Figure Technology Solutions: Compelling After Its Worst Day Ever

A 26% crash erased $2B in value, after a record quarter. Inside the disconnect between Figure’s accelerating fundamentals and a market pricing fear, not earnings power.

The Selloff

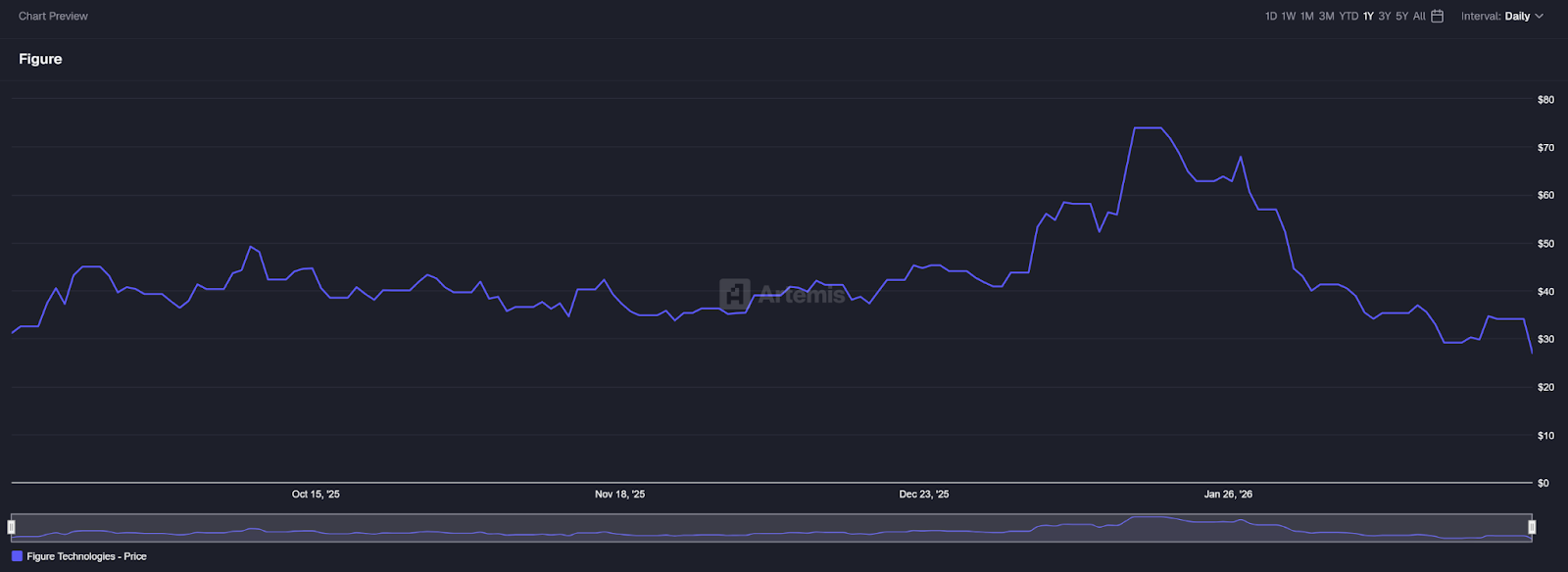

Figure just had the worst day in its short life as a public company.

