Hyperliquid Strategies ($PURR)

The Only DAT With a Productive Underlying Asset

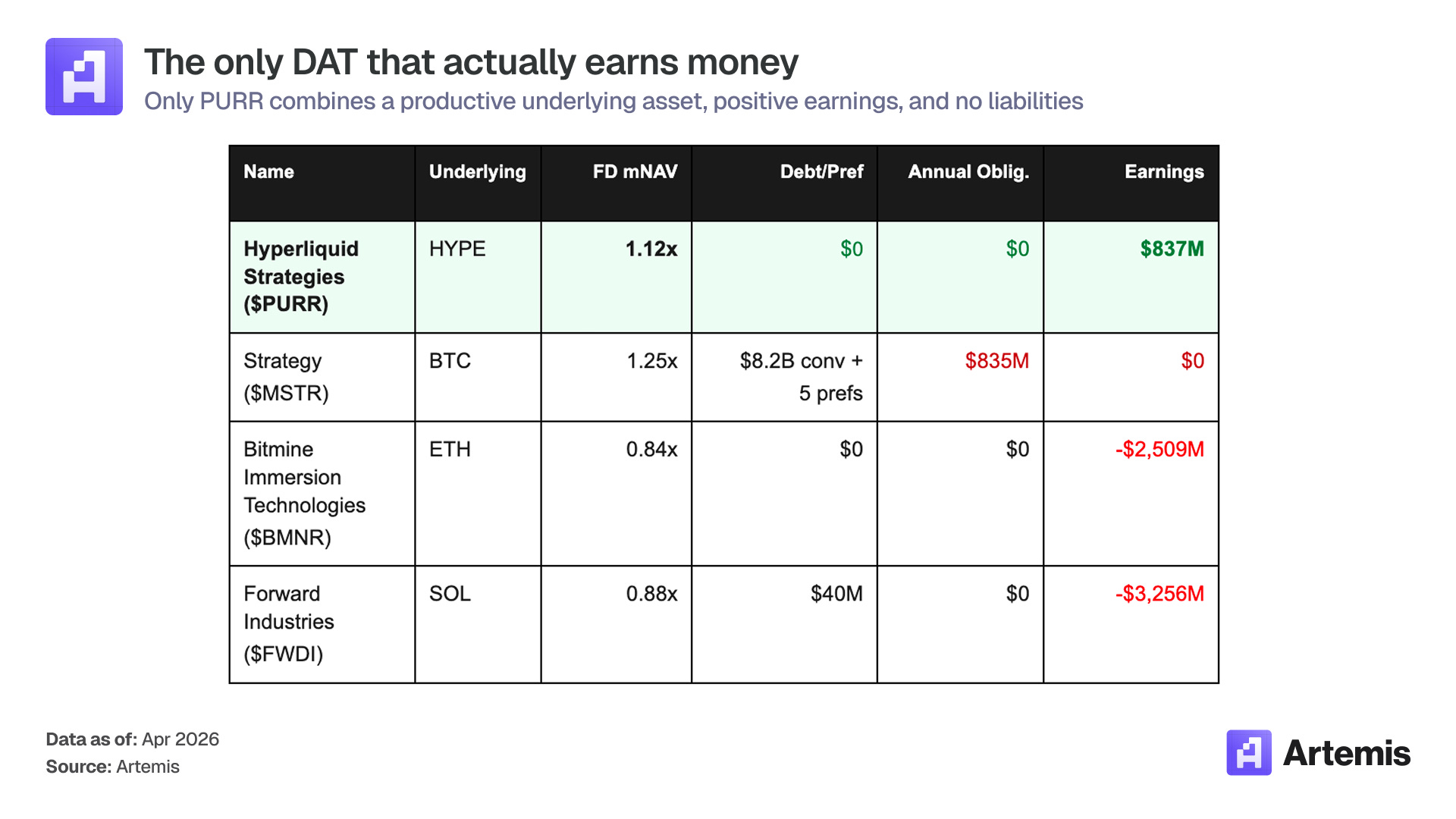

Conclusion:

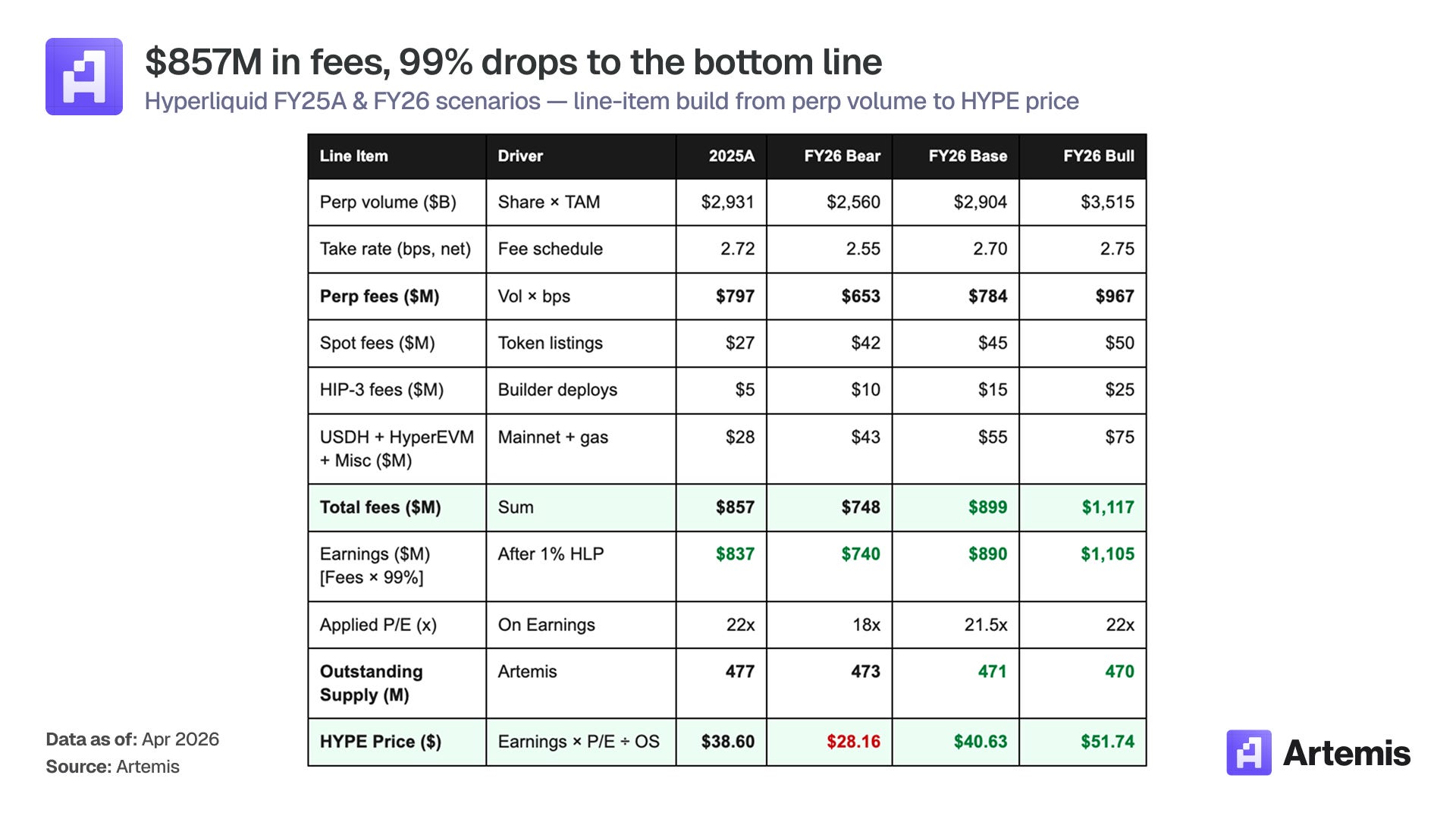

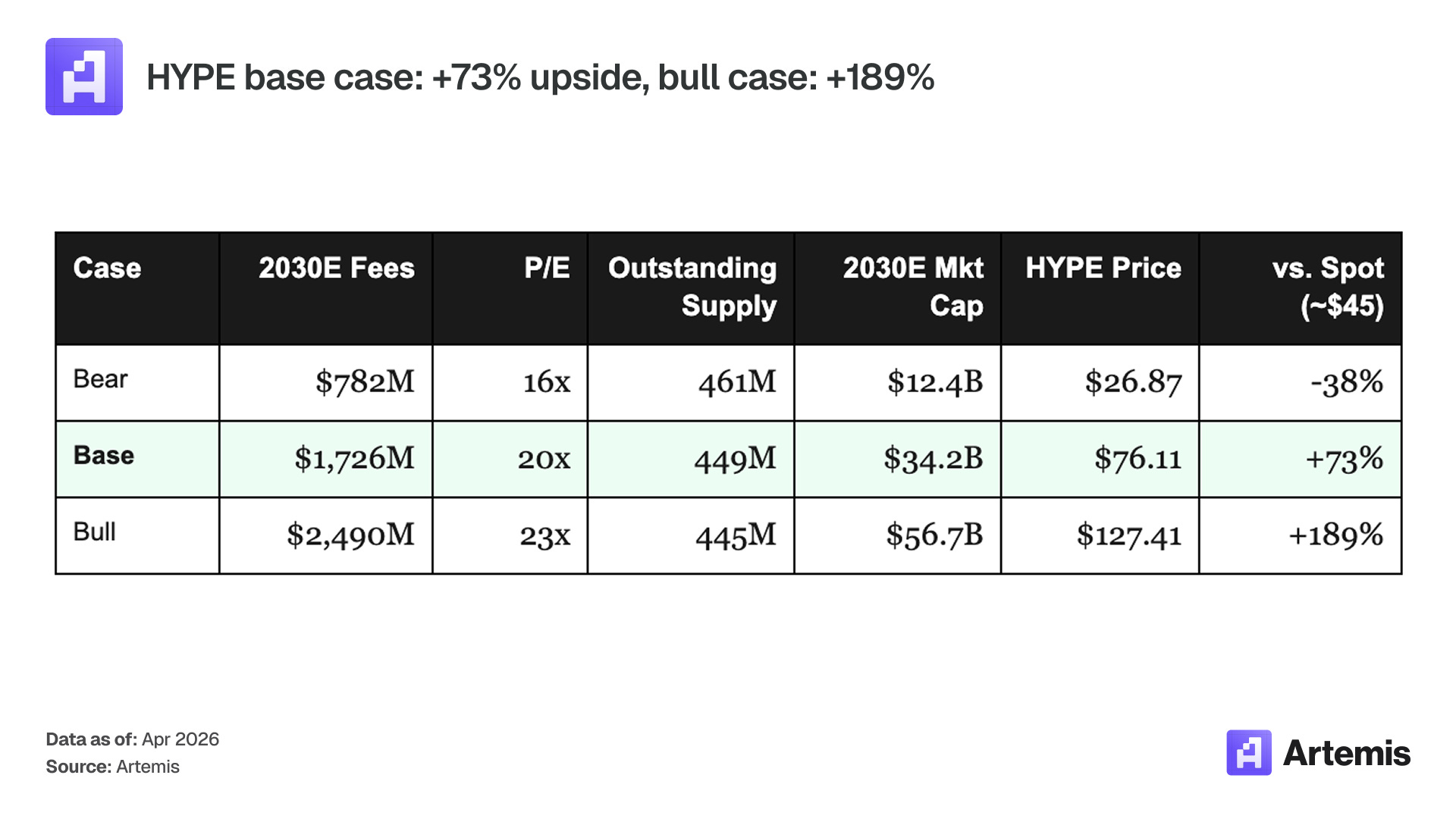

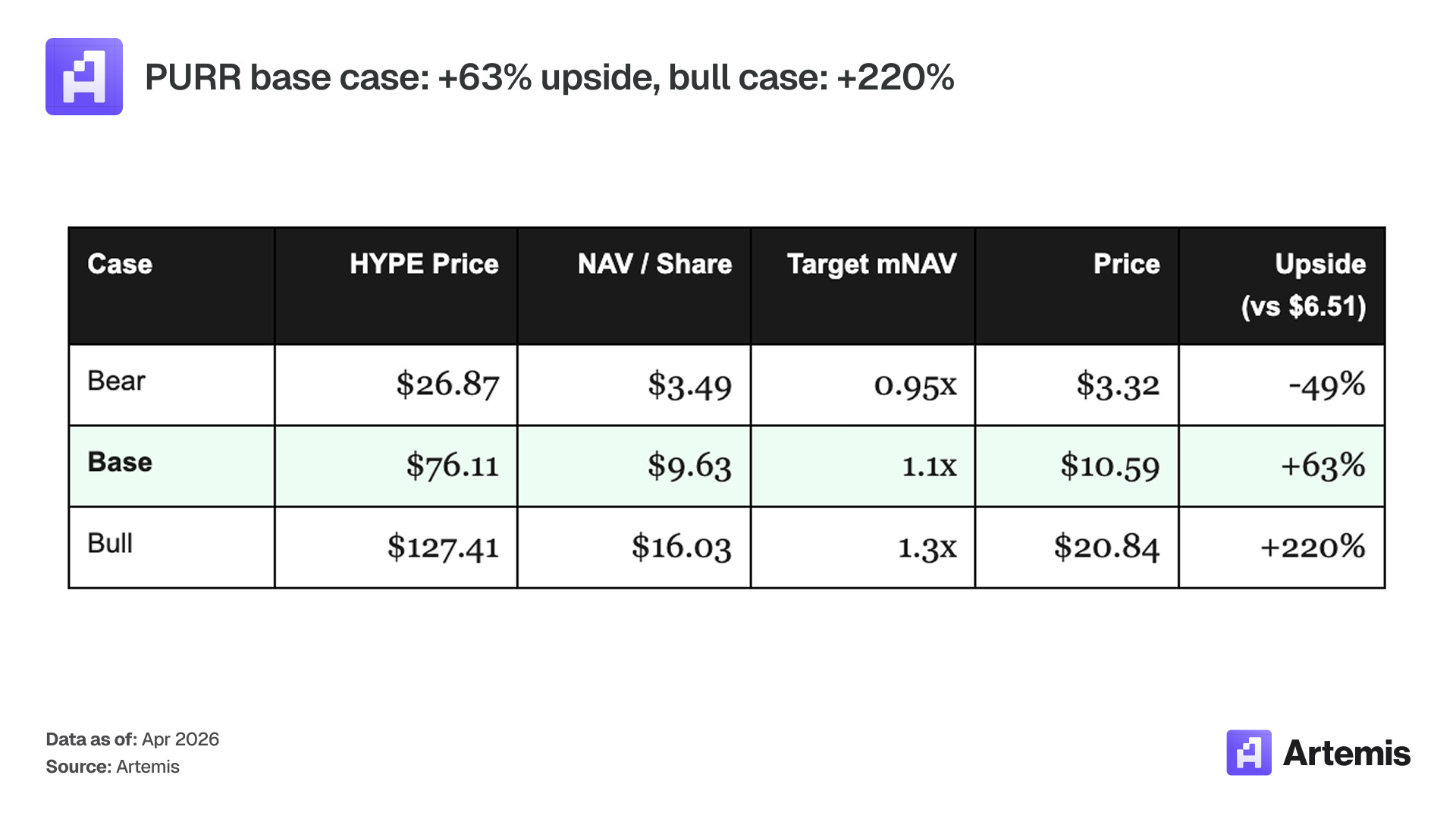

The market is pricing PURR as another digital asset treasury copycat — an MSTR-style vehicle where a premium lets management issue equity, buy more tokens, and accumulate more per share. We think that framing misprices the business. Strategy spends $2.3 million a day to service $835 million of annual preferred and convertible obligations on top of 780,897 bitcoin that earn nothing, and its mNAV has collapsed from peaks above 6x to 1.15x today. PURR carries zero debt, zero preferreds, and zero recurring obligations, and owns 18.8 million HYPE tokens in the only major protocol that produced positive earnings in 2025: $857M of