Figure: Reducing Friction With Blockchain To Build A Better Lending Infrastructure

Why reducing friction with blockchains to build a better lending infrastructure is helping Figure become a leader and beneficiary of RWAs.

“... when you remove friction, you unlock non linear-behavior” (Invest Like The Best Podcast, Modest Proposal)

Hey Fundamental Investors,

Jon here co-founder/CEO of Artemis. Our mission is to find and highlight the winners of digital finance (stablecoins, prediction markets, RWAs, DeFi, etc) using data.

We realize digital finance is lacking in strong sell-side research on the top crypto equities and tokens and so we’re bringing back deep dives by world class analysts.

We’ve previously did Fundamental Deep Dives on:

Today we have Tiago Souza, Research Analyst at Artemis, share his deep dive of Figure, which is up 50% in the last 3 weeks.

Figure is an important stock to understand for digital finance investors given they leverage blockchains to reduce friction for lending and are building a marketplace for tokenized loans.

Our view is that both equity and token businesses will benefit from blockchains and digital finance — we cover both so fundamental investors can properly allocate.

Without further ado, here is Tiago’s memo for Figure:

Figure: Reducing Friction With Blockchain To Build A Better Lending Infrastructure

By: Tiago Souza

Conclusion: We view Figure as a Buy, with a 2030 target price of $116, implying a 20% IRR over the period. Figure is at ~$500M revenue (50% yoy) with ~$200M Net Income, trading at 30x Net Income 2027. Figure began as a B2C HELOC lender, using blockchain technology to streamline the credit cycle end-to-end, and subsequently expanded by offering this infrastructure to financial partners. It is now scaling the core business and evolving into a marketplace for tokenized loans, built on proprietary blockchain rails that materially improve efficiency for lenders, originators, borrowers, and investors. While the opportunity is substantial, the downside is real. Given that this is a growth thesis, failure to scale would leave the business subject to a significant downside.

