The Anxiety Economy: Why Trading Explodes

The thesis behind the next decade of financial markets

TLDR:

An entire generation has done the math on passive investing and decided it’s not enough. Financial anxiety will replace greed as the primary driver of trading.

The gap between forming a market opinion and trading on it is collapsing to zero.

AI will narrow the knowledge gap between retail and institutions, but the median active trader will continue to underperform the market.

Winners: Robinhood, Coinbase, IBKR

Losers: Legacy brokers selling patience to a generation that wants speed

The Math

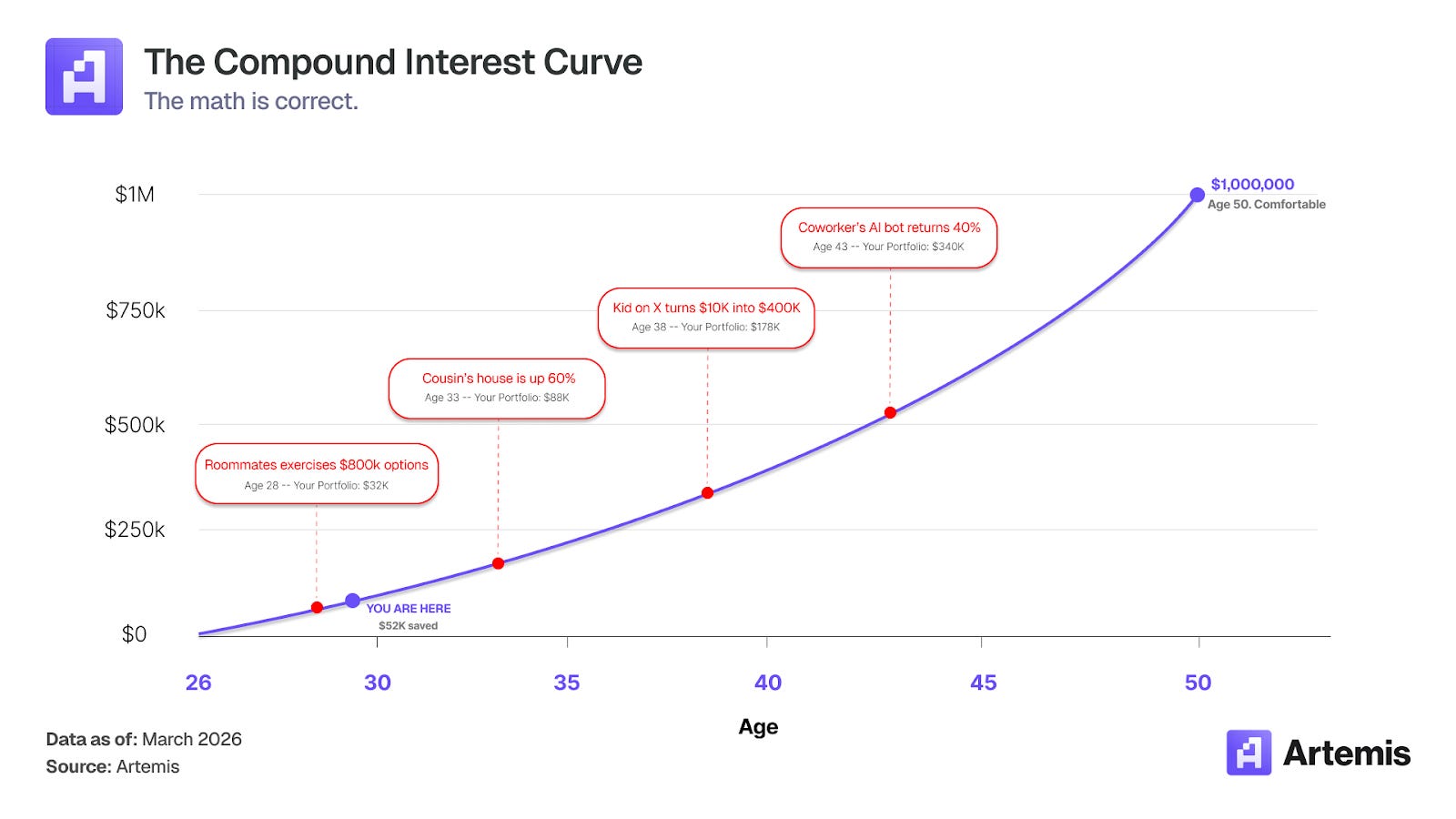

$1,200 a month.

8% annual returns.

24 years.

That’s what it takes to hit a million dollars starting from zero at age 26. That puts you at 50.

Open your calculator app and run the numbers yourself.

You’re making $90,000 a year, but after taxes, New York City rent and student loans, you can realistically only save $1,200 a month. Put that in the market index fund for 8% annually and you’ll reach $220,000 in ten years – in twenty, about $710,000. If you’re consistent and don’t hit any setbacks, you might reach a million at 50.

That’s the base case if you do everything right.

Then you check your phone. Your college roommate posted last week about exercising $800,000 in startup options. Your cousin bought a house in 2019 and it’s up 60%. A 24-year-old kid on X you’ve never met turned $10,000 into $400,000 on memecoins in a few weeks. You know these are outliers and most people don’t post their losses. That doesn’t matter. It still feels like you’re falling behind.

So you start trading.

