SoFi: Mispriced at the Inflection

A bank-chartered neobank scaling profitability and diversification while trading at a valuation disconnected from its growth profile

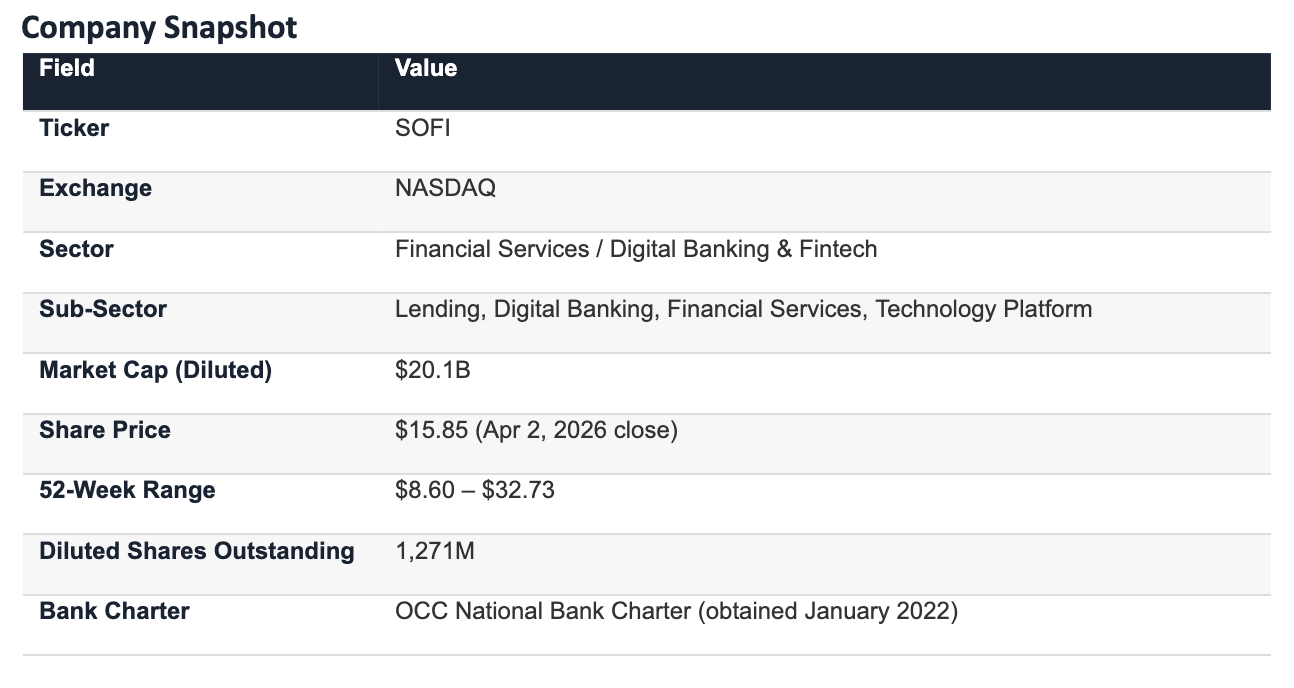

SoFi Technologies (SOFI)

Thesis Summary

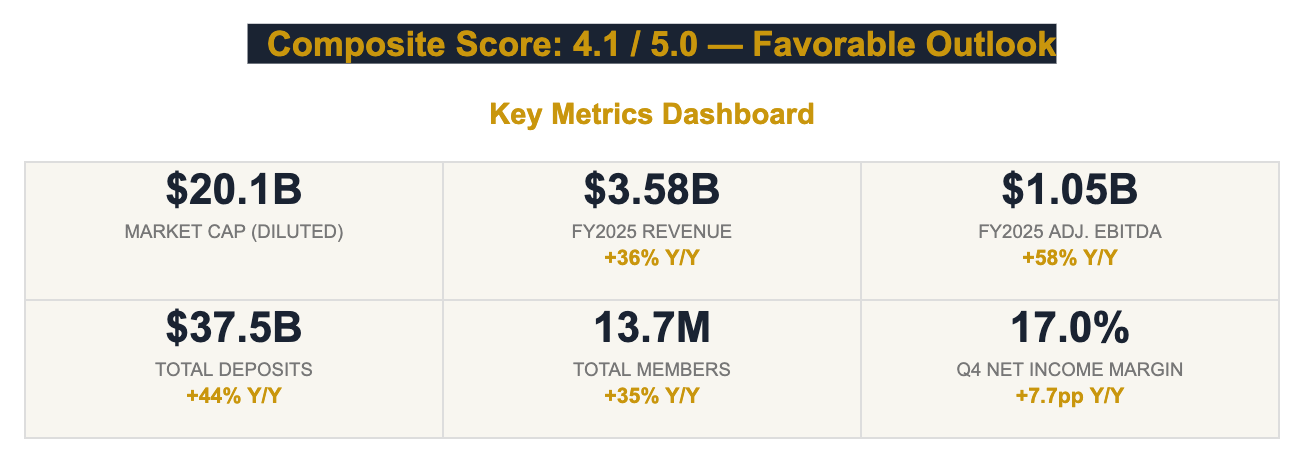

SoFi Technologies is one of the largest neobanks in the United States and one of a handful of fintechs to hold a national bank charter, providing structural advantages in cost of funding, product breadth, and regulatory positioning. The company delivered its first $1 billion revenue quarter in Q4 2025, grew members 35% to 13.7 million, and achieved nine consecutive quarters of GAAP profitability. Financial Services and Technology Platform now represent 57% of revenue and are growing 61% year-over-year, driving rapid diversification away from historical lending dependence. CEO Noto’s expansion into crypto (SoFi USD stablecoin, crypto trading), business banking, and international payments via SoFi Pay opens multiple new growth vectors. At $15.85—down 42% year-to-date and 52% from the 52-week high—the stock trades at ~10.7x FY2026E adjusted EBITDA despite guiding for 30%+ revenue growth in FY2026. The average analyst price target of $25.70 implies 62% upside. The selloff appears driven by broad market risk-off (tariff fears, macro uncertainty) rather than fundamental deterioration, creating an asymmetric risk/reward profile.

2. Company Overview

Business Description

SoFi Technologies was founded in 2011 as a student loan refinancing company and has since transformed into a comprehensive digital financial services platform. Under CEO Anthony Noto, who joined in 2018, SoFi obtained a national bank charter from the OCC in January 2022—a pivotal strategic move that enabled the company to take deposits, fund lending at lower cost, and offer FDIC-insured accounts. Revenue has compounded at nearly 50% annually from $240 million in 2018 to $3.6 billion in 2025, while the member base grew from 650,000 to 13.7 million.