fees ($797M from perps at a 2.72 bps take rate), 99% of which flows to the Assistance Fund — $837M of Earnings bought back and burned at near-zero operating cost. The token is structurally deflationary: ~19M HYPE bought back annually against ~7M emitted from staking reserves. The stock trades at 1.12x mNAV. Our base case carries HYPE to $76 on $1.71B of 2030E Earnings at 20x P/E, holds PURR at 1.1x mNAV, and implies a $10.59 share of ~63% upside over five years. Bull case at $127 HYPE and 1.3x mNAV implies ~$20.84, +220%. Bear case compresses HYPE to $27 at 16x P/E and 0.95x mNAV at −49%.

Comps:

PURR is the only DAT that combines a productive underlying, positive earnings, and zero liabilities.

What Does $PURR Do?

Hyperliquid Strategies Inc (NASDAQ: PURR) is a digital asset treasury company whose sole mandate is to accumulate and hold HYPE, the native token of the Hyperliquid protocol. The company was formed in December 2025 via an $888M business combination involving Sonnet BioTherapeutics, Rorschach I LLC (a Paradigm-affiliated SPAC), and a new entity spun up by Atlas Merchant Capital.

The balance sheet is the cleanest in the DAT category: 18.8M HYPE, $112.6M of cash, zero debt, zero preferreds, zero convertibles. A $30M stock buyback program was authorized in January 2026. As of February 3, 2026, $10.5M was deployed, retiring ~3.0M shares and pulling the fully diluted count to 150.8M. A $1 billion equity line sits on top of the cash position as optional dry powder for HYPE drawdowns.