This is the Anxiety Economy – an era where financial anxiety becomes the primary demand driver of an entire category of products. It’s built for people who’ve done the math and realized that playing it safe won’t get them to where they want to be.

The consensus explanation for why trading volumes will grow – better products, lower fees, more asset classes, more AI tools, and better user experience. All true, but incomplete.

The deeper driver is emotional. An entire industry is being built to serve that feeling: I am behind and I need a faster way to catch up.

The Proof

You’re not imagining things.

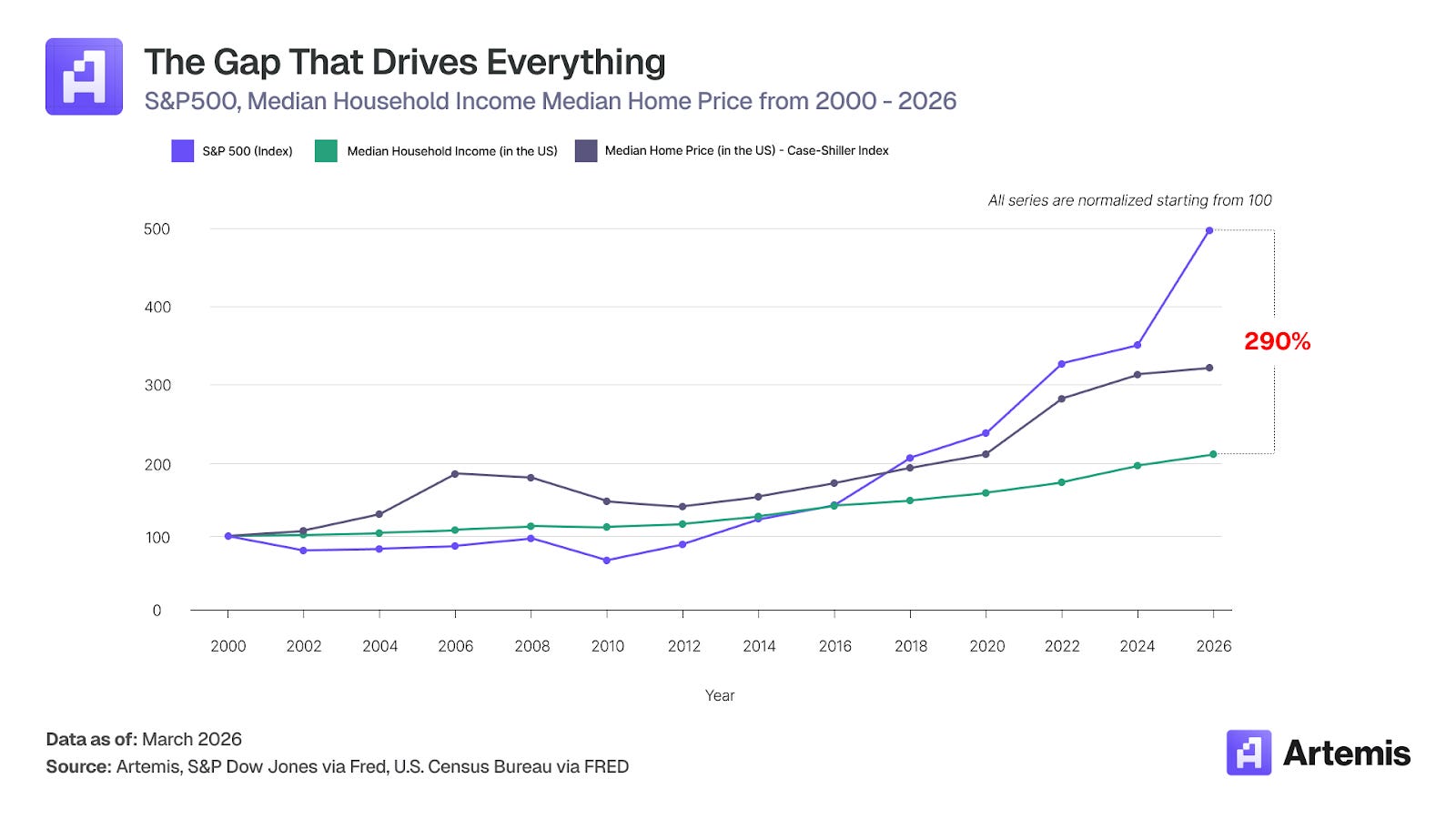

Since 2000, the S&P 500 index has returned around 400%, home prices have risen approximately 230%, but median wages in the United States have only grown about 110%. If you were in the market, your wealth compounded. If you weren’t, you fell further behind.