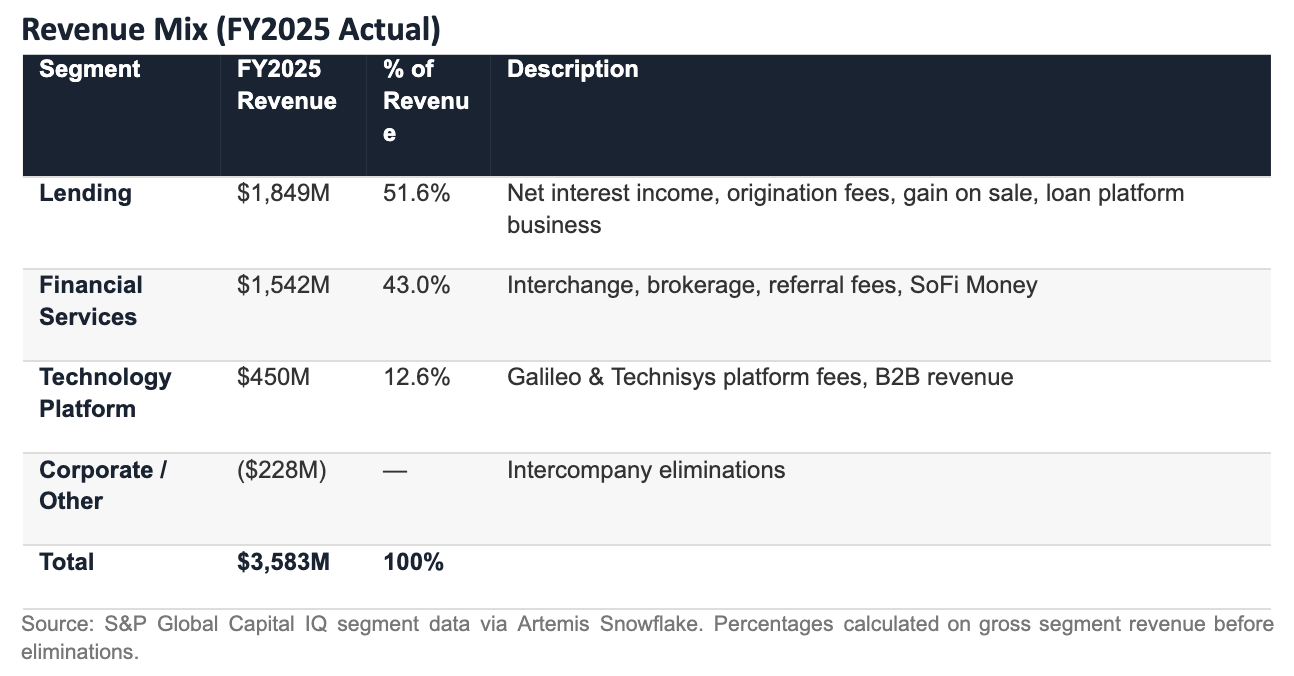

The company operates three reportable segments: Lending (personal loans, student loan refinancing, home loans), Financial Services (SoFi Money, SoFi Invest, SoFi Relay, SoFi Credit Card, SoFi Smart Card), and the Technology Platform (Galileo and Technisys, providing banking-as-a-service infrastructure to other fintechs and financial institutions globally). SoFi’s “one-stop shop” model enables members to borrow, save, spend, invest, and protect within a single integrated app, driving a 40% cross-buy rate and deepening multiproduct relationships.

In 2025, SoFi expanded aggressively into crypto—becoming the first nationally chartered bank to offer crypto trading, launching the SoFi USD stablecoin on public blockchain, and deploying SoFi Pay for international payments across 30+ countries. Business banking and institutional crypto services are planned for 2026, representing the next wave of product expansion. Nine sell-side analysts cover the stock with a consensus Buy/Hold rating and an average price target of $25.70.

Products & Services

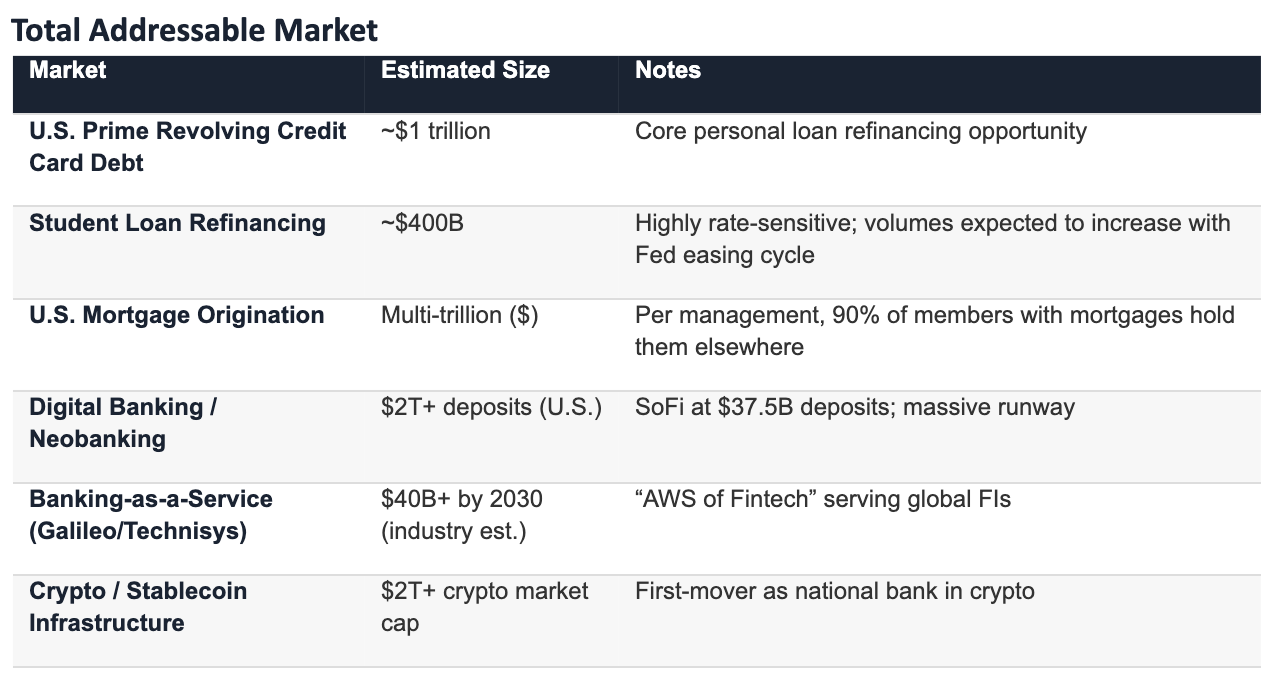

Personal Loans: SoFi’s largest lending product, targeting prime borrowers refinancing high-rate credit card debt. Per management, SoFi originates roughly 15% of total U.S. prime personal loan volume.

Student Loan Refinancing: The company’s founding product. Per company disclosures, SoFi saved members over $400 million in interest on 2025 refinances alone. Addressable market: ~$400 billion.

Home Loans: Record $3.4 billion in FY2025 originations, with Q4 running at a $4.5 billion annualized pace. Per management, 90% of SoFi members with mortgages currently hold them at other institutions.

SoFi Money: High-yield checking/savings account with up to 4.50% APY and FDIC insurance. 97% of deposits are direct-deposit customers, indicating high-quality primary relationships.

