are not. They have structural characteristics that could make them chokepoint owners, but they have not yet proven it at scale. These are the names worth tracking.

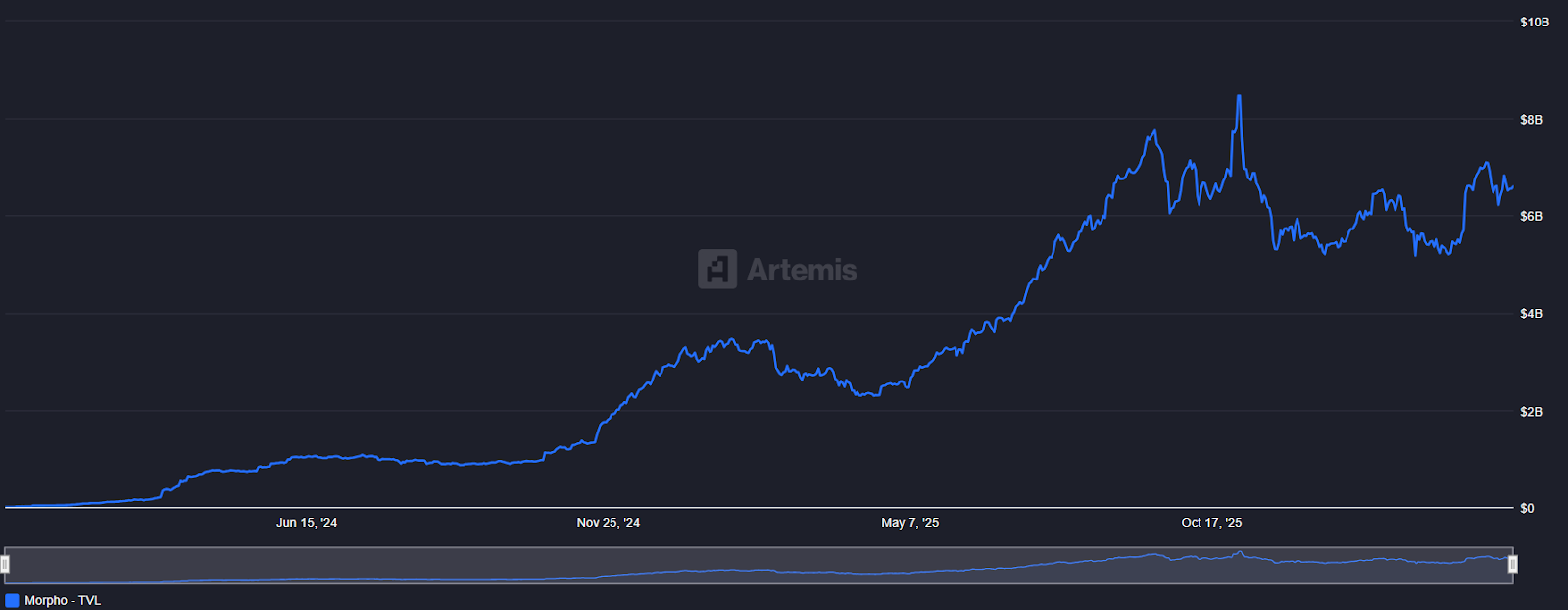

Morpho

Morpho has reached $6.6B in TVL with 164% YoY growth, and a market cap north of $800M. Its structural thesis is distinct from Aave’s. Where Aave is DeFi’s commercial bank (a monolithic lending pool) Morpho is building a modular lending layer that allows institutional participants to configure customized lending markets with their own risk parameters, collateral types, and interest rate models. If the lending stack is truly becoming modular, Morpho is the lending-as-a-service protocol for the on-chain layer.

Maple Finance

Maple originated $11.3B in total loans in 2025 across 65 active borrowers, with AUM growing 767% from $516M to $4.6B. It is targeting $100 million in ARR in 2026. Maple is one of the few protocols seriously attempting to make real-world corporate lending work on blockchain rails, by bridging institutional credit demand with on-chain capital and settlement infrastructure. The massive AUM growth is a signal that institutional appetite for on-chain credit markets is moving from theoretical to operational.

Cross River Bank

Cross River has originated over $140B across more than 96 million partnership loans since 2008. It is the bank behind Affirm, Upstart, and dozens of other fintech lenders. It is reportedly exploring an IPO. Cross River is an “invisible” bank, serving is the infrastructure layer that a significant share of fintech lending runs on. As the partner bank model matures, Cross River’s position gives it leverage that no single fintech lender can replicate. To win, the bank needs fintechs to be unable to lend without it.

The Charter Land Grab

The OCC received 14 de novo bank charter applications in 2025 alone — nearly equal to the previous four years combined. Total fintech charter filings have hit an all-time high of 20. Affirm, Stripe, and Nubank are all pursuing charters. These firms see a charter as the endgame of the rebundling thesis.

Companies that started as technology layers are now acquiring the regulatory infrastructure to capture full-stack economics. The charter is lending’s equivalent of a cloud region, in that it is a) expensive to build, b) impossible to route around, and c) a permanent structural advantage once obtained.

The math is clear: every 1% improvement in cost of funds translates to a mid-single digit improvement in pre-tax return on equity. For a scaled player, the charter advantage is enormous. For a sub-scale player, however, the charter can be a trap. They incur all the regulatory cost, examination burden, and capital requirements with none of the scale economics to justify them. The charter is a supercharger only for companies that already have volume.

The Lending Stack in 2030

If you take one framework away from this piece, it should be these three questions. They work for any lending company, whether it is public, private, or on-chain.

The first is: which layer does it own? Origination and undifferentiated capital provision are commodity layers. Margins there compress with every cycle. AI underwriting, blockchain settlement, and bank charters are chokepoint layers whose issues compound. If a company is stuck in a commodity layer with no path to a chokepoint, the economics will grind it down over time regardless of how good the team is.

The second is: is it a platform or a product? A product serves end borrowers and scales linearly with its own distribution. A platform enables other lenders and scales with their volume, not just its own. SoFi is both. Pagaya is pure platform. The companies that only lend directly to their own customers are capped in a way that platform businesses are not.

The third is: does it have a regulatory moat? A bank charter, 180 state lending licenses, or programmatic compliance enforced through smart contracts. Regulation in lending is not overhead. It is infrastructure. The companies that figured this out early have an advantage that takes years and significant capital to replicate.

By 2030, lending will look less like banking and more like cloud computing. A small number of full-stack platforms will operate across multiple layers, compounding advantages at each one. SoFi is the clearest candidate in TradFi. Aave is the clearest on-chain. Around them, a larger number of specialized layer providers will plug in via APIs and on-chain rails, each owning a specific function and charging for access.

The $348 trillion global debt market at less than 20 basis points of fintech penetration is not an opportunity for hundreds of lenders. It is an opportunity for a dozen platforms that everyone else builds on.

Disclosure: This material is provided for informational purposes only and does not constitute investment advice, financial advice, trading advice, or any other form of advice. The views expressed are those of the authors and should not be relied upon as a recommendation to buy, sell, or hold any asset. The authors or affiliated entities may hold positions in the assets discussed. You should conduct your own research and consult appropriate financial professionals before making any investment decisions.