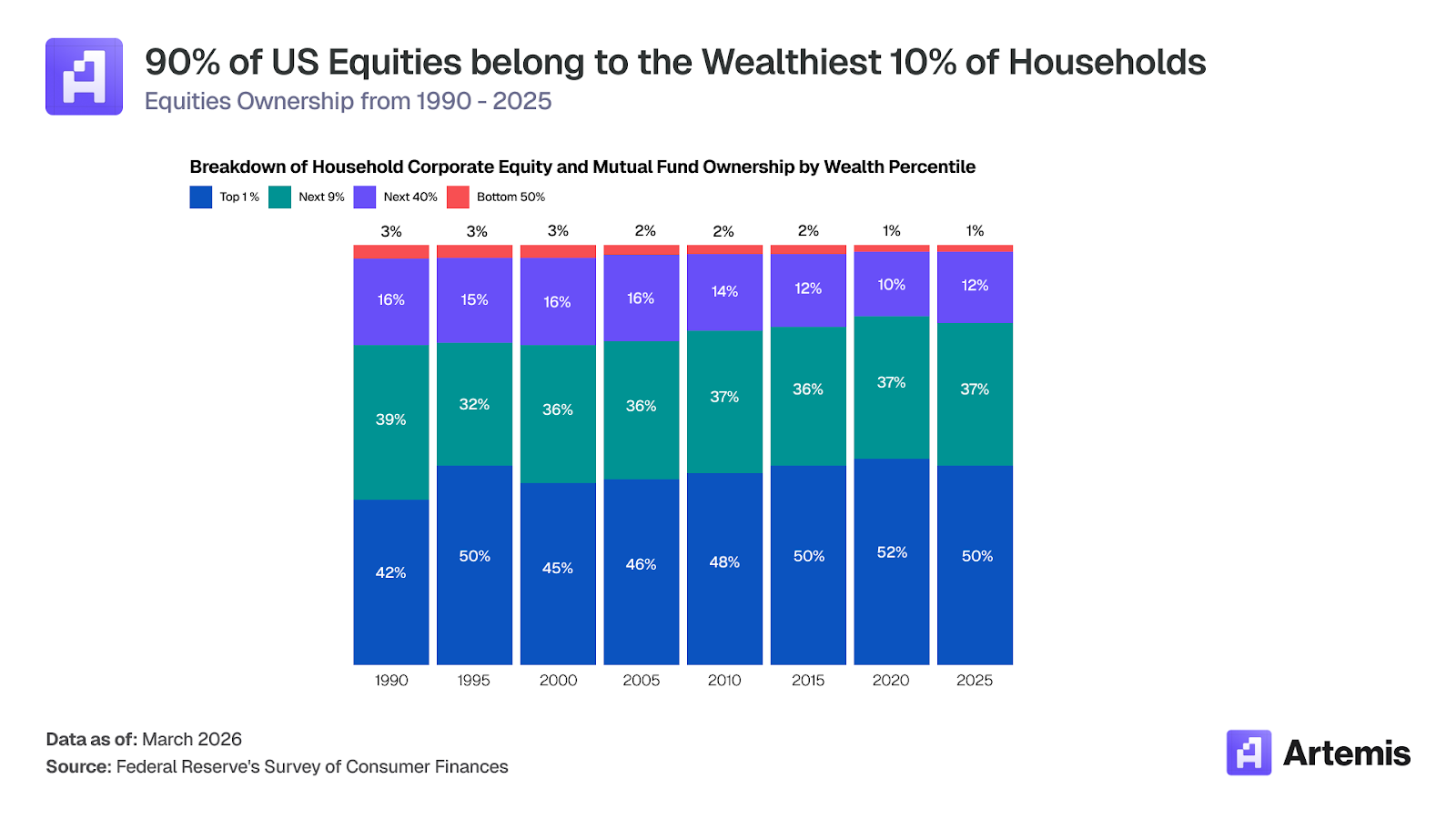

The top 10% of American households now own 87% of all US equities, up from 82% in 1989 and the wealth gap is accelerating.

A recent study conducted by Amerisleep found that 49% of Americans lie awake at night due to financial stress. For Gen Z, that number is 69%. When saving and investing doesn’t feel safe, people start gambling.

And yet, passive investing works.

If you’re in the market, you get the market’s 8% annual returns. The problem isn’t the math but where most people start. The bottom half of American households own less than 1% of all equities. You’re compounding 8% on $15,000 while someone else is compounding 8% on $1.5 million. Same returns. Completely different lives.

This is why the old advice sounds right and empty at the same time.

“Be patient.”

“Buy the index.”

“Dollar-cost-average.”

“Let time do the work.”

It’s good advice for building wealth slowly, but it doesn’t work for someone trying to close a wide gap within their lifetime.

Some people have started calling this financial nihilism – the idea that the system is so broken you might as well gamble. That framing misses the point. These people aren’t giving up. They’re trying harder than ever because the safe path isn’t fast enough.

This is why the distinction between investing and trading matters.

Investing is rational and works on long time horizons. Trading offers a chance at asymmetric upside on a compressed timeline. The products that exist today – options, perpetuals, memecoins, prediction markets – each offers a different flavor of that upside.

The expected value for most of these trades is, of course, negative. We know that. But when the baseline path feels too slow, people take bigger bets.

Patience used to feel like virtue. For most people now, it feels like something they can’t afford.

The Product

Anxiety is the demand side. Let’s talk about the supply side.

In 2015, acting on a market view required the following:

Open a brokerage account (three days for approval).

Fund it (two days for transfer). Wait for market hours.

Pay a $9.99 commission.

You were only allowed to buy whole shares (i.e. If you wanted Amazon at $500, you needed $500).

The waiting was the point. By the time you could act, the conviction and edge were gone.

In 2026, the boundaries are being lowered. Commission-free trading removed the cost barrier. Fractional shares removed the capital barrier. Mobile apps removed the location barrier. 24/7 crypto markets removed the time barrier. AI is beginning to remove the analysis barrier.