SoFi Invest: Brokerage platform offering stocks, ETFs, crypto, IPO access, private market funds, and Level 1 options. Revenue grew 2.2x year-over-year in 2025.

SoFi Relay: Free credit monitoring and financial tracking dashboard serving as the top-of-funnel member acquisition tool.

SoFi Smart Card: All-in-one debit/credit card with up to 5% grocery cashback. Per CEO Noto, built and launched in 4.5 months using the in-house tech platform.

SoFi Crypto & SoFi USD: First national bank to offer crypto trading and issue a stablecoin. SoFi USD is backed 1:1 by cash at the Fed master account with zero credit, liquidity, or duration risk.

SoFi Pay: Blockchain-powered international payments across 30+ countries including Mexico, India, Brazil, Philippines, and Europe.

Galileo (Technology Platform): Card issuing, payments, and digital banking API platform powering other fintechs and financial institutions. Known as the “AWS of Fintech.”

Technisys (Technology Platform): Cloud-native core banking platform enabling enterprise clients to modernize their banking systems. Expanding into Latin America and the Middle East.

Market Positioning

SoFi is one of the largest neobanks in the United States and one of the most comprehensive fintech platforms globally. Its national bank charter differentiates it from most digital-only competitors (e.g., Robinhood, Cash App, Chime) who rely on sponsor banks. This charter enables SoFi to offer higher APYs while maintaining healthy margins—deposits sit in an FDIC-insured account earning interest, whereas funds at non-bank competitors earn nothing while awaiting deployment. The combination of lending, banking, investing, and technology infrastructure under one roof is unique among publicly traded fintechs and positions SoFi at the intersection of multiple secular growth trends: digital banking adoption, crypto/blockchain infrastructure, and the unbundling of traditional financial services.