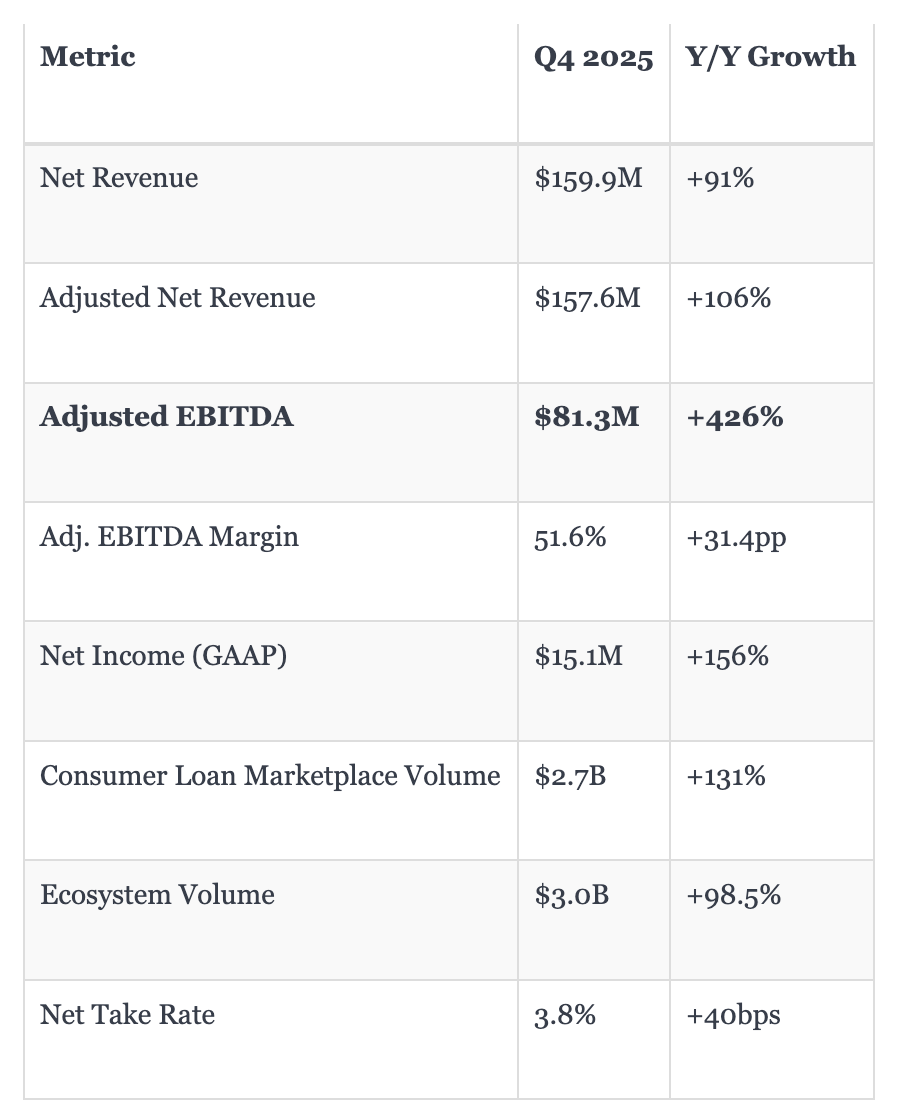

On February 27, 2026 — one day after reporting Q4 results that showed 91% revenue growth, 131% loan volume growth, and 426% adjusted EBITDA growth — shares of $FIGR cratered 26%, erasing roughly $2 billion in market capitalization in a single session. The stock closed at $25.28, just twenty-eight cents above its September 2025 IPO price of $25, and down 67% from its January highs near $78.

The proximate catalysts were twofold. First, Bank of America analyst Craig Siegenthaler cut his price target from $42 to $34 while maintaining an Underperform rating, citing concerns that large banks may not adopt Figure’s loan origination system due to its currently limited number of loan segments. Second, Figure reported GAAP EPS of $0.06 versus consensus expectations of $0.15 — a 60% miss that spooked investors who didn’t look beyond the headline number.

But here’s the thing: the EPS miss was almost entirely driven by elevated stock-based compensation, specifically one-time fully vested grants to third-party advisers and accelerated RSU recognition that the company explicitly flagged as non-recurring. CFO Minchung Kgil guided SBC to normalize around $21 million per quarter going forward. On an adjusted basis, the quarter was outstanding by any measure.

The market isn’t pricing in what Figure actually reported. It’s pricing in a bunch of fear. The fear of crypto exposure, fear of recent IPOs, fear of growth stocks broadly. And that disconnect between fundamentals and stock price is precisely what creates opportunity.

I believe Figure is an excellent buy for the long-term investor and will continue to prove itself as a massive disruptor in financial services. Here’s why.

What Is Figure?