Every major innovation in financial products did one thing. It removed another barrier between forming a market opinion and trading on it.

Today, the final barriers are asset class fragmentation, settlement delays and geographic restrictions. These barriers will be removed too.

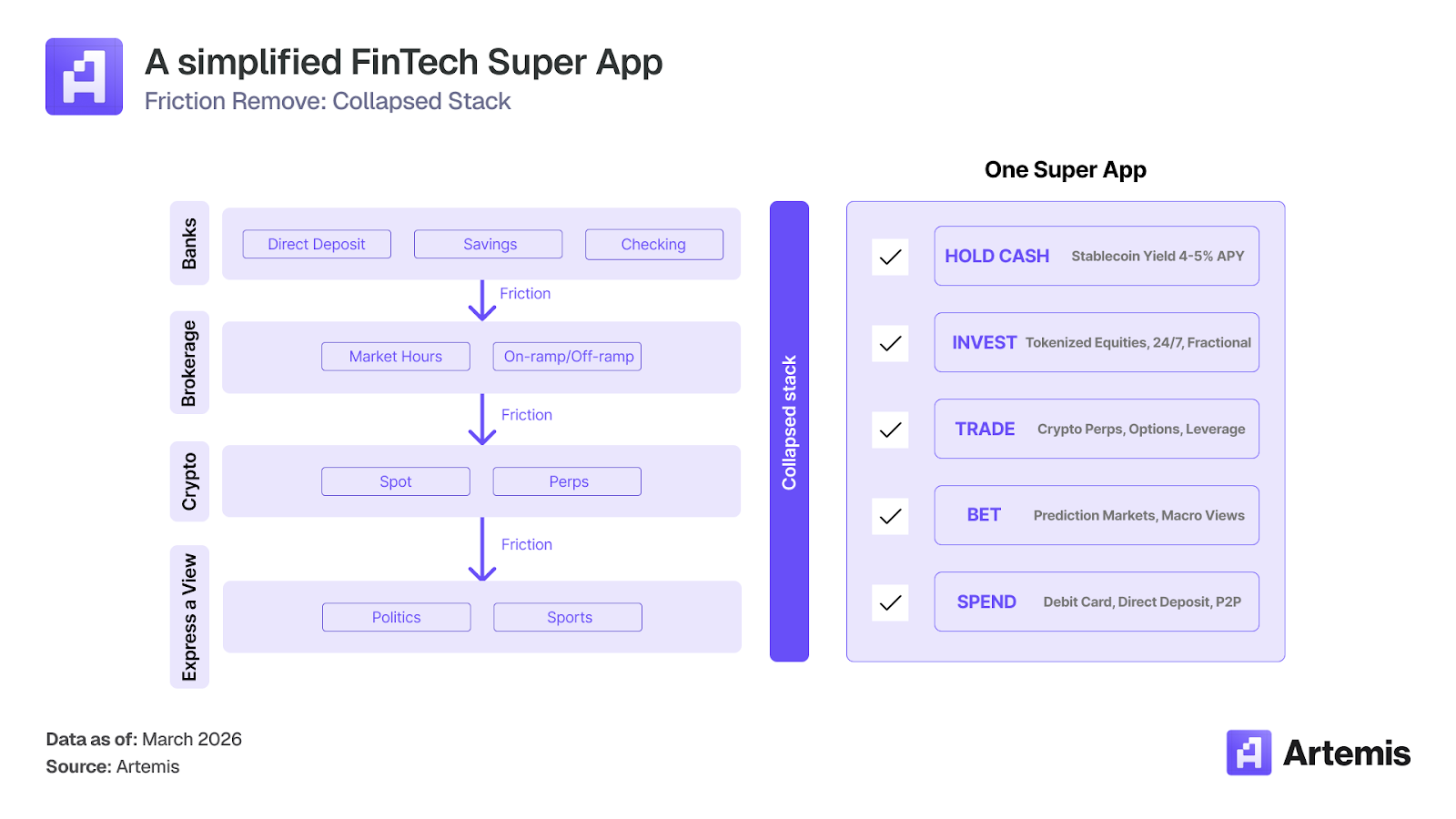

You’ve already seen it happen in your own account. You opened a brokerage account to auto-invest into an index fund. Slowly, it started offering more: fractional stocks, options, crypto, leverage, a prediction market on the Fed, tokenized equity markets open on weekends.

Each step feels small. What used to be a clear line between “investing” and “trading” became another product funnel.

The next stage is obvious. Today, the experience is still fragmented. One app for stocks (Robinhood, IBKR). One for crypto (Coinbase, Hyperliquid). One for payments (Venmo). One for banking (Chase, BofA). Maybe another for prediction markets (Polymarket, Kalshi). The tools already exist, but they’re just spread across five different apps.

Fragmentation is the last form of friction. Every time you switch apps, there’s a moment where you might stop and think. A moment where your impulse fades.

By 2030, that fragmentation will collapse. The winners will hold your paycheck, your savings, your margin, your card spend, your stablecoins and your watchlist in one place.

The question is who those winners will be. To answer that, you need to see the full picture.