3. Financial Analysis

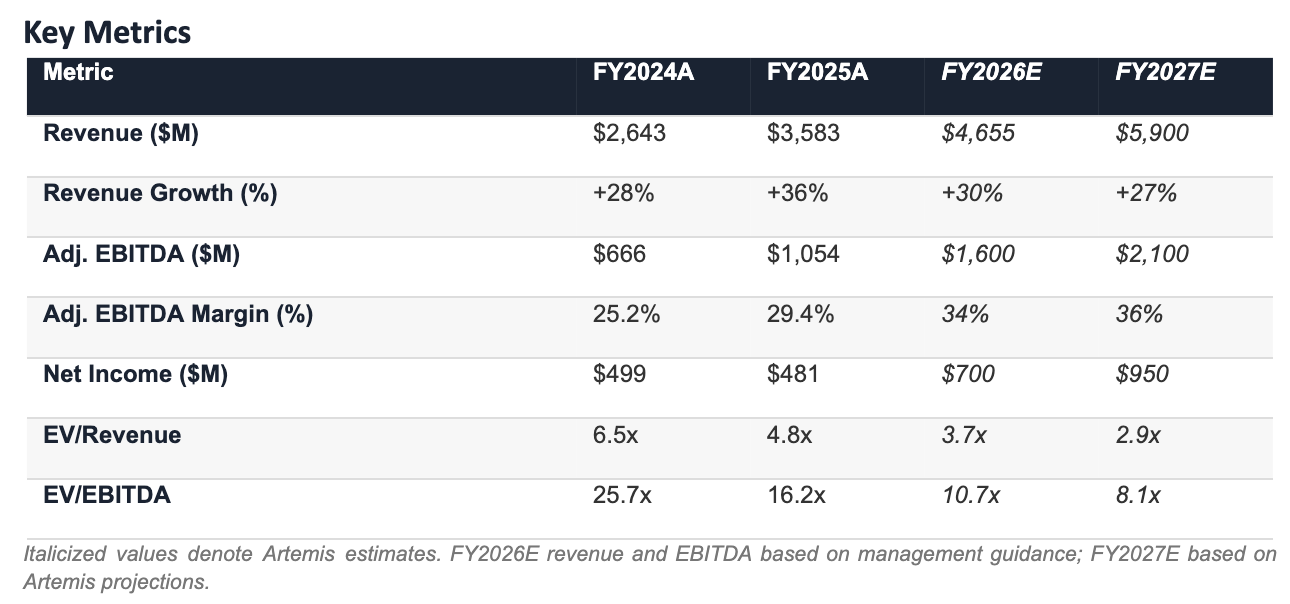

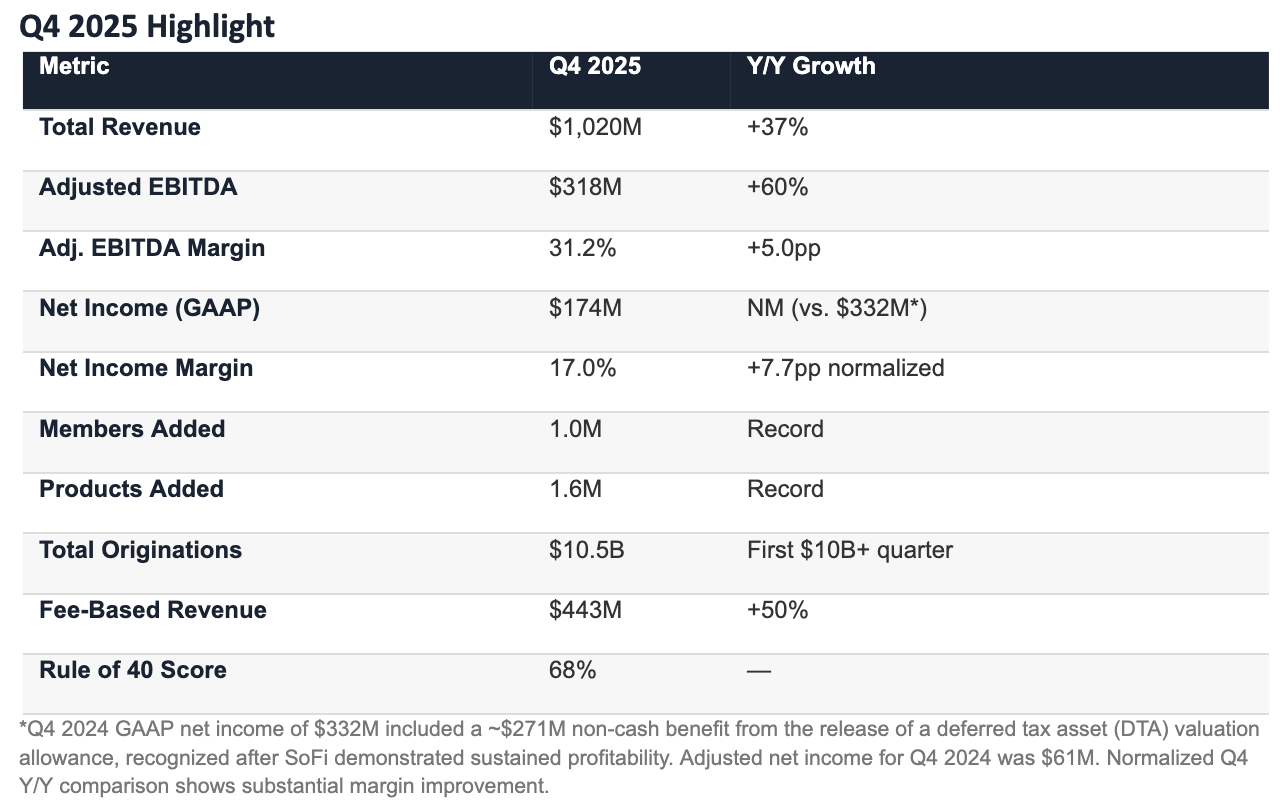

Revenue growth reaccelerated in FY2025 to 36% from 28% in FY2024, driven by the rapid scaling of Financial Services (which grew 88% year-over-year in Q4) and the loan platform business. The company crossed $1 billion in quarterly revenue for the first time in Q4 2025. Revenue has compounded at a nearly 50% CAGR since 2018, yet the company remains in the early stages of penetrating its addressable markets. Management has guided for 30%+ revenue growth in FY2026, with a long-term aspiration for sustained growth at similar rates, supported by expanding crypto services, business banking, and international expansion.

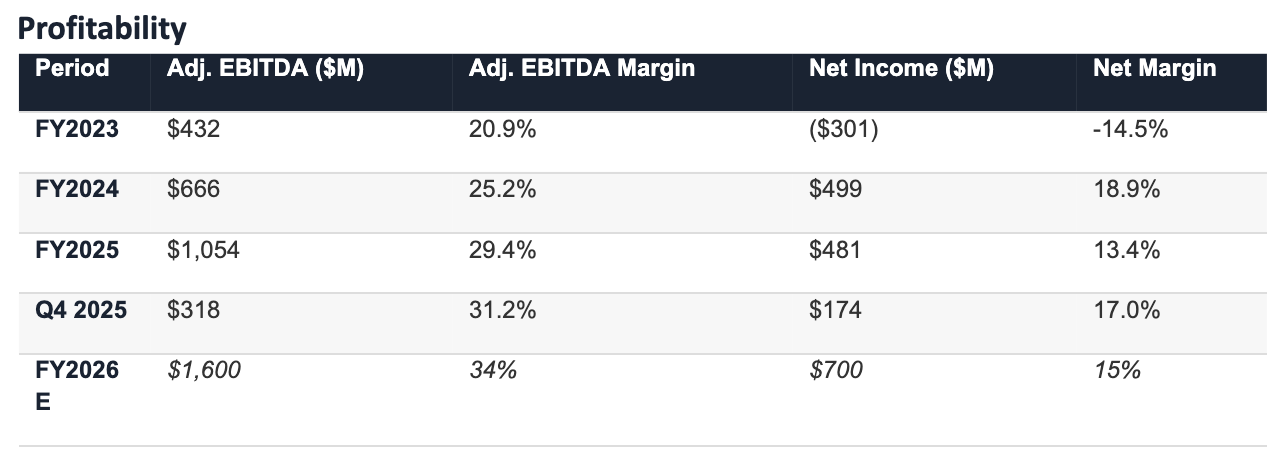

Adjusted EBITDA grew 58% year-over-year in FY2025 to $1.05 billion, with margins expanding from 25% to 29%. Q4 margins hit 31%, surpassing the company’s original long-term target of 30% set at IPO. The incremental EBITDA margin of ~41% demonstrates strong operating leverage. FY2025 GAAP net income of $481 million appears to decline from FY2024’s $499 million, but this is misleading: Q4 2024 included a ~$271 million non-cash DTA valuation allowance release that inflated FY2024 results. Stripping that out, underlying profitability improved significantly, as evidenced by net income margins expanding sequentially from 9.3% in Q1 to 17.0% in Q4 2025.

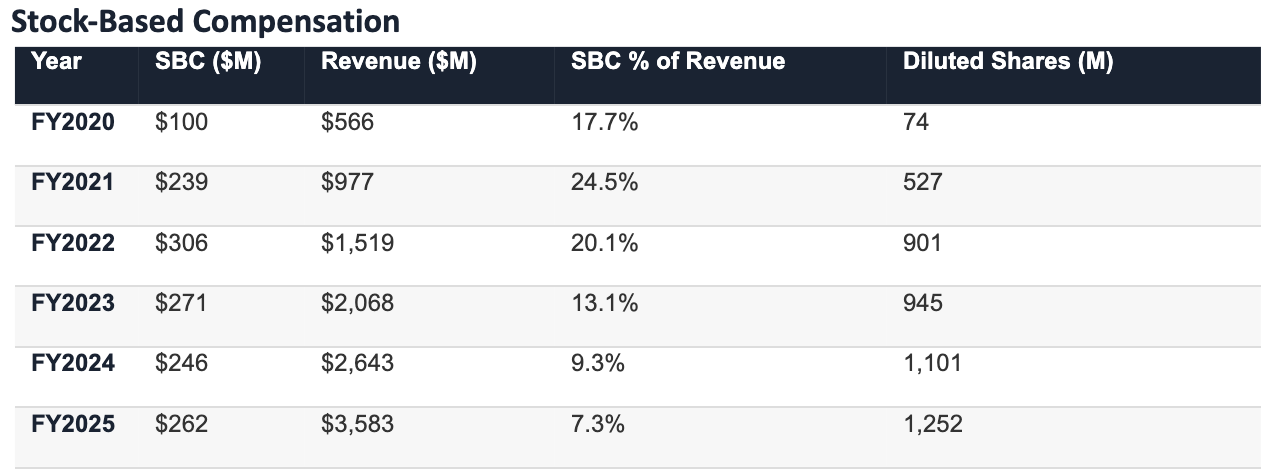

Stock-based compensation peaked at $306 million in FY2022 and has since moderated to approximately $250–$270 million annually, even as headcount and scope have expanded. More importantly, SBC as a percentage of revenue has declined sharply—from 24.5% in FY2021 (the SPAC year) to 7.3% in FY2025—as revenue growth has far outpaced compensation expense. The cumulative dilution remains significant: diluted shares outstanding have grown from 527 million post-SPAC to 1.25 billion, a 137% increase. However, the rate of dilution is slowing, and if absolute SBC remains flat while revenue scales toward $5 billion+, the SBC-to-revenue ratio should converge toward the 3–5% range typical of mature fintechs.