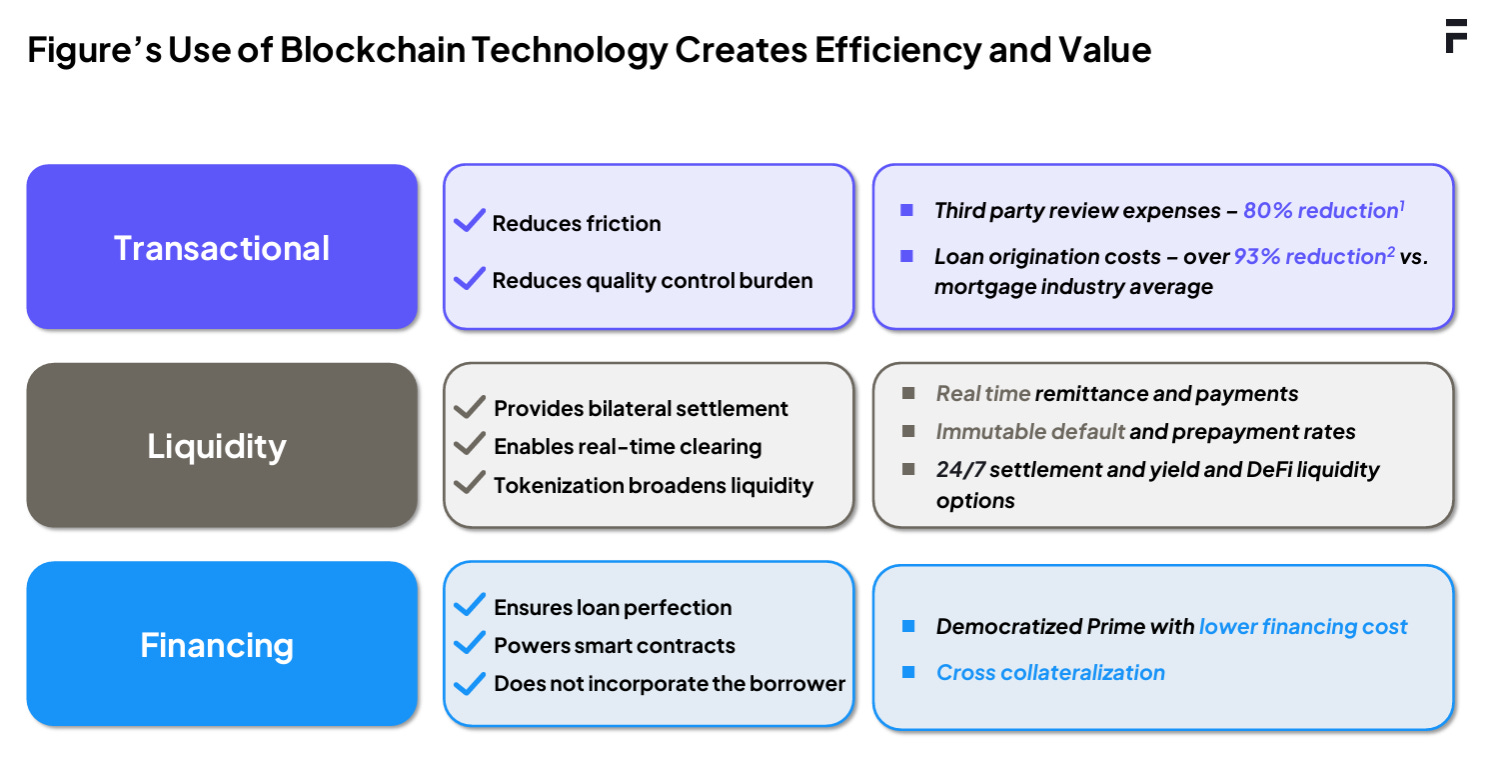

Figure Technology Solutions isn’t just another crypto company. It lives at the intersection of traditional finance and cryptocurrency, showing genuine leadership in on-chain real-world assets. There are many companies that handle crypto well, and many that handle TradFi and capital markets well. Very few navigate both domains with deep understanding and excellence. Figure is a vertically integrated company leveraging blockchain across everything it builds, eliminating friction and realizing extreme efficiency gains that incumbents simply cannot match.

Founded in 2018 by the team that helped build SoFi (including co-founders Mike Cagney and June Ou) Figure is now led by CEO Michael Tannenbaum, who joined from SoFi and Brex roots last year. The company initially set out to prove that you could originate, aggregate, and securitize loans on blockchain and save upwards of 85 basis points in transaction costs. When the banks universally said “We’d love to be the tenth bank to try this,” Figure realized it needed to become the proof of concept itself.

They chose home equity lines of credit (HELOCs) — a product vertical where inefficiency was obvious, margins were attractive, and incumbents were slow to innovate. What traditionally took 30-45 days could be approved in as little as 5 minutes and funded in 5 days. And the savings exceeded expectations: over 117 basis points per loan versus the original 85 bps estimate.

That was the beginning. What Figure has built since is far more ambitious.

The Platform Today: Four Pillars (And A Fifth Emerging)

Figure has evolved from a direct HELOC lender into a vertically integrated capital markets platform with five technological pillars:

Figure LOS (Loan Origination System): White-label software enabling over 307 partners — banks, credit unions, and independent mortgage banks — to originate loans in minutes, not days. Figure does a mortgage for under $1,000 in total cost versus an industry average of $11,045. That cost advantage is structural and widening.

Figure Connect: The capital-light marketplace where partners sell loans directly to institutional investors. In Q4, Connect represented 54% of consumer loan marketplace volume for the first time — a milestone that took just 18 months from launch. This is Figure’s most strategically important asset: it shifts the business from balance-sheet intermediation to high-margin marketplace economics.

DART (Digital Asset Registry Technology): A blockchain-native replacement for MERS (Mortgage Electronic Registration Systems) that handles asset custody, lien perfection, and real-time settlement. The data is 100% immutable and verifiable — the blockchain IS the custodian.

Democratized Prime: An on-chain financing marketplace providing institutional liquidity without traditional prime brokerage overhead. This grew nearly 10x quarter-over-quarter in Q4, from $20 million to over $200 million in matched offers, with 1,000+ active participants. It has nearly doubled again since the start of 2026 to ~$337 million as of mid-February.