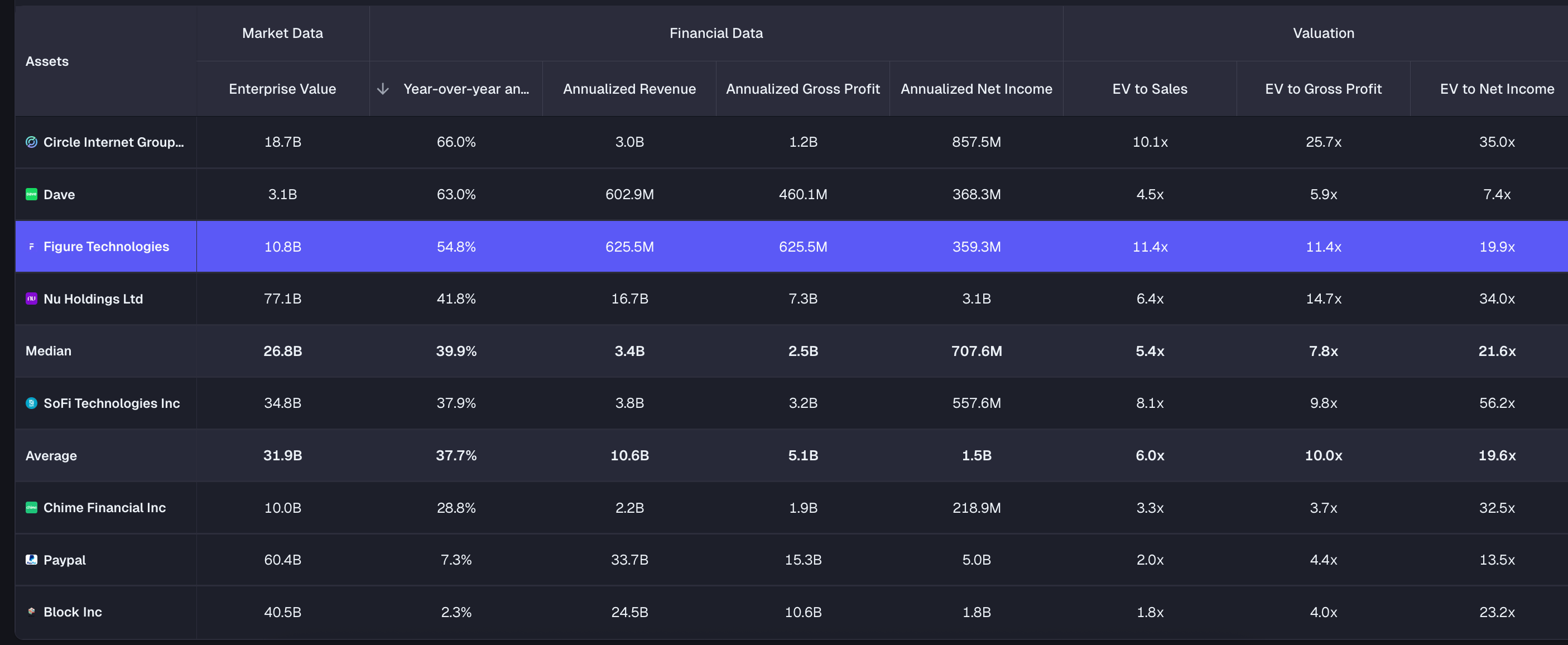

Comps Table: Figure is one of the fastest-growing companies in the crypto-adjacent world (note these metrics are using last quarter metrics and annualizing them)

Why Now? What was once perceived as an experimental crypto-adjacent lender has now demonstrated its ability to originate, service, and distribute high-quality credit through a fully digital and structurally more efficient stack. Following its IPO in September 2025, investors only recently gained access to the company through public markets, at a stage when Figure had already established a robust and scalable value proposition in HELOCs. As a newly listed and still undercovered name, the company is now expanding into additional credit products and building a marketplace for the on-chain distribution and settlement of tokenized loans, building blocks designed to support highly profitable, sustainable long-term growth.

What does Figure do? Figure is a US-based fintech that leverages blockchain technology to make the origination, processing, and trading of loans more efficient than traditional lenders. Founded in 2018, Figure operates a digital-first, non-bank HELOC lending platform and has become the leading non-bank originator in the U.S. HELOC market (a $420B+ market in credit outstanding).