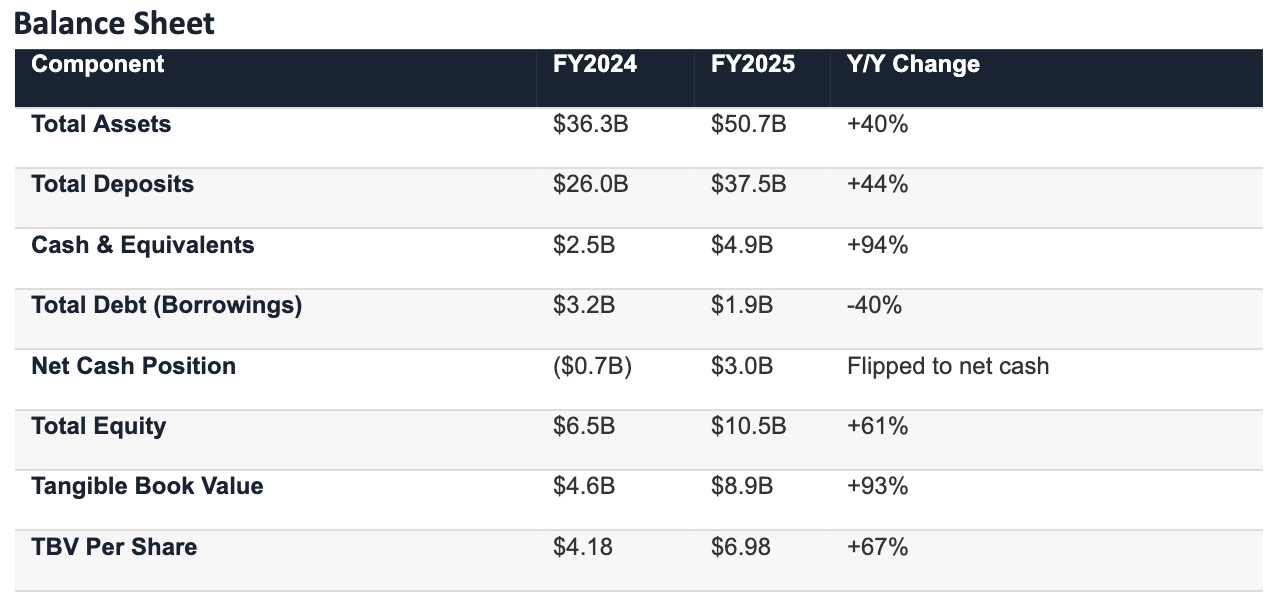

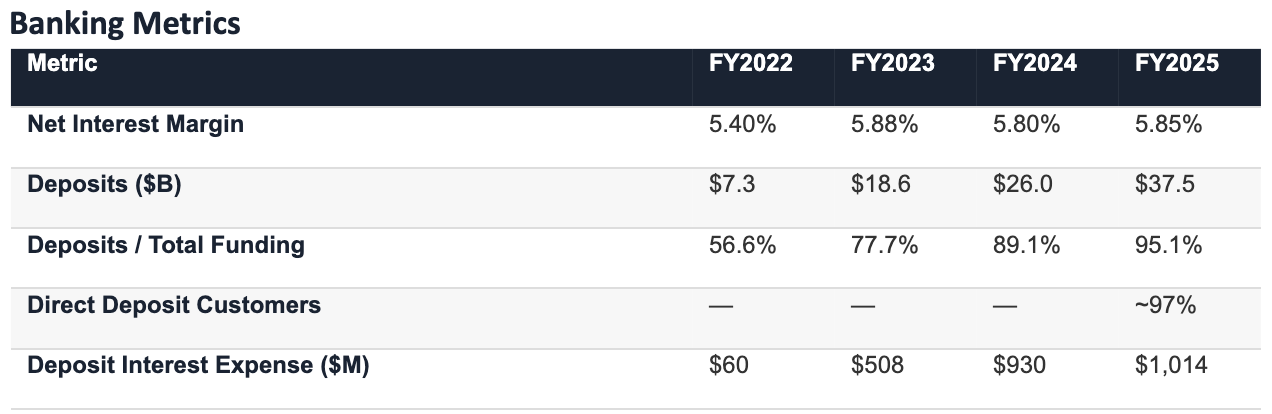

SoFi’s balance sheet strengthened dramatically in FY2025. The company raised $3.2 billion in new capital, growing tangible book value by $4.3 billion to $8.9 billion ($6.98 per share). Total debt was cut by 40% from $3.2 billion to $1.9 billion, flipping the company from a net debt to a $3.0 billion net cash position. Deposits grew 44% to $37.5 billion, now representing 95.1% of total funding—up from 89.1% in FY2024—replacing higher-cost warehouse borrowings. CEO Noto described this as a “fortress balance sheet” that provides “a broad range of optionality.”

SoFi maintains an exceptionally high net interest margin of 5.85%—well above traditional bank peers—reflecting its focus on higher-yielding personal and student loans funded by lower-cost deposits. The deposit franchise has scaled at a remarkable pace, growing from $7.3 billion (first full year post-charter) to $37.5 billion in three years. Critically, 97% of deposits come from direct deposit customers, indicating high-quality primary banking relationships that are naturally sticky. As CEO Noto noted, SoFi’s structural advantage in deposit pricing comes from its profitable lending business, which allows it to offer top-quartile APYs while still generating strong spreads.

4. Growth Drivers & Member Metrics

Unlike traditional banks that grow primarily through rate competition and branch expansion, SoFi’s growth engine is built on a digital flywheel: brand awareness drives member acquisition, product quality drives cross-buy, and cross-buy drives lifetime value and operating leverage. This section examines the key growth vectors and their trajectory.

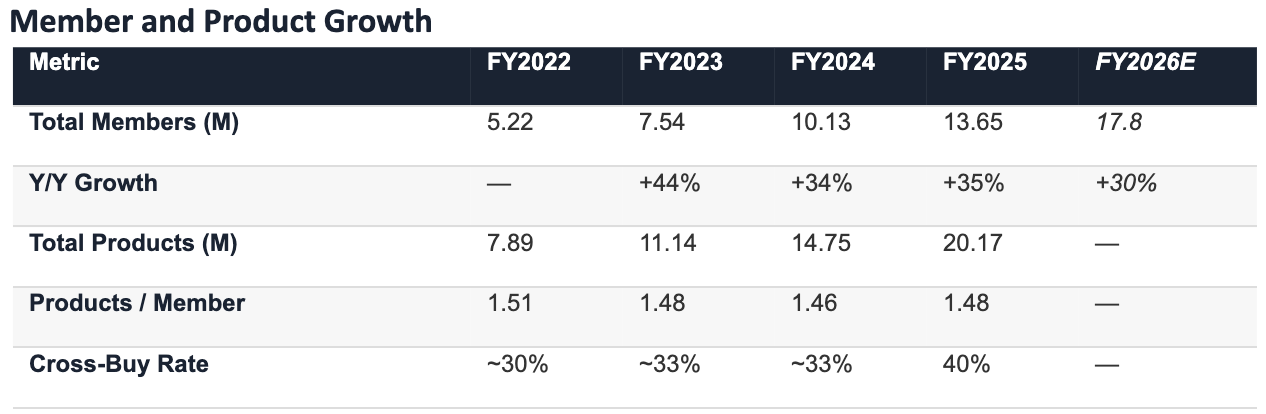

SoFi added a record 1 million members in Q4 2025 alone—the first time the company achieved seven-figure quarterly member growth—bringing total membership to 13.7 million, up 35% year-over-year. Product adoption is accelerating even faster: 1.6 million new products were added in Q4, and the cross-buy rate reached 40%, up 7 percentage points year-over-year. Management attributes this to the “one-stop shop” strategy: a single integrated app where members can borrow, save, spend, and invest. The 2026 guidance targets at least 30% member growth, implying ~17.8 million members by year-end.