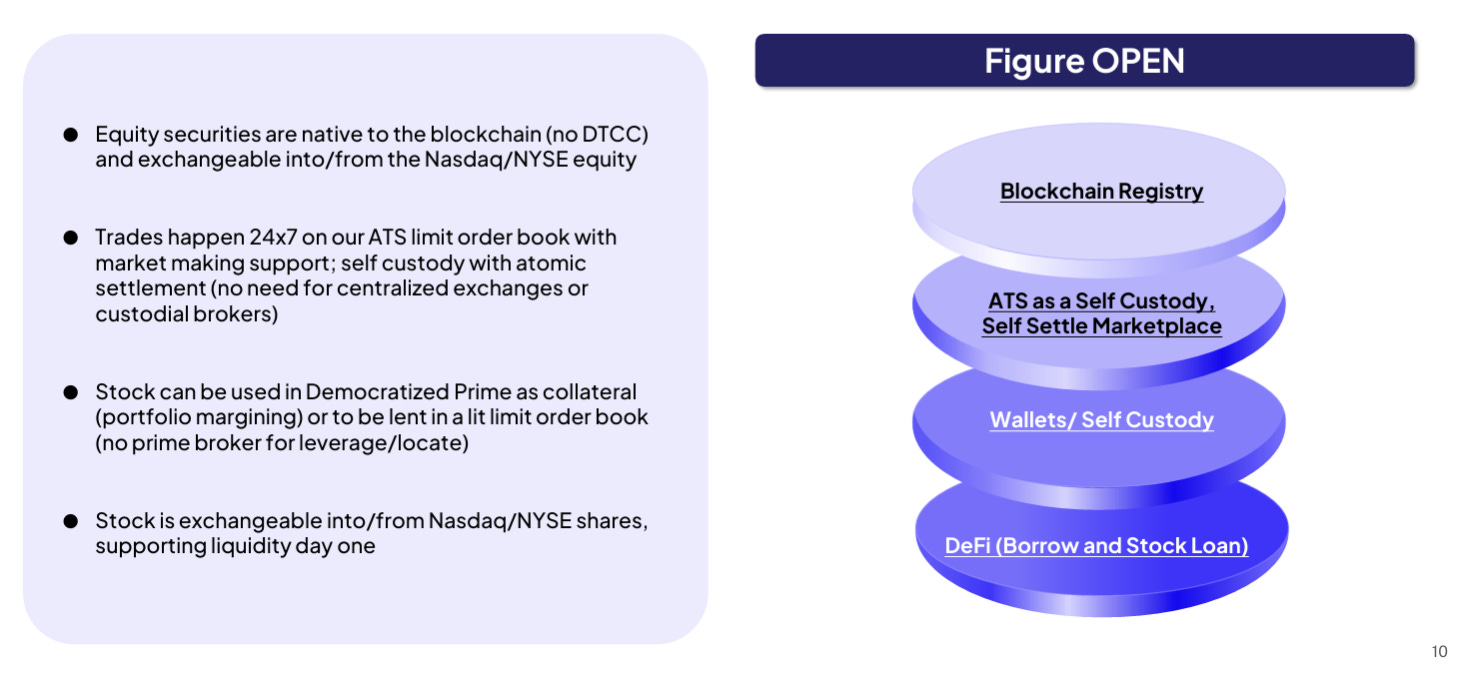

OPEN (On-Chain Public Equity Network): Figure’s newest and highest conviction initiative — a blockchain-native equity issuance and trading platform. Figure became the first public company to launch a blockchain-native share class (FIGD), with 24/7 trading, atomic settlement, and self-custody. While early, this effectively demonstrates an alternative stock exchange infrastructure that Figure happens to own.

The vertical integration is the key. $YLDS (the first SEC-registered yield-bearing stablecoin, now nearing $500 million in circulation) provides the liquidity. Provenance blockchain provides the rails. DART provides the legal registry. Democratized Prime provides the leverage. Every transaction — whether a HELOC origination or a secondary share trade — feeds back into the same proprietary loop, capturing fees that were previously leaked to a dozen legacy intermediaries.

Q4 2025: The Numbers Speak For Themselves

Despite the stock’s reaction, Q4 was unequivocally Figure’s strongest quarter:

Revenue growth accelerated from 55% in Q3 to 91% in Q4. Adjusted EBITDA margins expanded by over 31 percentage points year-over-year, and the company has a clear path to its medium-term target of 60%+ margins — driven by the ongoing shift to capital-light marketplace volume, ~80% contribution margins on partner-branded volume, and extreme operating leverage (volume up 131% while operating expenses excluding SBC grew just 13%).

Full-year 2025 results were equally impressive: $506.9 million in revenue (+49%), $134.3 million in net income (+574%), and $251.2 million in adjusted EBITDA (+148%). This is a company that IPO’d already profitable — a rarity in recent vintages — and is compounding that profitability at scale.

The company ended the year with $1.2 billion in cash and authorized a $200 million share repurchase program, a strong signal of management’s confidence at these levels. We will have full balance sheet metrics when the 10-K is released in coming weeks.

2026: The Year Of Product Expansion

What makes Figure’s growth story particularly compelling is that it’s still early. The company is expanding aggressively across three vectors:

First-Lien Mortgages: “The Year Of The First Lien”

CEO Tannenbaum declared on the earnings call: “2026 will be the year of the first lien for Figure.” First-lien volume grew 3x year-over-year in Q4 to $506 million, now representing 19% of originations (up from 12% a year ago). This is significant because first-lien mortgages are a multi-trillion dollar market — dwarfing the HELOC space where Figure built its name.

Figure’s competitive advantage is stark: a mortgage originated for under $1,000 in five days versus the industry average of $11,045 and weeks of processing. Partners who once viewed Figure as their HELOC outlet now increasingly see it as a comprehensive mortgage platform. The company’s existing partners alone do over $300 billion of first-lien production annually.

While take rates on first-lien loans are modestly lower in basis point terms (due to larger loan balances), the dollar economics per loan are actually higher because unit costs remain the same. Management guided take rates to 3.5%-4% going forward — not from competitive pressure, but simply from this product mix shift.

Auto Lending: A $1.6 Trillion TAM Opens Up

Figure struck a partnership with Agora Data – an AI-powered intelligence platform for auto loan originators – to bring auto finance assets onto Figure’s blockchain rails. This marks Figure’s first foray into the $1.6 trillion auto lending market.

Critically, this is pure margin for Figure. They don’t incur origination or LOS costs as Agora handles that. Figure provides the capital markets infrastructure: tokenization via DART (preventing double-pledging, as seen in the Tricolor bankruptcy), short-term financing via Democratized Prime, and permanent capital distribution via Connect. The partnership is expected to bring tens of millions in auto finance volume in the coming months, with a clear upsell path from Demo Prime financing into Connect whole-loan sales and eventually securitization sponsor fees.