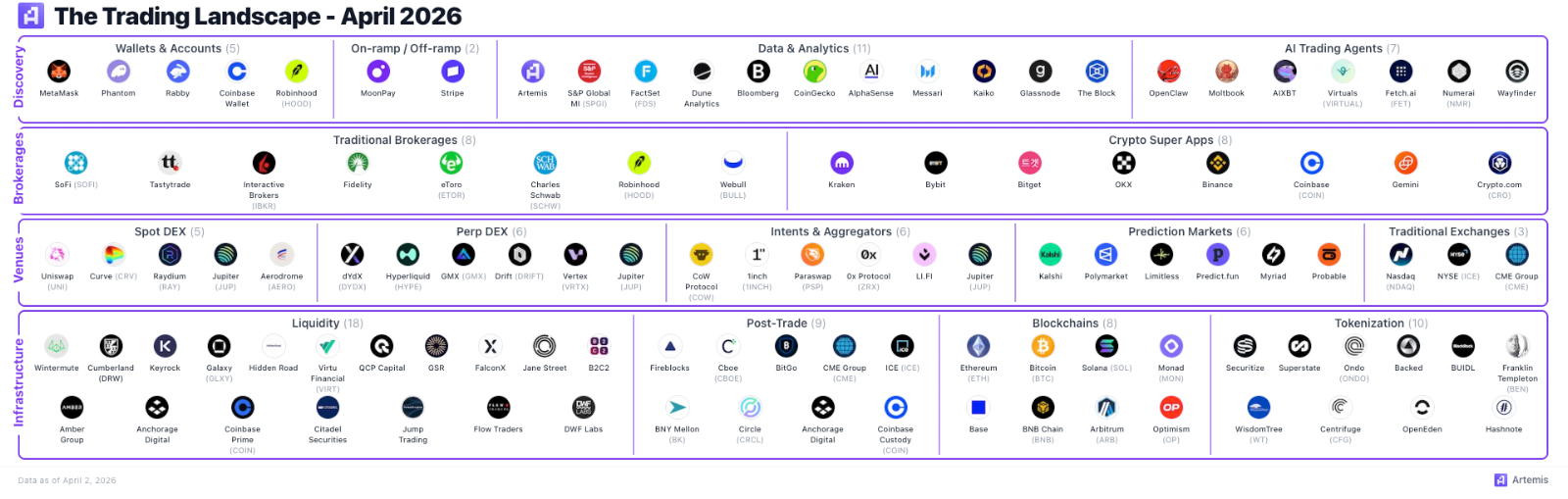

The Landscape

At first glance, the trading landscape feels crowded. There are wallets, brokerages, crypto super apps, spot venues, perp venues, aggregators, prediction markets, post-trade providers, blockchains, tokenization rails, and everything in between.

It’s simpler than it looks.

I’ve broken it down to four layers.

First: the discovery platform.

Wallets, on-ramps, data products and AI tools – this is where users check prices, get alerts, move cash, and form intent. The brokerages don’t own this layer because by the time you open Robinhood, you’ve already decided what you want to do. The opinion forms somewhere else. On X, in an Artemis dashboard, in a Claude conversation. This layer owns the moment before the trade.

Second: the brokerages.

Brokerages and crypto super apps – this is where intent turns into action. You tap buy, set your size and confirm the order. These companies will want to own the user’s capital, trades and spending. The more money they hold, the harder it is to leave.

Third: the venue.

Exchanges, perpetual venues, aggregators, prediction markets and tokenized exchanges – this is where the transaction actually settles. As more assets trade globally and around the clock, this layer will capture more flow.

Fourth: the infrastructure.

Liquidity, post-trade systems, blockchains, and tokenization infrastructure – this layer sits furthest away from the user. It doesn’t care who wins the app war. It earns from the volume.

The biggest winners will be the app people open first, the platform that holds the money, and the venue that executes the trade. Here’s who I think that is.