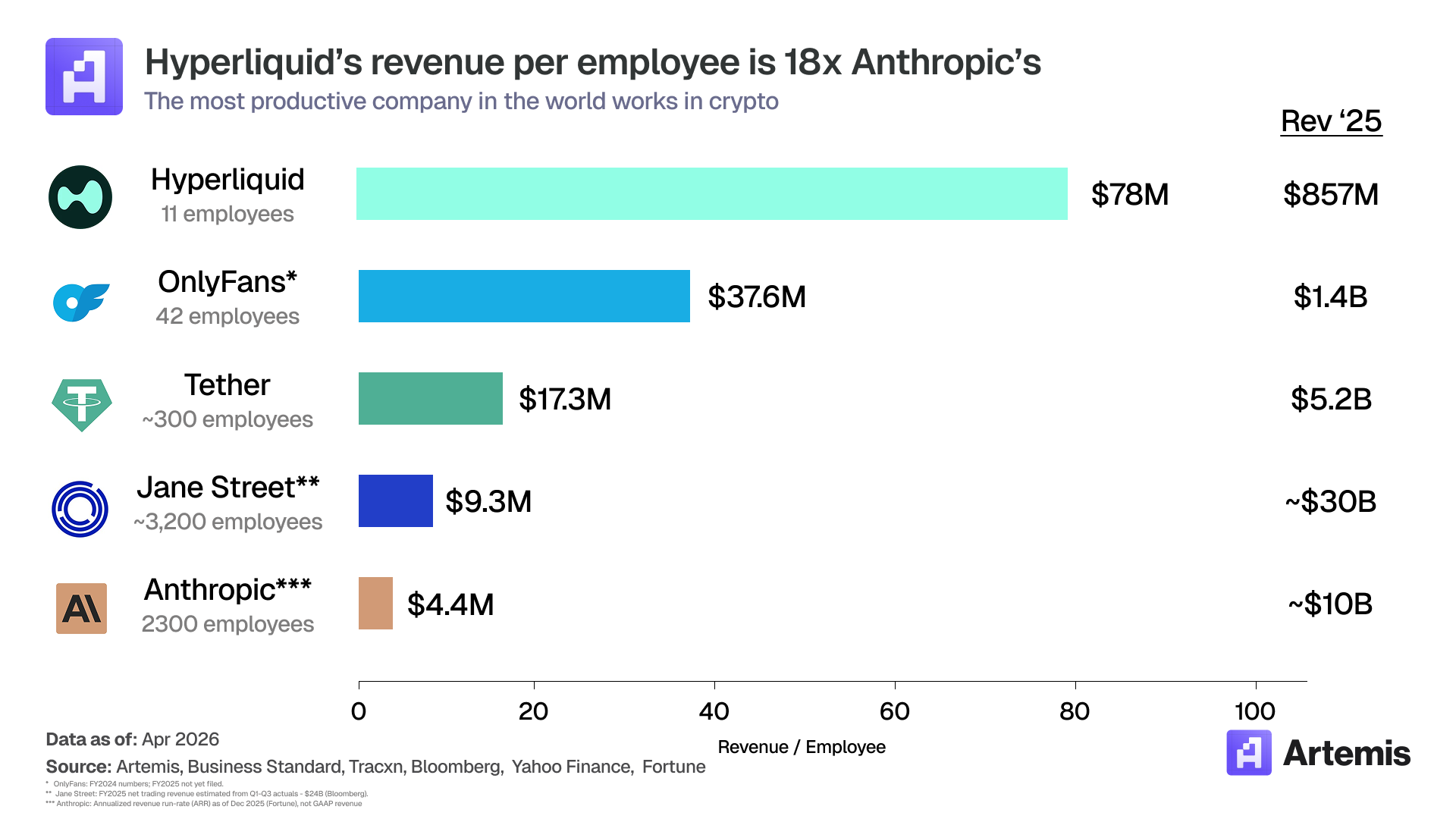

The underlying is the asset that makes this structure unusual. HYPE is an equity-like claim on Hyperliquid, a perps exchange that generated $857M in 2025A fees with 11 employees (~$78M rev/employee, the highest of any company in the world).

The Fee Machine

Hyperliquid is an exchange.

The model is a volume × take-rate business with near-zero marginal cost.

The fee waterfall breaks down into six line items:

Thesis #1: The Only Underlying Asset That Earns

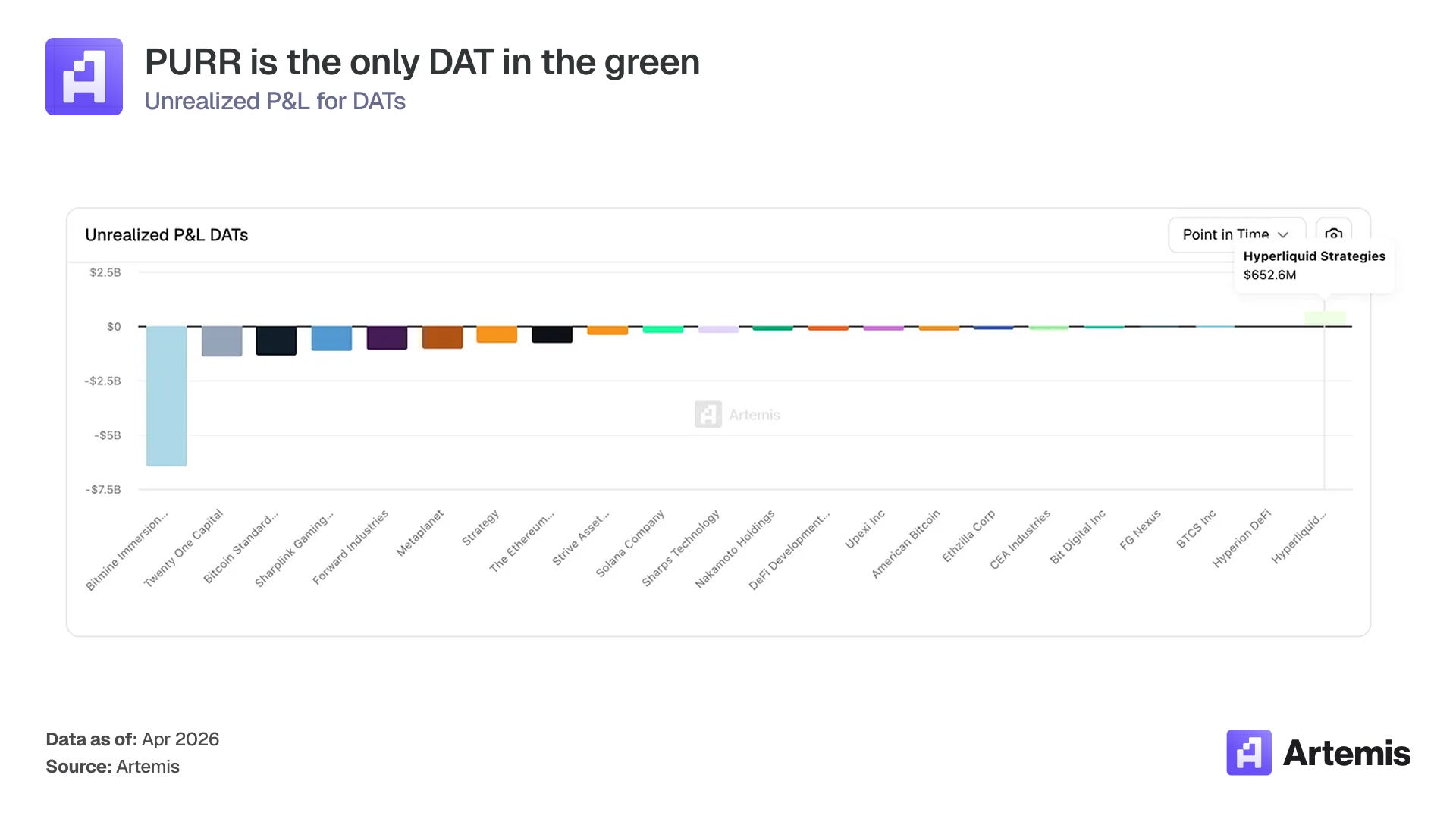

Every DAT on a U.S. exchange today wraps an asset that either earns nothing (BTC) or runs at a loss once you account for the tokens minted to keep the chain alive. Ethereum generated $526M of fees but paid $3,035M in staking emissions; Solana generated $680M but paid $3,936M. Hyperliquid generated $857M in fees. Earnings definitions matter here. For Hyperliquid, earnings = fees after the 1% HLP vault cut (3% pre-Aug 30, 2025), with 99% flowing to the Assistance Fund for buyback-and-burn: $837M on $857M of fees. For Ethereum and Solana, the comparable figure is fees minus staking issuance, since their chains cannot function without token emissions to pay validators. This is a true operational cost, and both are negative at time of writing. Hyperliquid’s $312M of staking emissions are drawn from a pre-allocated reserve, not from exchange revenue, so they sit below the line. On the adjusted basis ($545M), Hyperliquid is the only protocol with positive underlying cash flow assets. The performance gap shows up on DAT balance sheets. BMNR’s average ETH entry was $2,826; Forward Industries bought SOL at $232. Both are underwater.

PURR is the only DAT sitting on meaningful unrealized gains, up roughly $600M on its HYPE position. The underlying asset isn’t just productive, it’s appreciating.

Five growth drivers are compounding this advantage:

1. HIP-3: Hyperliquid becomes a listing platform. Live since October 2025, HIP-3 lets any builder stake 500,000 HYPE to deploy permissionless perps on any asset — commodities, equities (China, Korea, Japan), FX, exotics. This transforms HL from a crypto trading venue into a general listing layer. TradeXYZ’s crude-oil HIP-3 market processed $305M of weekend notional during the Strait of Hormuz crisis; cross-asset weekend prices tracked TradFi reopen at R² = 0.785 (Shaunda from Blockworks). The listing TAM expands from $3-5T of crypto derivatives to the >$100T global derivatives market. Each HIP-3 deployment requires a permanent 500k HYPE stake. HIP-4 carries the same requirement. Twenty markets at scale retire ~10M HYPE (2.1% of Outstanding Supply) from the float permanently.

2. DAT as a builder partnership. At current prices, 500k HYPE is roughly $23M. Most builder teams cannot self-fund that stake. A large holder like PURR (18.8M HYPE) is a natural counterparty: financing or partnering on HIP-3/HIP-4 deployments in exchange for a share of the market’s fees. This creates a revenue stream and ecosystem influence that individual HYPE holders cannot replicate at scale.

3. HIP-4: options and outcome contracts. Testnet launched March 2026; mainnet targeted Q4 2026. Deribit, which got acquired by Coinbase, traded over $1,875B in options notional value in 2025, making up over 85% of the market (~$2.2T). Options are just ~3% of crypto derivatives today (as Coinglass sizes the total crypto derivatives volume at $85.7T). If onchain options reach 15% penetration and HL captures half, that’s $165B of volume at ~8bps (options carry wider spreads than perps, deribit charges 12bps) = $135M/yr in fees. Our Base model assumes $50M in 2026E scaling to $130M by 2030E. Prediction-market outcome contracts open a second HIP-4 fee line (Annualized fees for Polymarket are reaching $700M).

4. Builder codes: negative CAC distribution. ~40% of HL DAUs already route through third-party frontends (Phantom is the largest). Builders earn a rev-share for every trade routed — $40M+ paid out to date (Dwellir). Compare Coinbase’s $400-600 retail CAC per funded account: HL’s is negative. This is why the model grows perp volume from $2.9T (2025A) to $5.2T (Base 2030E). The distribution layer is outsourced.