As Tannenbaum put it on the 4Q25 earnings call: “For the auto loan space, the road ahead is paved on-chain.”

SMB Lending & Beyond

Small business lending is another natural extension. Two-thirds of small business owners also own their homes, giving Figure a unique ability to serve asset-rich but liquidity-constrained entrepreneurs. Q4 SMB volume doubled to $46 million, and Figure just announced a strategic partnership with Newtek, a leader in small business financial services, to deliver HELOCs for small business through Newtek’s deep network — with plans to evolve into embedded lending, banking, and money movement anchored by $YLDS.

Additional growth vectors include crypto-backed loans (zero losses to date despite recent volatility), DSCR and residential transition loans, and the continued expansion of Democratized Prime across new blockchain ecosystems including Solana.

The Macro Tailwind: Mortgage Rates Are Falling

An underappreciated catalyst for Figure’s growth is the declining interest rate environment. The 30-year mortgage rate has fallen to 5.94%, down approximately 40 basis points over the past year and roughly 50 basis points over six months — its lowest level since early 2022. The 30-year rate for excellent credit borrowers has fallen even more sharply, down 78 basis points year-over-year to 5.84%.

Source: StreetStats

This matters for Figure in several ways:

HELOC demand strengthens. The millions of homeowners who locked in ultra-low first-lien rates during 2020-2021 have strong incentive to tap home equity via HELOCs rather than refinancing and losing their low rate. As rates decline further, the equity available to borrow against increases.

First-lien origination accelerates. Lower rates directly improve purchase affordability and stimulate refinancing activity — feeding directly into Figure’s “year of the first lien” push. Every 25 basis point decline in mortgage rates meaningfully expands the addressable refinancing pool.

Securitization execution improves. Lower rates generally tighten credit spreads and improve gain-on-sale premiums. Figure already earned its AAA rating from S&P and Moody’s in summer 2025, which significantly boosted securitization execution in Q3 and Q4. Declining rates only amplify this.

Figure’s cost advantage widens. In a more competitive origination environment — which lower rates create — Figure’s sub-$1,000 cost advantage over the $11,045 industry average becomes an even more compelling reason for partners to route volume through Figure’s platform.

Kgil noted on the earnings call that November through February represents seasonal weakness in home lending volumes, and that they anticipate higher growth beginning in March. The combination of seasonal normalization and the ongoing rate decline sets up a strong spring origination season.

On-Chain Activity Is Accelerating

One of the unique advantages of analyzing Figure is that much of its core activity occurs on the Provenance blockchain — meaning we can observe real-time, independently verifiable signals about the health of the business.