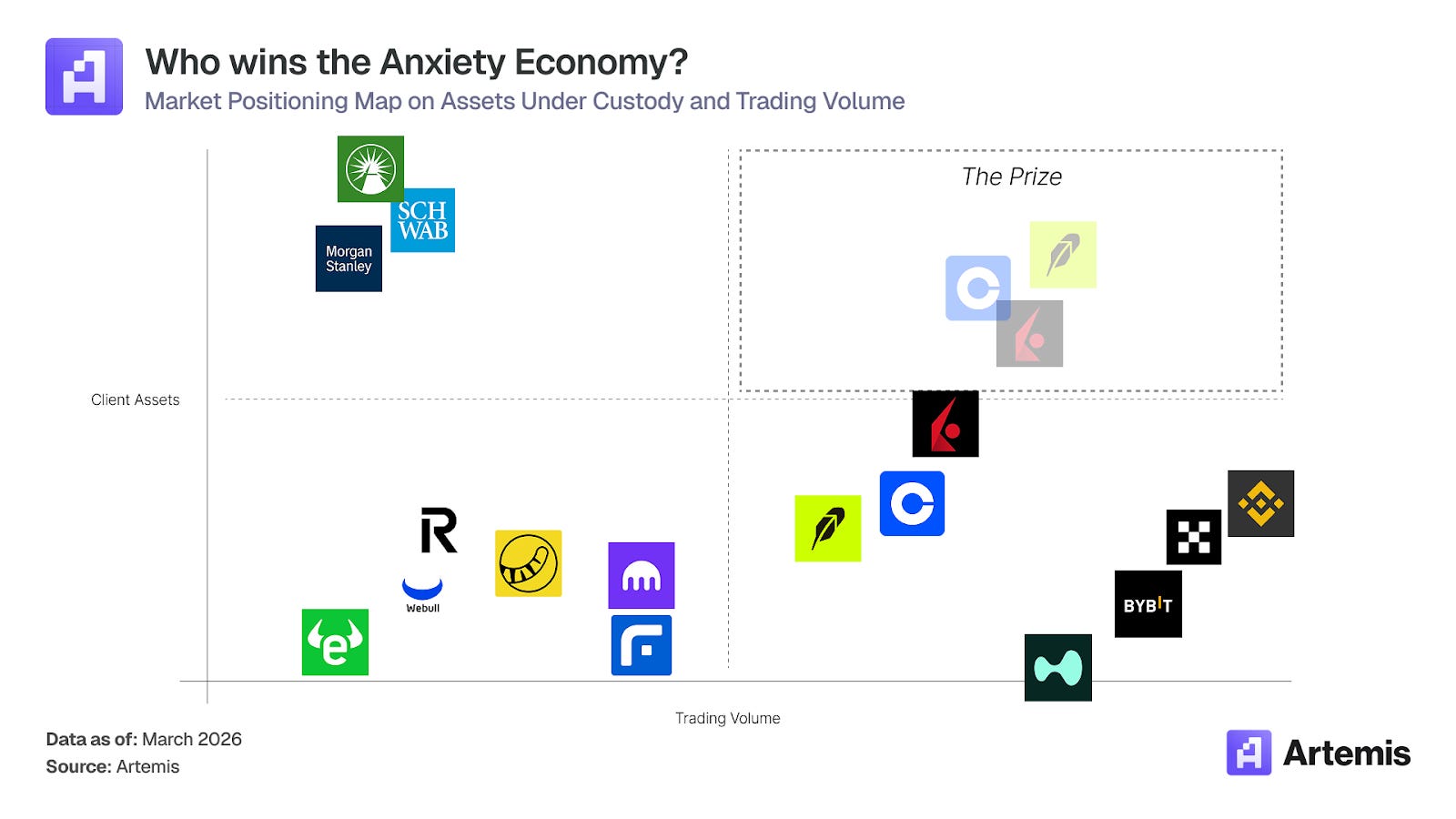

Where Value Accrues

The winners will be the firms that make it easiest for users to act on the feeling.

Robinhood is the clear winner. Robinhood understood the emotional needs before the product needs. It was built from day one for people who feel behind – commission-free trading, fractional shares, a clean interface that made finance feel accessible instead of intimidating. Now it’s layering on prediction markets, the Gold Card, crypto, retirement accounts. Their product velocity is the fastest in fintech. In Q1 2026, they launched Cortex, an AI assistant that lets you buy, sell and research in plain English. They also unveiled a Platinum Card. They also acquired a CFTC-licensed exchange to run their own prediction markets infrastructure. Gold subscribers hit 3.9 million, up 77% year over year. No other fintech is shipping this fast. Robinhood wins because they realized that volume growth is driven by anxiety.

Coinbase is best positioned in the intersection of consumer finance and 24/7 internet-native markets. It owns the crypto on-ramp and the infrastructure underneath it. USDC is becoming a default savings and settlement instrument. Base is attracting developers and transaction volume. Revenue is diversifying away from volatile trading fees toward subscriptions, stablecoin interest and infrastructure services. Stablecoin revenue alone hit $332 million in Q4 2025, up 38% year-over-year. USDC market cap reached an all-time high of $76 billion. Base is now profitable. They now have 12 products generating over $100 million annually. Subscriptions and services account for 41% of revenue. Coinbase wins because even when you stop trading, your money is still on their rails.

Interactive Brokers (IBKR) has potential to be a winner as well. IBKR provides access to over 170 markets in 40 countries. They added over 1 million net new accounts in 2025, bringing the total to 4.4 million. Client equity hit $780 billion. They’re now letting US clients fund brokerage accounts with stablecoins. They also launched a Visa card linked to your brokerage account, and redesigned their mobile app with AI-driven market insights. They’re finally working on the user experience. If IBKR can make the product feel as simple as Robinhood without losing the depth, they win the high-intent end of the Anxiety Economy. The traders who’ve outgrown Robinhood and need somewhere serious to go.

ICE (Intercontinental Exchange, parent of the NYSE) is the toll collector. Trading volume is a tax base. ICE owns the collector. If more of the world becomes tradable – more asset classes, more hours, more geographies – ICE earns the take rate on this expanding base. ICE posted record trading volumes in 2025. ADV up 14% year-over-year, $9.9 billion in revenue. In the first half alone, 1.2 billion futures and options contracts traded. Municipal bond volume was up 27%. MBS volume doubled. ICE just needs the app war to produce more transactions and they will win.