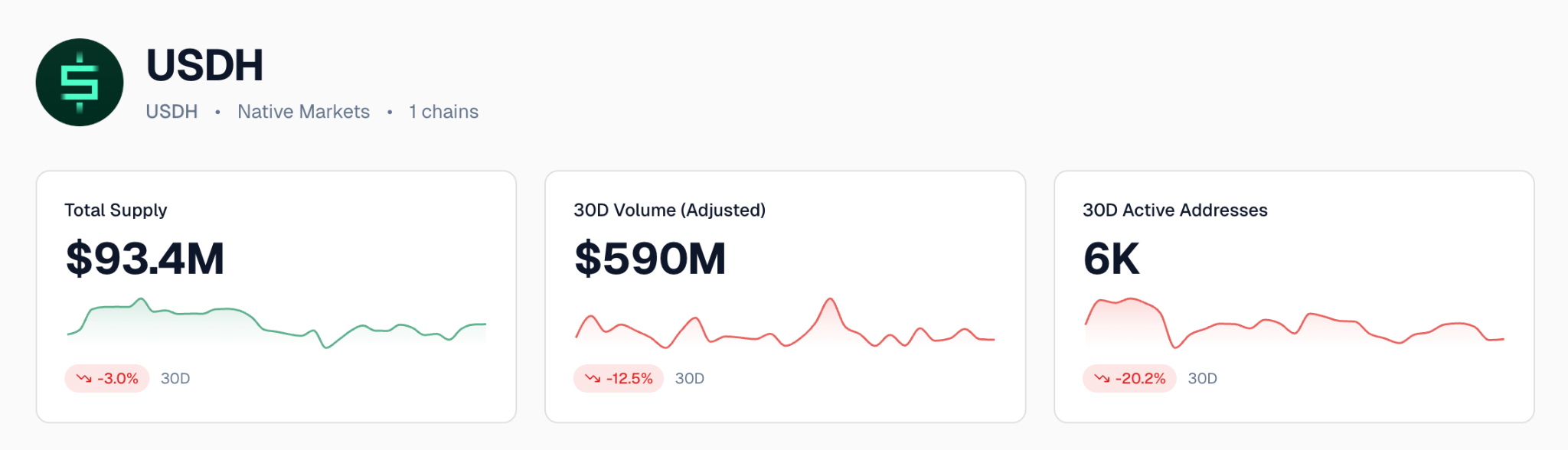

5. USDH: native stablecoin with revenue sharing. Native Markets won the USDH bid (Sept 2025). Reserves sit in a BlackRock-managed fund; 50% of reserve yield routes to the Assistance Fund.

At current supply (~$93M) and 3.7% T-bill yields, USDH contributes ~$1M/yr to the AF buyback. At $2-5B supply, that scales to $40-100M/yr. With the addition of HIP-4 which could only be traded on USDH, this could be a massive tailwind for the Native Markets stablecoin.

None of this expansion requires Hyperliquid to hire. Every growth vector (HIP-3 listings, HIP-4 options, builder distribution, and USDH float) is outsourced to external teams who take listing and distribution risk in exchange for a rev-share. The 11-person core team writes the protocol and the fee plumbing. This is a platform-scaling model: throughput, listings, and frontends grow without headcount.

Thesis #2: Buy the Wrapper at Cost

Strategy issued equity at a premium, converted the cash to BTC, and called it financial engineering. The mechanism inverts the moment the premium collapses, which is where the entire DAT category sits today (Strategy at 1.15x, down from 6x). PURR runs the opposite trade: the stock sits at ~1.12x NAV, and the $30M buyback program deploys only when the market prices PURR below the tokens it already owns. Every dollar deployed sub-NAV mechanically increases HYPE-per-share. The mechanism works both ways. Below NAV, management buys back stock and each remaining share represents more HYPE. Above NAV, they can issue shares at a premium and use the proceeds to buy more HYPE, also increasing HYPE-per-share. Either direction accretes value to existing holders.

No other DAT operates this way. Strategy, BMNR, and Forward Industries issue shares to buy tokens but have no buyback mechanism when the premium compresses. Their shareholders absorb the dilution on the way up and get nothing back on the way down.

Where direct HYPE wins: no corporate overhead, no dilution risk from the equity line, no regulatory risk specific to PURR management, and 100% of the token upside. Staking/airdrop optionality accrues only to direct holders.

But the wrapper offers four things direct HYPE doesn’t:

Automatic accretion without additional risk: the buyback described above is funded by cash already on the balance sheet. No margin calls, no liquidation risk, no action required from the holder. A direct holder can lever up through perps or borrowing, but that adds counterparty and liquidation exposure.

The regulatory moat: PURR and HYPD are the only two NASDAQ-listed vehicles for HYPE exposure, and any enforcement action on Hyperliquid’s no-KYC operations pushes institutional demand INTO the wrapper

Zero obligations: no debt service, no forced selling, no preferred shares.

Tax efficiency: PURR is taxed as a standard equity. Holders who hold for over a year pay long-term capital gains (20% federal max), can hold shares in IRAs and 401(k)s for tax-deferred or tax-free growth, and use tax-loss harvesting against other equity positions. Direct HYPE holders pay ordinary income tax (up to 37%) on every staking reward the moment it’s received, have no access to tax-advantaged retirement accounts, and face unresolved IRS guidance on airdrop cost basis. For a top-bracket U.S. investor, the wrapper roughly halves the tax drag.

The underlying exchange produces $1.76 of earnings per Outstanding HYPE ($837M ÷ 477M Outstanding Supply - we introduced this metric with Pantera Capital back in August 2025).

Valuation & Scenarios

Valuation is a two-step chain: first we value HYPE on fundamentals (2030E earnings × P/E ÷ Outstanding Supply), then we value PURR as NAV per share at that HYPE price multiplied by a target mNAV.