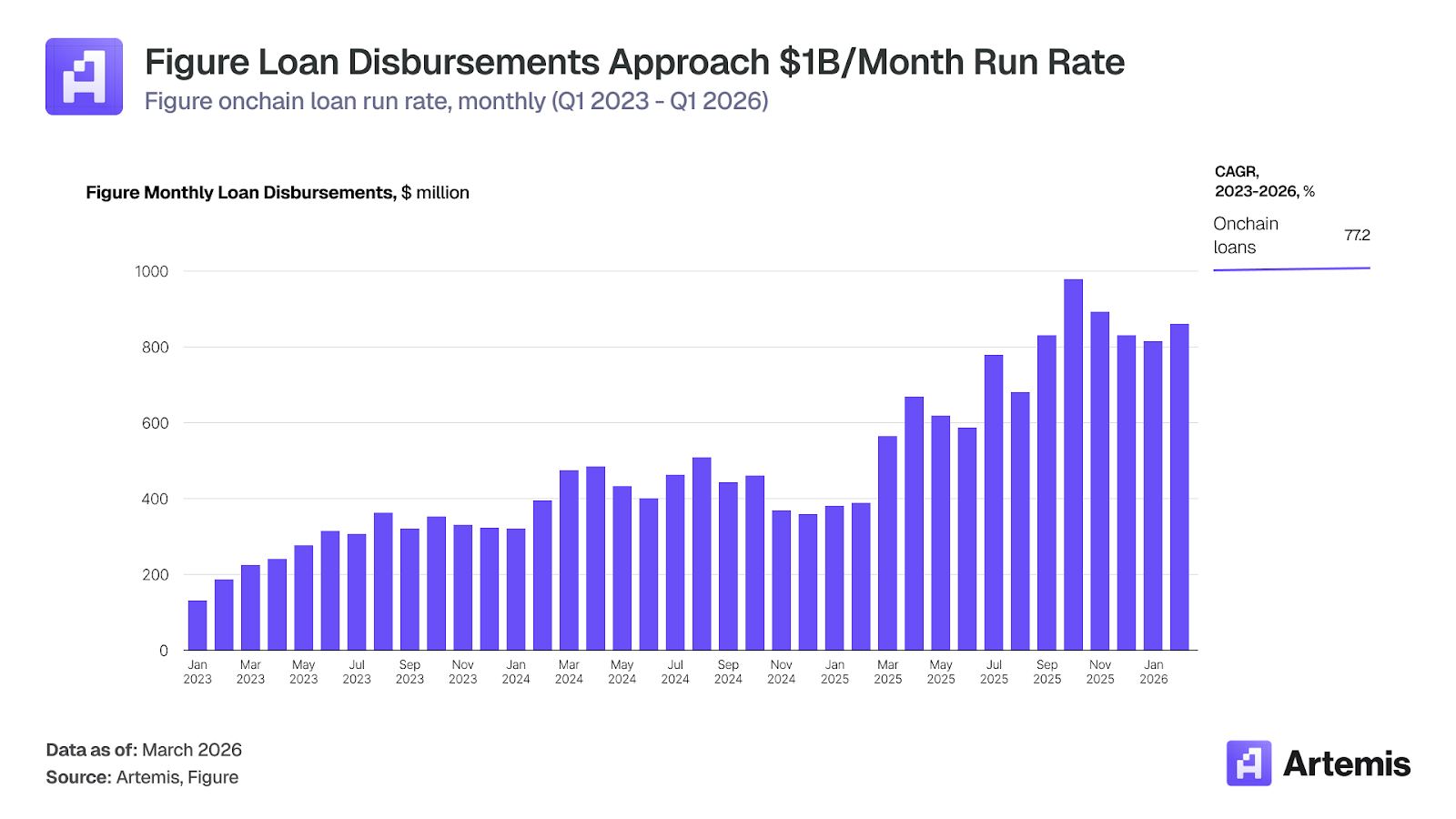

Loan Disbursements Have Grown Significantly

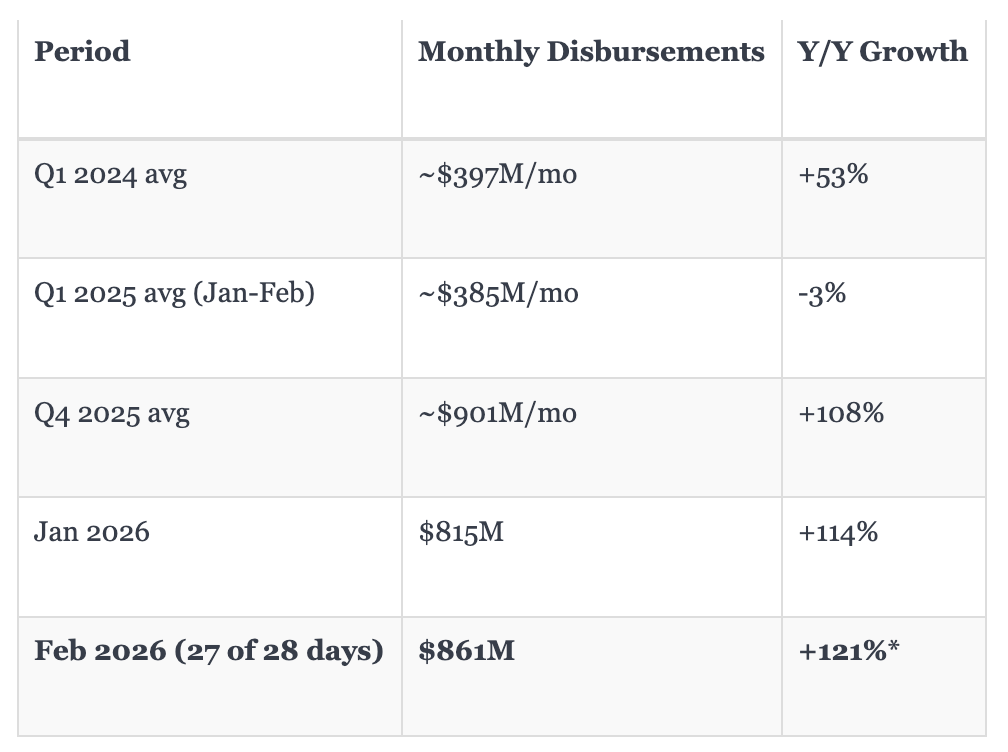

On-chain loan disbursements have grown from approximately $131 million per month in January 2023 to over $860 million in February 2026 — roughly a 7x increase in three years. The monthly trajectory tells the story:

Source: Figure, Artemis Analytics

Here it is in table form:

*Feb 2026 annualized for full month: ~$893M, representing approximately +130% year-over-year growth versus February 2025’s $389 million.

What’s particularly notable is February’s daily average of $31.9 million — the highest daily run rate in the dataset, achieved during what management calls the seasonally weakest period of the year (November through February). Historically, March shows sharp seasonal acceleration: in 2025, March disbursements were 47% higher than the January-February average. Applying that seasonal pattern to the current growth trajectory suggests March 2026 could approach or exceed $1 billion in monthly disbursements.

The year-over-year growth rate in disbursements reaccelerated sharply in mid-2025 and has sustained above 100% for the last several months. This reacceleration aligns with Figure Connect’s scaling (launched June 2024), the expansion into first-lien mortgages, and the broadening partner base.