Fee-Based Revenue Diversification

One of the most significant structural shifts in SoFi’s business is the rapid growth of fee-based, capital-light revenue. Fee-based revenue hit a record $443 million in Q4, representing $1.8 billion on an annualized basis, up 50% from the prior year. This includes interchange, brokerage fees, referral fees, and loan platform business commissions. The loan platform business—where SoFi originates loans on behalf of third-party partners—generated $3.7 billion in originations in Q4 alone, earning fees without deploying balance sheet capital.

New Growth Vectors

Crypto & Stablecoin: SoFi Crypto (first nationally chartered bank to offer consumer crypto trading), SoFi USD stablecoin (backed 1:1 by cash at Fed master account), and plans for institutional crypto trading, custody, and stablecoin-as-a-service for B2B clients.

Business Banking: Launching in 2026. SoFi aims to be the bank for businesses transacting in both fiat and cryptocurrencies, filling a critical market gap. Will include institutional trading, digital asset custody, and 24/7 settlement via SoFi Exchange.

International Expansion: SoFi Pay now covers 30+ countries. Medium-term plan to offer full SoFi Pay to non-U.S. users, serving as a global brand-building channel. Technology Platform (Galileo/Technisys) already expanding to Latin America and Middle East clients.

AI & Product Innovation: SoFi launched its own Agentic AI ETF and is leveraging AI across product quality and marketing efficiency. Goal is to drive “escape velocity” in customer acquisition cost efficiency.

5. Valuation

Methodology

Primary Methods: Comparable Company Analysis using EV/EBITDA and P/TBV (important for bank stocks) as primary multiples, supplemented by a scenario-based valuation framework. For a bank holding company, Price-to-Tangible Book Value provides a fundamental floor, while EV/EBITDA captures the growth and operating leverage of the non-lending segments.

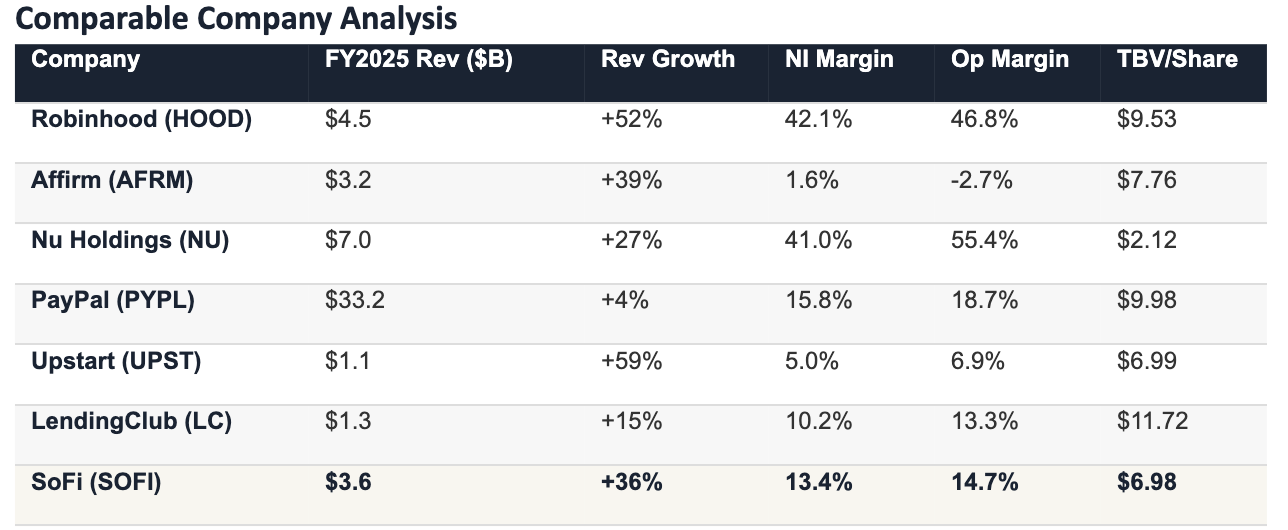

SoFi’s growth profile (+36% revenue growth) is second only to Upstart (+59%) and comparable to Affirm (+39%) within its peer set, but with significantly better profitability than either. The company’s net interest margin of 5.85% and 95% deposit-funded model distinguish it from non-bank fintechs. At a P/TBV of ~2.3x, SoFi trades at a meaningful discount to most fintech peers despite superior growth and an improving margin trajectory. The -42% YTD decline has compressed multiples to levels that appear disconnected from fundamentals: EV/FY2026E EBITDA of ~10.7x for a company guiding 30%+ growth is well below the typical growth fintech range of 15–25x.

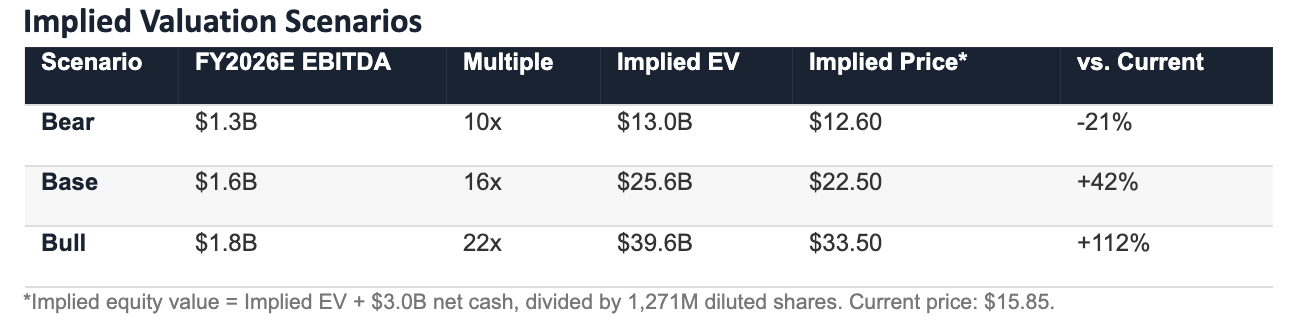

The base case of $22.50 per share (+42% upside) assumes SoFi meets its FY2026 guidance of ~$1.6 billion adjusted EBITDA and the market rewards execution with a 16x forward multiple—below the peer median but reflecting fintech-bank hybrid discount. The bull case at 22x assumes margin upside from accelerating fee-based revenue and successful crypto/business banking launches. The bear case reflects a recession scenario where lending volumes decline and the stock de-rates to deep value bank multiples.