HYPE Scenarios

We value HYPE on earnings (fees × 99% after HLP) multiplied by a terminal P/E:

PURR Scenarios

Translating HYPE scenarios to PURR uses Adjusted NAV per share = (18.8M HYPE × price + $112.6M cash − $95.8M DTL + $4.5M adj) ÷ 150.8M FD shares, then applies a target FD mNAV. DAT stocks with productive underlyings have historically re-rated to 1.1x–2.0x NAV in up cycles; category norm at par is 1.0x.

Base case: HYPE at $76 by 2030, Adjusted NAV per share of $9.63, held at 1.1x NAV, implying a $10.59 stock and +63% upside over five years.

Bull case: HYPE reaches $127 by 2030, Adjusted NAV of $16.03, re-rate to 1.3x NAV, implying $20.84 and +220% upside.

Bear case: HYPE compresses to $27, Adjusted NAV drops to $3.49, mNAV slips to 0.95x, implying $3.32 and –49% downside. Base case returns ~10% annualized, but the distribution is asymmetric: bear downside is floored by zero liabilities and a protocol that still generates $782M of fees at trough, while bull upside compounds from both HYPE appreciation and mNAV re-rating.

Management & Cap Table

PURR is a balance sheet vehicle. The only job is capital allocation: when to buy HYPE, when to buy back shares, when to draw the equity line, and when to sit still. The team running that decision has 80+ combined years in capital markets, bank balance sheet management, and exchange infrastructure. Paradigm, the largest crypto-native fund in the world ($12.7B AUM), anchored the SPAC. D1, Galaxy, and Pantera round out a cap table that bridges TradFi and crypto. Diamond’s institutional network doubles as a distribution channel for allocators who want HYPE exposure but can’t custody tokens or navigate crypto tax complexity.

Bob Diamond (Chairman) — Former CEO of Barclays; co-founder of Atlas Merchant Capital.

David Schamis (CEO) — Co-founder of Atlas Merchant Capital; ex-JC Flowers partner.

Eric Rosengren (Board) — Former President, Federal Reserve Bank of Boston (2007-2021).

Larry Leibowitz (Board) — Former COO of the New York Stock Exchange; Operating Partner at Atlas Merchant Capital

Anchor investors include Paradigm, D1, Galaxy, and Pantera.

Risks

1. HYPE Price Drawdown

PURR is a levered claim on HYPE’s price. A broad crypto bear market compresses volumes, fees, and the buyback pool. Our bear case models this: TAM plateaus at $85T, HL share holds at 3%, take rate drifts to 2.3 bps, P/E de-rates to 16x, implying $27 HYPE and $3.32 PURR (−49%). Outstanding Supply is ~477M; Bear assumes a 35% team claim rate in 2026–27.

Mitigant: Zero liabilities mean no forced-seller dynamic. Even in the bear case, Hyperliquid still generates $782M of fees and $774M of earnings — the buyback-and-burn continues to exceed staking emissions, and the token remains deflationary (−23M HYPE/yr net). The $1B equity line is optional, not mandatory.

2. Regulatory Action on Hyperliquid

Hyperliquid operates without KYC. The Futures Industry Association has filed formal complaints with U.S. regulators requesting enforcement on U.S.-person access to offshore perps. An adverse action would compress HYPE directly. The HIP-3 expansion into TradFi assets (silver, oil, equities) increases regulatory surface area — commodity perps may draw CFTC attention beyond the crypto-specific enforcement actions seen to date.

Mitigant: PURR itself is a fully compliant NASDAQ-listed entity. A regulatory action would most likely push U.S. institutional demand into the PURR wrapper, which is the regulated way to own HYPE economics.

3. Equity Line Dilution

The $1B equity line can be drawn if HYPE dips, but drawing at the wrong price dilutes existing holders. At the bear-case $27 HYPE, PURR Adj NAV is $3.49/share — drawing at that level would issue shares below $6.51 spot.

Mitigant: The line is optional and at management’s discretion. Current posture is buyback, not issuance — $10.5M of the $30M authorized program was deployed by early Feb 2026, retiring ~3M shares and pulling FD count to 150.8M. The Paradigm-led cap table has no incentive to dilute itself.

4. DAT Premium Compression

Any premium that opens above NAV in a rally can compress quickly when sentiment turns. Strategy’s 6x mNAV premium collapsed to 1.15x FD in under 12 months. In the bull case, PURR re-rates to 1.3x NAV ($20.84); if sentiment reverses and the multiple compresses back to 1.1x, the loss is capped at the mNAV delta.

Mitigant: PURR trades at 1.12x mNAV today. The premium is 12 cents on the dollar versus Strategy’s peak of $5+ on the dollar. The asymmetry runs upward: 1.3x in a bull cycle is modest relative to the 2.0x+ that DAT stocks with productive underlyings have historically reached. At 1.0-1.1x, the wrapper’s value is the underlying asset.

Disclosure: This material is provided for informational purposes only and does not constitute investment advice, financial advice, trading advice, or any other form of advice. The views expressed are those of the authors and should not be relied upon as a recommendation to buy, sell, or hold any asset. The authors or affiliated entities may hold positions in the assets discussed. You should conduct your own research and consult appropriate financial professionals before making any investment decisions.