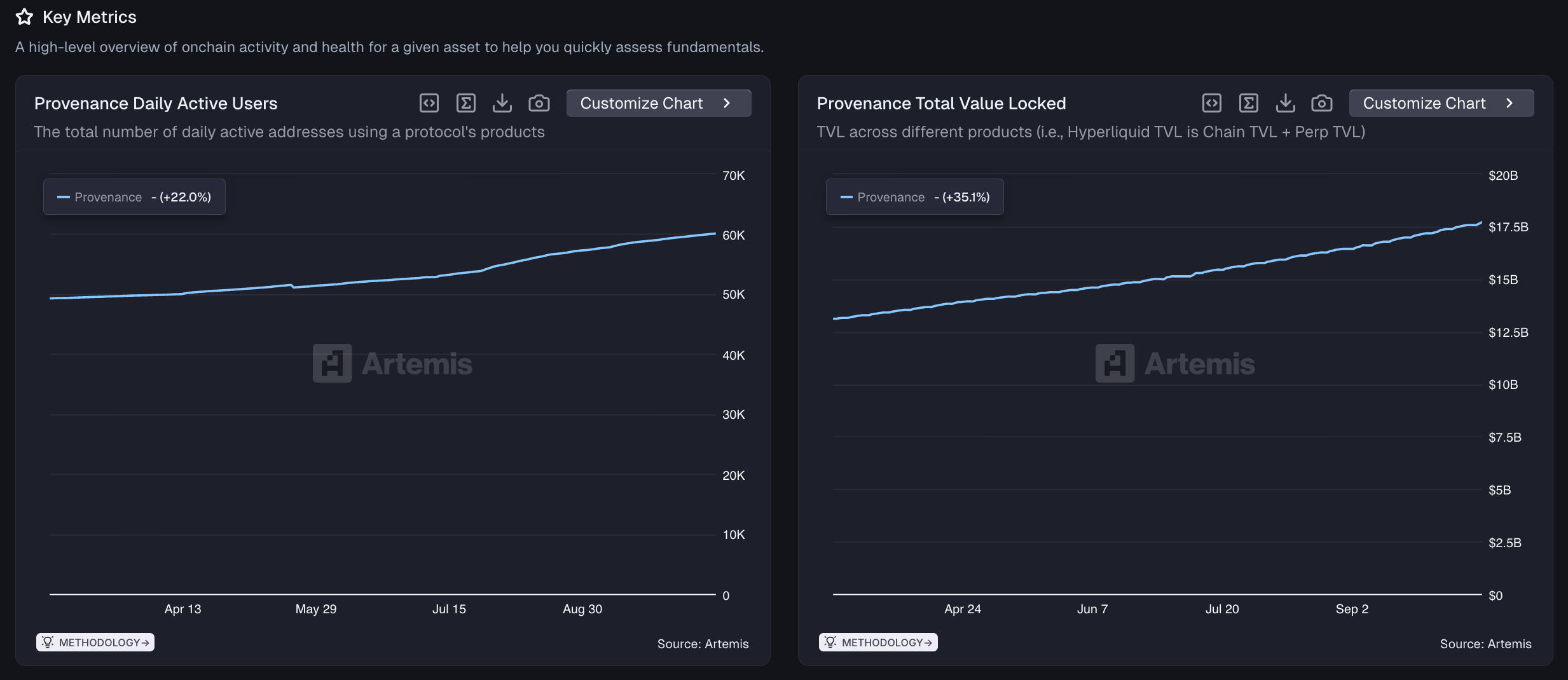

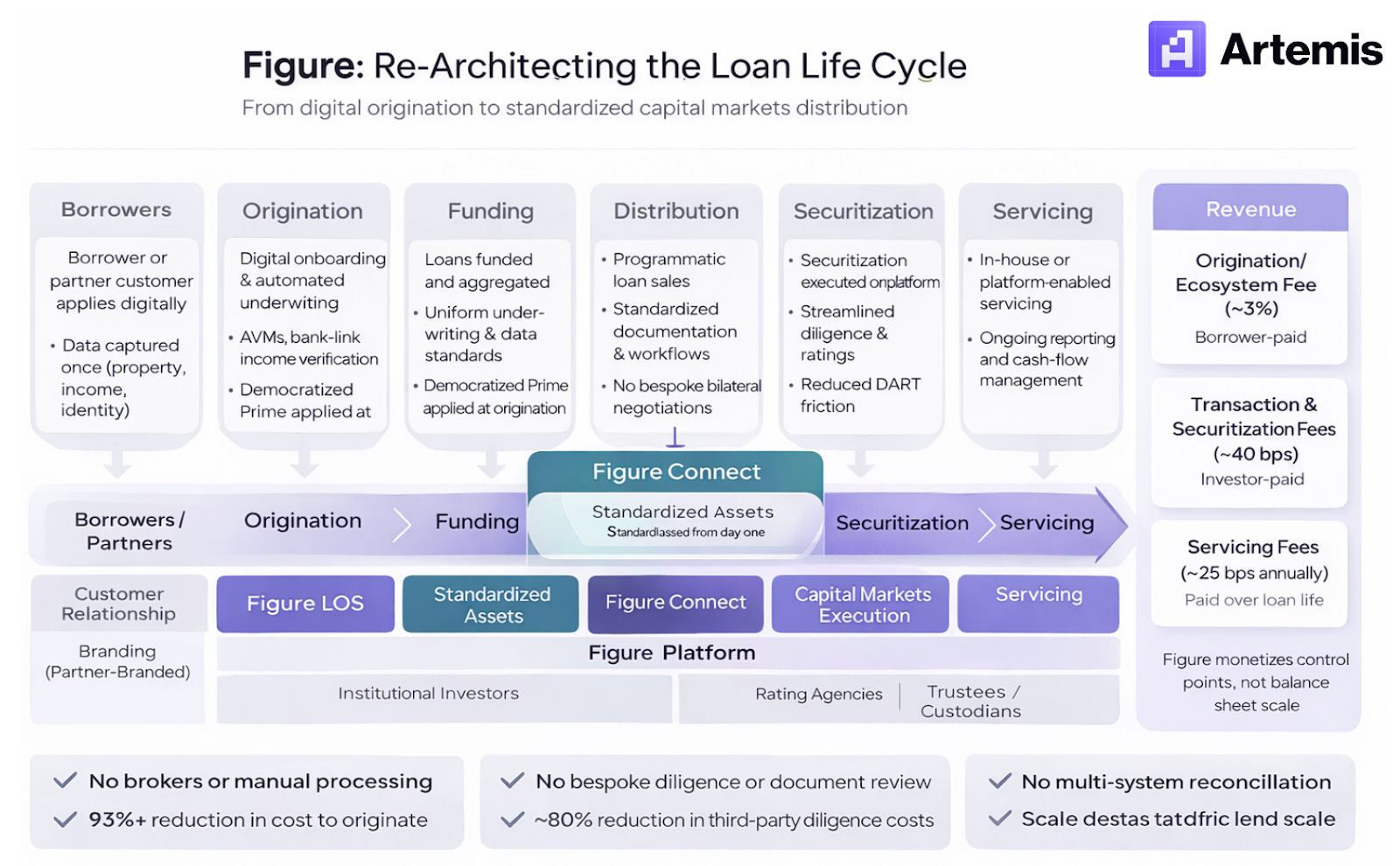

A key component of Figure’s infrastructure is its Loan Origination System (LOS): a fully digital platform that manages the entire lending process, from application submission and underwriting to verification, approval, and closing. Unlike traditional LOS platforms, Figure’s is built natively on the Provenance Blockchain, recording each loan as a hashed, tamper-proof asset on chain. Tracking the health of Provenance Blockchain is an indication of a healthy business for Figure. Artemis’ Dashboard shows steady growth in Daily Active Users (35% CAGR from March to October 2025) and Total Value Locked for Provenance (56% annualized growth in the same period).