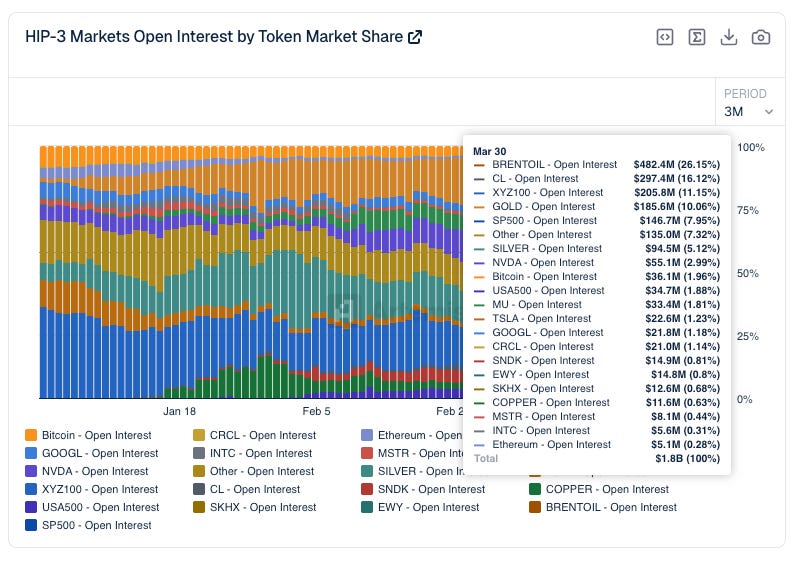

Hyperliquid is a pure venue bet. It’s the decentralized exchange that’s starting to look like something bigger. When oil prices spiked on a weekend and traditional markets were closed, traders went to Hyperliquid’s HIP-3 for price discovery. HIP-3 daily volumes in WTI-linked contracts exceeded $2 billion on March 23 and open interest hit $1.8 billion in late March 2026. Oil volume on the platform grew over 100x in six months. If tradable assets keep expanding beyond traditional market hours, venues that never close have a structural advantage.

The losers are the legacy brokerages. Companies that don’t innovate will be eliminated. If they continue selling safety and long-term planning to a generation that wants speed and hope, they’ll be able to keep the Boomers’ assets but not the next hundred million traders (Gen Zs and Gen Alphas).

On the watch list:

Webull – built a strong product for active traders – real charting, extended hours and an easy to use mobile experience. The risk is that it’s stuck in the middle: too complex for beginners and not deep enough for professionals.

eToro – one of the first platforms to make trading feel social. Copy-trading, community feeds and the idea that you could follow someone who knows more than you. In the Anxiety Economy, that instinct – someone who you think figured has figured out the market is only going to become stronger.

SoFi – still one of the best examples of financial services being bundled (banking, lending, credit and investing) into a single consumer brand. My worry is positioning. When people think of SoFi do they think about “trading” or “refinancing their student loans”. They have a broad suite of products but are shallow.

Every company on this list grows when people trade more. By now, you know why they will.