6. Bull / Bear Thesis

Bull Case

Financial Services Flywheel Reaching Escape Velocity: Financial Services and Technology Platform grew 61% year-over-year in Q4 and now represent 57% of revenue. Fee-based revenue hit a $1.8 billion annualized run rate. As these capital-light segments continue to scale, margins should expand toward 35%+ adjusted EBITDA and the market should re-rate SOFI closer to software/platform multiples rather than bank multiples.

Crypto First-Mover Advantage as a National Bank: SoFi is the first nationally chartered bank to offer crypto trading, issue a stablecoin, and deploy blockchain-powered payments. The combination of FDIC insurance + crypto infrastructure positions SoFi as the trusted bridge between traditional finance and digital assets. SoFi USD and business banking could unlock an entirely new B2B revenue stream as infrastructure provider for banks and fintechs.

Deposit Machine Creates Structural Funding Advantage: Deposits grew 44% to $37.5 billion and now fund 95% of liabilities. With 97% direct deposit penetration and a 4.50% APY that most competitors cannot match profitably, SoFi’s cost of funding should decline as rates fall while maintaining deposit growth. CEO Noto noted this advantage will “make itself more clear” as rates decline, as SoFi can maintain top-quartile APY funded by lending spreads.

Massive Insider Buying Signals Management Confidence: CEO Noto purchased $1 million in SOFI stock in March 2026 amid the selloff. Combined with 2026 guidance for 30%+ growth through 2028 and the company’s track record of meeting or beating guidance, insider buying at these levels signals conviction that the selloff is unwarranted.

Valuation Disconnected From Fundamentals: At $15.85, SOFI trades at 10.7x FY2026E adjusted EBITDA and 2.3x tangible book value for a company growing revenue 30%+, generating a Rule of 40 score of 68%, and with nine consecutive quarters of GAAP profitability. The average analyst price target of $25.70 implies 62% upside. Historical dislocation of this magnitude in high-quality growth fintechs has typically resolved favorably for investors.

Bear Case

Consumer Credit Deterioration in a Macro Downturn: SoFi’s $15+ billion personal loan portfolio is sensitive to employment and consumer spending. Tariff-driven inflation and a potential recession could increase default rates and force higher provisioning, compressing margins. The company’s limited track record through a full credit cycle creates uncertainty about loss severity.

Persistent Share Dilution From Stock-Based Compensation: Diluted shares outstanding have grown from 527 million post-SPAC to 1,252 million in FY2025—a 137% increase. While absolute SBC has moderated from its $306M peak to ~$262M and fallen from 24.5% to 7.3% of revenue, the cumulative dilution is substantial. Continued SBC to attract talent represents ongoing per-share value erosion that must be offset by earnings growth.

Lending Revenue Concentration and Rate Sensitivity: Despite diversification efforts, lending still represents 52% of revenue and is sensitive to interest rate movements. Rising rates increase funding costs and can dampen loan demand; falling rates too quickly compress net interest margins. The bank’s 5.85% NIM, while strong, could face pressure in a rapidly shifting rate environment.

Crypto Execution Risk: SoFi’s ambitious crypto strategy (stablecoin, business banking, institutional trading) introduces operational complexity and regulatory risk. The regulatory framework for bank-issued stablecoins is still evolving, and the Clarity Act has not yet been enacted. Crypto revenue is inherently cyclical and sentiment-driven.

Intense Competition Across All Segments: SoFi competes with well-capitalized incumbents in every segment: JPMorgan, Goldman Marcus in banking; Robinhood, Schwab in brokerage; LendingClub, Upstart in lending; Stripe, Marqeta in infrastructure. The “one-stop shop” model requires SoFi to be competitive in each category simultaneously.

Base Case

SoFi delivers on its FY2026 guidance of ~$4.65 billion in adjusted net revenue and ~$1.6 billion in adjusted EBITDA, supported by continued 30%+ member growth and expanding fee-based revenue. Crypto and business banking products launch but do not contribute materially until late 2026 or 2027. Credit quality remains manageable but provisions increase modestly due to macro uncertainty. The stock re-rates from current levels toward the $20–25 range as the market recognizes that the YTD selloff overreacted to macro fears. At 16x FY2026E EV/EBITDA, the base case price target is approximately $22.50—representing 42% upside from current levels.

7. Risk Factors

Company-Specific Risks

Credit Quality: SoFi’s unsecured personal loan portfolio is the largest revenue driver and is sensitive to employment levels and consumer spending. A spike in unemployment could lead to higher-than-expected defaults.

Stock-Based Compensation & Dilution: Diluted shares have grown 137% since FY2021 post-SPAC. SBC as a percentage of revenue has improved significantly (24.5% → 7.3%), but the cumulative dilution is already embedded in the share count. Continued SBC must be offset by earnings growth to create per-share value.

Execution Across Multiple New Verticals: SoFi is simultaneously expanding into crypto, stablecoins, business banking, international payments, and new lending products. Managing multiple growth vectors increases operational complexity.

FY2025 Net Income Anomaly: GAAP net income declined from $499M (FY2024) to $481M (FY2025) despite revenue growth, primarily because Q4 2024 included a ~$271M non-cash gain from releasing a deferred tax asset valuation allowance (adjusted Q4 2024 net income was only $61M). While the underlying profitability trend is improving, this creates an optically unfavorable Y/Y comparison.

Industry & Macro Risks

Tariff-Driven Recession Risk: Escalating tariffs and trade uncertainty could trigger a consumer recession, reducing loan demand, increasing credit losses, and compressing valuations for the entire fintech sector.

Interest Rate Sensitivity: SoFi’s bank model is sensitive to rate movements. Rapidly falling rates could compress NIM; rising rates could dampen loan demand and increase funding costs.

Regulatory Burden: As a bank holding company, SoFi faces heightened regulatory oversight (OCC, Fed, FDIC). Consumer lending regulations could increase compliance costs or restrict product offerings.

Concentration Risks

Revenue: 52% from lending products; Financial Services (43%) growing rapidly and approaching parity

Geographic: 100% United States (international expansion via SoFi Pay and Galileo is nascent)

Product: Personal loans represent the single largest revenue contributor; student loans subject to federal policy changes (OBBB legislation)

Platform: Technology Platform client concentration; loss of a major Galileo client could impact segment revenue