Source: Figure, Artemis Analytics

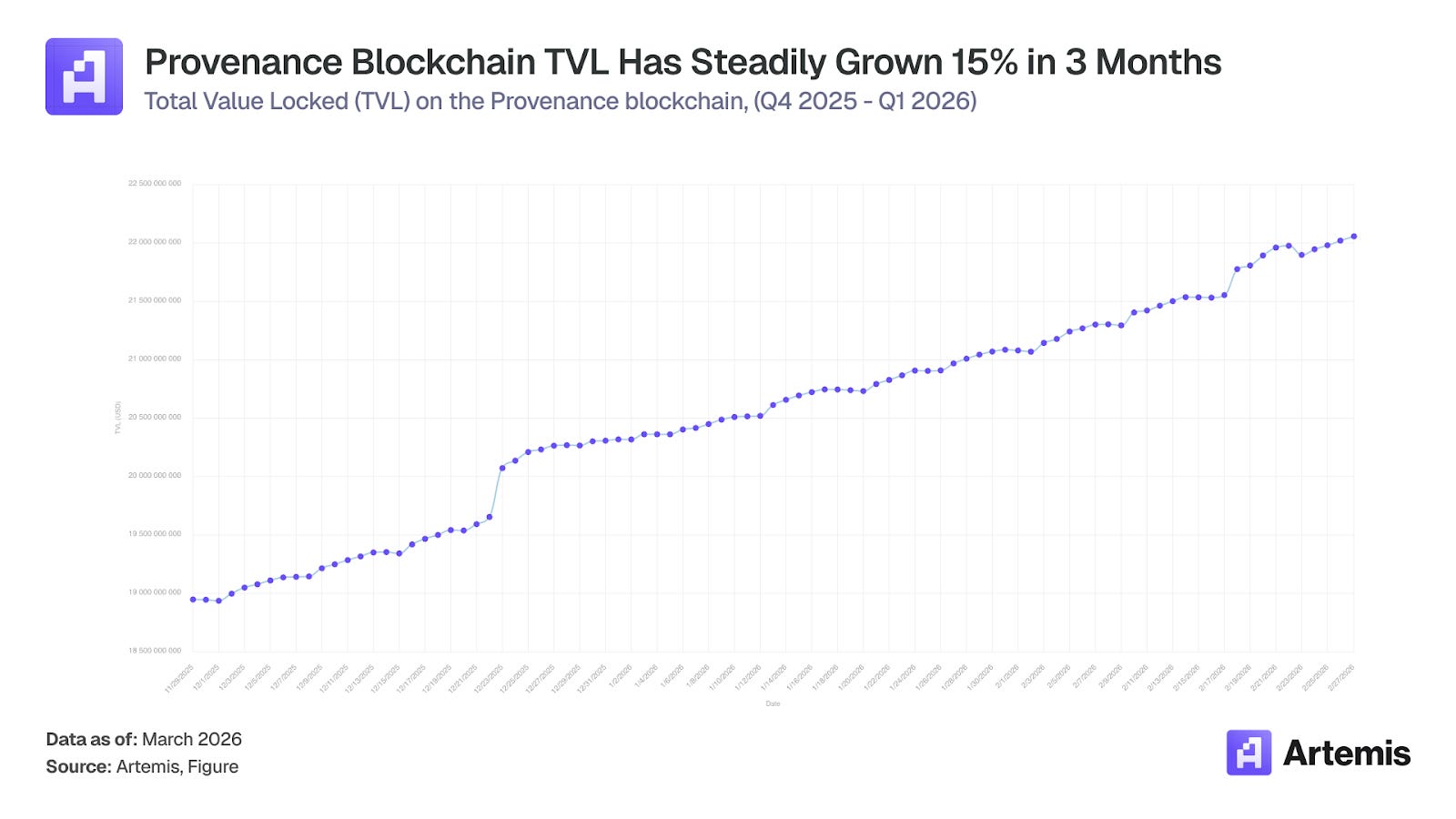

Total Value Locked on the Provenance blockchain — Figure’s native chain — has grown steadily from $18.9 billion in late November 2025 to $22.1 billion as of February 27, 2026. That’s +$3.2 billion (+17%) in approximately three months, reflecting continued adoption of YLDS, Democratized Prime, and the broader tokenized asset ecosystem.

The key takeaway: on-chain activity is accelerating even as the stock price collapses. This is the kind of divergence between fundamentals and sentiment that long-term investors should pay close attention to.