The Edge That Isn’t

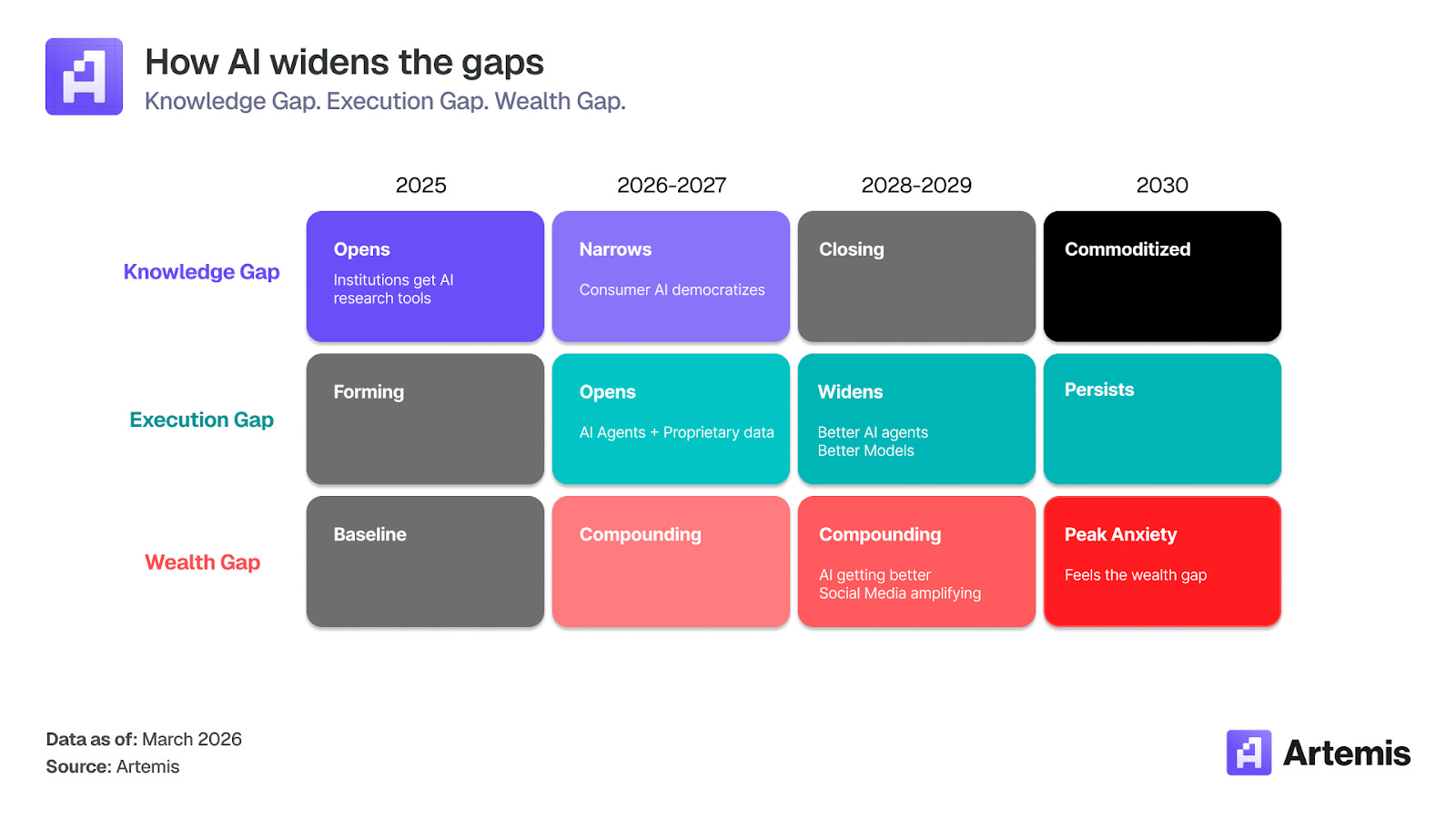

AI will reshape trading from a technical perspective, but the larger effect will be psychological.

Picture this: before the market opens, an AI brief summarizes your portfolio, flags a catalyst, and explains what CPI or tariffs or earnings could mean for your positions. By the time you pour your coffee, you have a thesis. It feels like you know something.

And in some ways, you do. The knowledge gap between retail and institutional is narrower than it’s ever been. A few years ago, institutional investors had Bloomberg terminals and teams of analysts parsing SEC filings, supply chain data and earnings transcripts before the market opened. Retail had Google.

Now everyone has Claude, Perplexity and Artemis, specialized finance copilots that can synthesize eight quarters of earnings data and identify competitive divergences in thirty seconds. The pure information edge that used to cost $24,000 a year in Bloomberg subscription is compressing fast. Bloomberg’s moat still exists – proprietary data, the chat function everyone on Wall Street is addicted to, but the gap between a hedge fund analyst and a regular guy (with an AI subscription) is narrower than it’s ever been.

That’s the good news.

What hasn’t changed is that institutions still have better infrastructure, routing, tooling and systems. Their algorithms execute trades, adjust sizing by volatility regime and route orders to the tightest spread at that millisecond. They don’t sleep or get emotional. Retail will get a taste of this through Robinhood’s AI features and Coinbase’s smart routing, but it’s not the same product. This matters because small edges in execution, repeated thousands of times across years, compound into large differences in outcome.

Meanwhile, social media makes sure you see every winner and every person telling you how they did it.

That brings us to the part nobody in the industry wants to discuss openly: the median active retail trader still underperforms index funds. That has been true for decades. Every study confirms it. AI hasn’t changed this yet.

So the real effect of AI in retail trading is more subtle and more commercially valuable. It turns uncertainty into confidence. You feel informed, so you trade more. The information edge is real but the execution edge isn’t yours. The distance between these two facts is where a lot of money will be made – just not by you.

The Spread on Hope

AI creates confidence. But where does the anxiety come from?

In 2010, critics said social media was making people anxious and addicted. The platforms said they were connecting the world.

Both were right. The critics lost.

Social media makes the wealth gap visible, personal and constant. Every startup exit post, every portfolio screenshot, every casual mention of someone’s house purchase. Your brain doesn’t treat them as anecdotes, it treats them as evidence of where you stand. The answer, for most of us, is behind.

That’s the spread on hope. On one side, the feeling: I’m one good trade away from catching up. On the other, the fact that the median trader still underperforms the market. That gap is where the industry makes its money.

Every trade generates revenue. Every session generates data. The more features a platform ships, the harder it becomes to leave. Nobody in the industry will say this out loud, so I will.

The Counterargument

Now let me argue the other side. I owe you that.

Long-term investing still works.

A disciplined person in 2030 with AI portfolio management, stablecoin yield at 4-5% APY, tokenized global equities available 24/7 and prediction markets for hedging is genuinely better positioned than someone with a legacy brokerage account and a phone call to an advisor in 2015. For the person who treats these platforms as tools rather than entertainment – who uses the AI brief to understand their position before doing in-depth research – the outcomes will be meaningfully better. The index fund still works.

What’s shrinking is the number of people with the psychological space to actually stick with it. Looking at my peers, I can count on one hand how many are consistently dollar-cost averaging into an index fund. I don’t blame them. It’s an increasingly difficult path to choose and an even harder one to stay on.

Conclusion

The future of trading is a story about what happens when an entire generation decides that waiting is the riskiest thing they can do. A lot of very smart companies are building very good products for that feeling.

The uncomfortable question is whether packaging hope into a better product makes the world better or just makes certain companies richer.

I think it does both.

Special thanks to @Onchainlu, @x0wes, @mzhao8, @jinglingcookies and @jonbma for your thoughtful feedback!

Disclaimer: The authors of this content, as well as affiliates of Artemis Analytics, may have financial interests in the equities or tokens mentioned. This does not constitute investment advice or a recommendation to buy, sell, or hold any asset. The information provided is for educational purposes only and should not be relied upon for financial, legal, or tax decisions. Readers should assess their own circumstances before making any financial choices. Views expressed may change without notice, and Artemis Analytics is not liable for any losses resulting from the use of this content.*