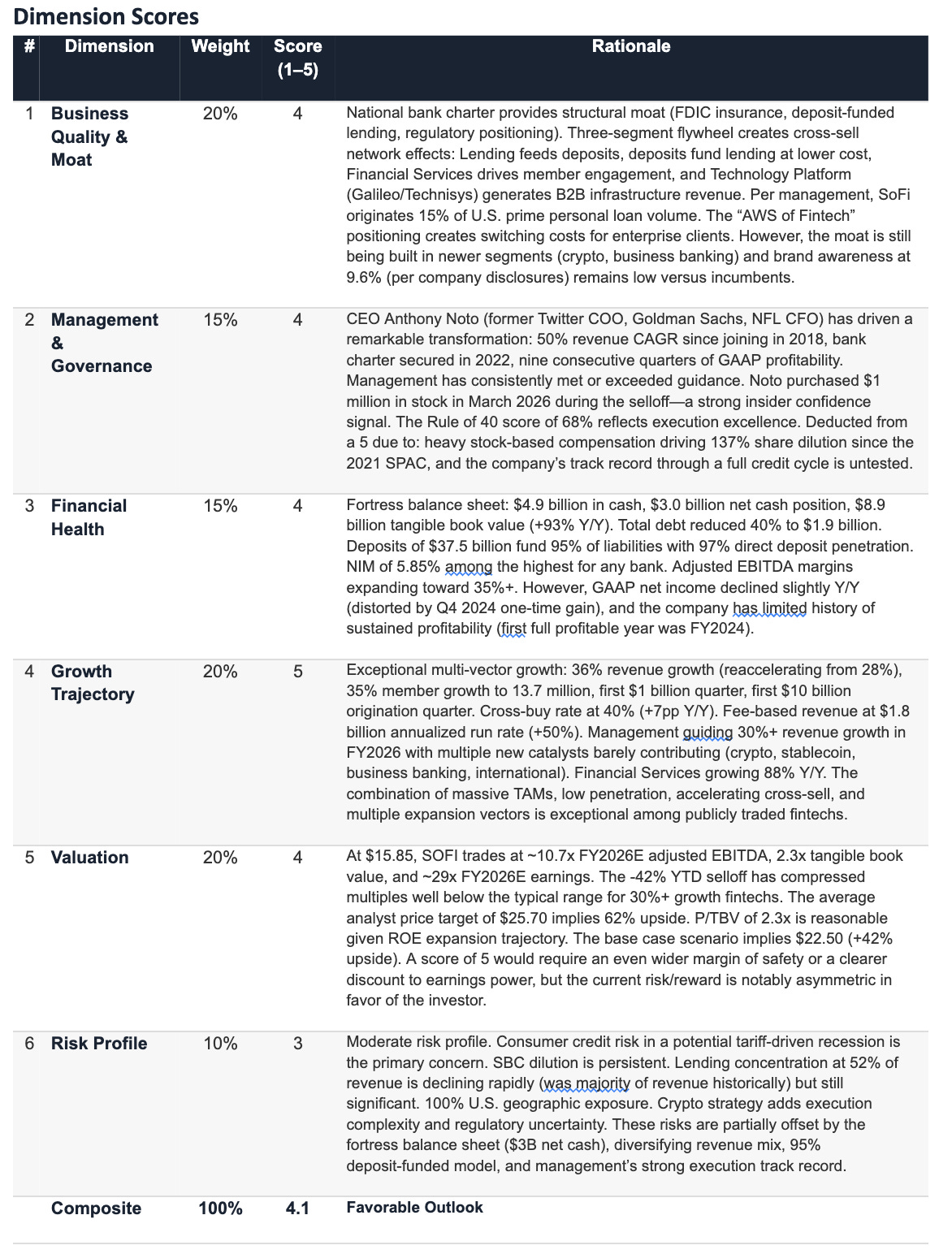

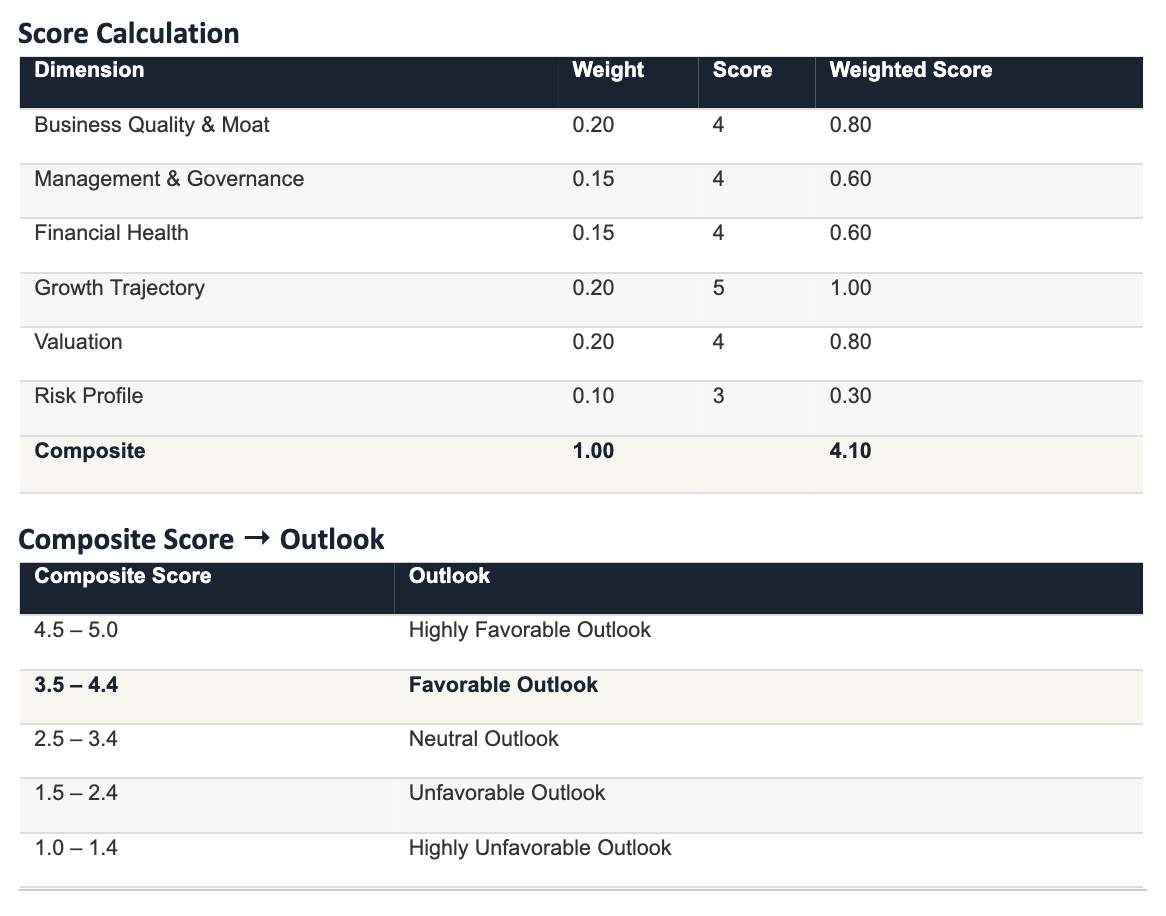

8. Scoring Framework

Disclaimer: This report is produced by Artemis for informational and educational purposes only. It does not constitute investment advice, a recommendation, or a solicitation to purchase, sell, or hold any security. The analysis, scores, and outlook labels contained herein reflect the research team’s assessment based on publicly available information at the time of publication and are subject to change without notice. Readers should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions. Artemis, its affiliates, and its analysts may hold positions in the securities discussed in this report. Past performance is not indicative of future results. The information in this report is believed to be accurate but is provided “as is” without warranty of any kind. Artemis disclaims all liability for any errors, omissions, or losses arising from reliance on this report.

© 2026 Artemis. All rights reserved.