Valuation: Compelling At These Levels

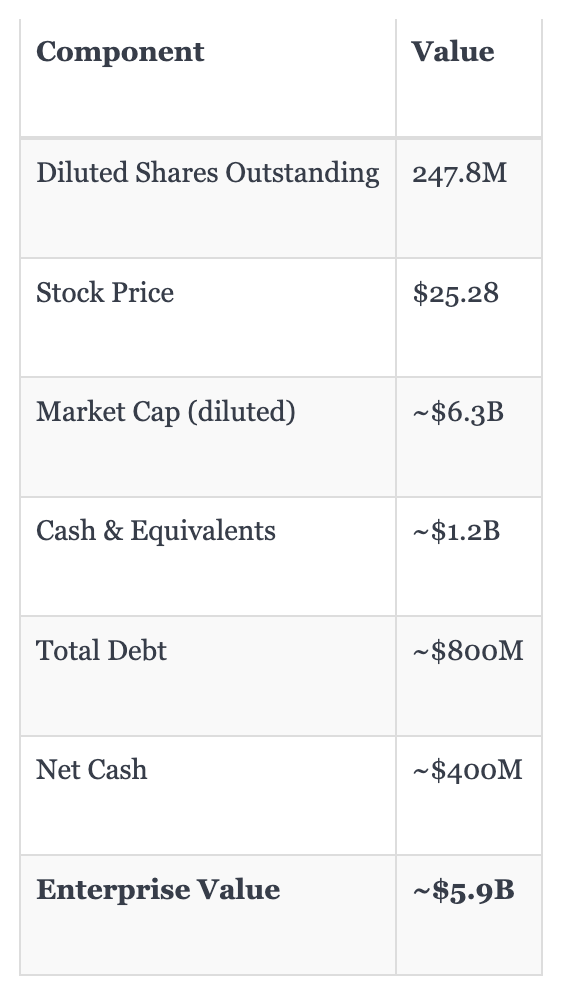

Let’s do the math at $25.28:

*Actual numbers for cash and debt to arrive when FIGR files 10-K. Current disclosures from 8-K and management commentary.

Sell-side FY2026 EBITDA estimates are beginning to trickle in, with a median consensus around $380 million. Against the current enterprise value:

FY2026E EV/EBITDA: ~15.5x

To put this in context: Coinbase (COIN), the number-two crypto exchange, trades at ~17x forward EBITDA. Rocket Mortgage (RKT), which just acquired Mr. Cooper and Redfin to build a vertically integrated mortgage platform, trades at similar levels. Neither can match Figure’s ~2x top-line growth or its 50%+ (and expanding) EBITDA margins.

If Figure hits its 60%+ EBITDA margin target — which the Q4 trajectory strongly supports — and continues growing revenue at anything close to its current pace, the earnings power in 2027 and beyond makes today’s valuation look remarkably cheap. Even modest multiple expansion from 15.5x back toward the 20-25x range typical for high-growth financial infrastructure companies would imply significant upside from current levels.

The $200 million buyback authorization provides a further floor. At $25.28 per share, that represents approximately 7.9 million shares — over 3% of the diluted float — and management has signaled they will execute in a disciplined manner consistent with their confidence in the business.

Addressing The Bear Case

The BofA downgrade raises legitimate questions worth addressing:

“Large banks may not adopt the LOS.” This is true — and largely irrelevant to the near-term thesis. Figure’s growth is being driven by independent mortgage banks, credit unions, and non-licensed partners (fintechs, SMB channels, real estate investors). The company added partners at a 25% sequential clip in Q4, reaching 307 — and Tannenbaum confirmed this is a leading indicator of continued strong volume growth. Large bank adoption would be additive but isn’t required to justify the current valuation.

“Large banks don’t need Connect because they hold loans on balance sheet.” This misunderstands the platform’s value proposition. Connect’s power is in connecting smaller and mid-size originators — who don’t have balance sheet capacity — with institutional buyers. The fact that 54% of volume already flows through Connect validates the model. Large banks may eventually participate as buyers, not sellers, on Connect — and the Agora partnership demonstrates how third-party asset classes can be layered onto the platform without bank participation at all.

“Crypto exposure creates volatility.” Figure Exchange (the crypto trading platform) contributed roughly one quarter of Q4 revenue. While this introduces some earnings variability, the core lending business — origination fees, servicing fees, gain on sale, and interest income — accounted for the majority of revenue and is growing steadily. Crypto-backed loans have experienced zero losses to date, even through recent volatility.

“The EPS miss signals weakness.” As discussed, the GAAP miss was entirely SBC-driven and non-recurring. Adjusted EBITDA grew 426% and margins expanded 31 percentage points. This was not an earnings miss in any meaningful operational sense.

Risks

No investment is without risk. Key risks for Figure include:

Macro deterioration that reduces home lending demand, though declining mortgage rates currently mitigate this

Crypto market volatility affecting Figure Exchange revenue and sentiment overhang on the stock

Regulatory changes to blockchain-based financial infrastructure, stablecoins, or securitization

Execution risk in scaling new product verticals (auto, first-lien, SMB) simultaneously

Concentration risk in home equity products, which still represent the majority of origination volume

Security incidents, as evidenced by the recent phishing attack affecting ~12,400 individuals (though not blockchain-related and not expected to be material)

Conclusion

Figure Technology Solutions just delivered a quarter that validated its entire thesis — accelerating revenue growth, expanding margins, surging marketplace adoption, and successful entry into new product verticals — and the market responded by delivering its worst single-day decline since going public.

The disconnect is stark. On-chain data shows loan disbursements running at 7x the levels of three years ago and still accelerating. Provenance TVL is growing by billions per month. Mortgage rates are falling to multi-year lows, setting up a strong spring origination season. The company has $1.2 billion in cash, a $200 million buyback program, and a clear path to 60%+ EBITDA margins.

At ~15.5x FY2026E EV/EBITDA — cheaper than Coinbase, cheaper than Rocket Mortgage, and growing faster than both — the market is offering you a vertically integrated financial infrastructure platform at a balance-sheet lender’s multiple.

Disclosure: This material is provided for informational purposes only and does not constitute investment advice, financial advice, trading advice, or any other form of advice. The views expressed are those of the authors and should not be relied upon as a recommendation to buy, sell, or hold any asset. The authors or affiliated entities may hold positions in the assets discussed. You should conduct your own research and consult appropriate financial professionals before making any investment decisions.