This approach eliminates multiple costly manual reconciliations and provides a single, verifiable source of truth for all parties involved in the credit cycle. As a result, many of the intermediaries and process steps that define traditional HELOC origination are either eliminated or materially compressed.

“What stands out with Figure is how fast it is. A HELOC that might take 30 to 45 days at a bank can be done in days if the AVM and title come back clean.” (Mortgage Advisor)

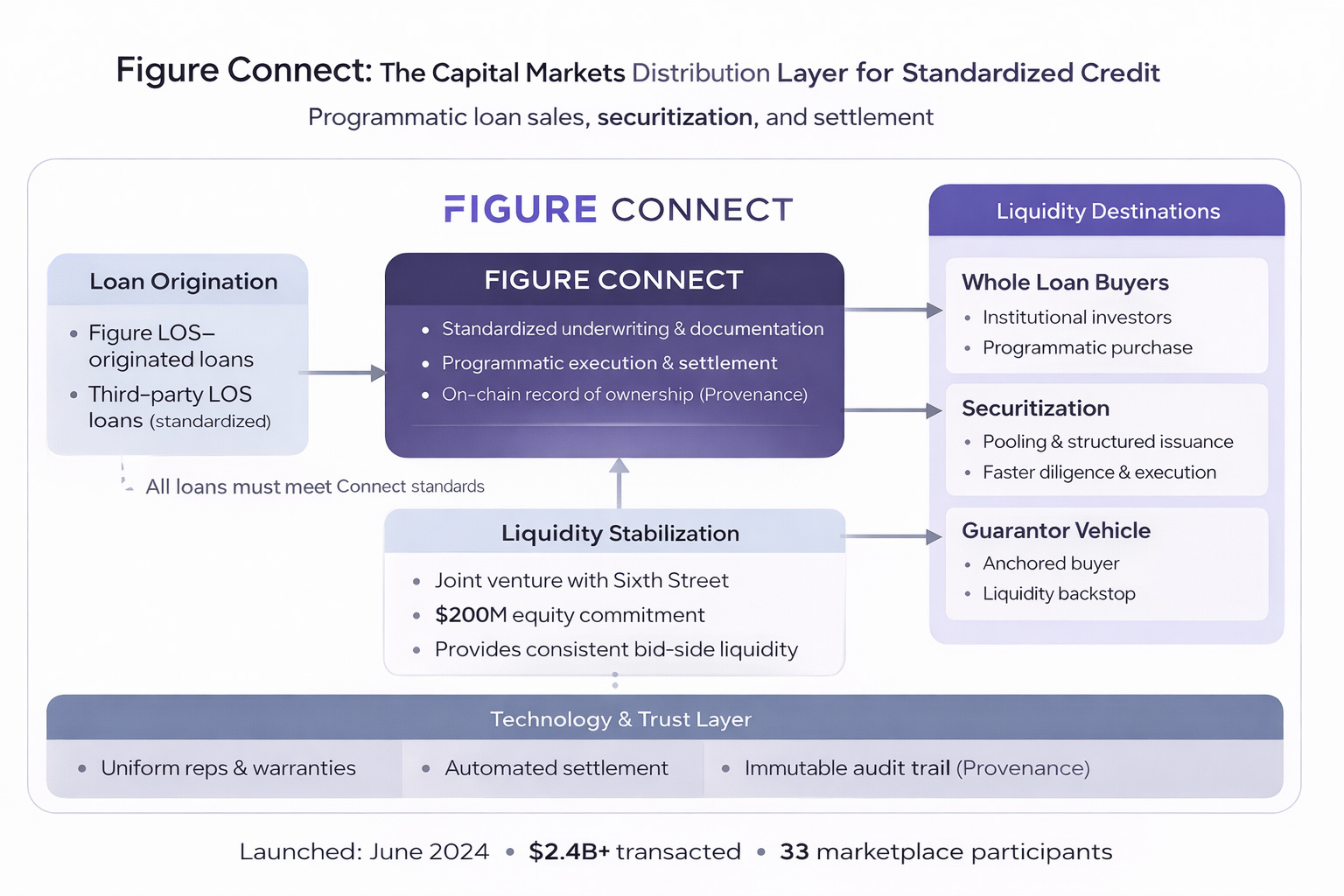

Beginning in 2020, this infrastructure was commercialized beyond Figure’s direct consumer channel, segmenting the business into two complementary operating lines: Figure-Branded and Partner-Branded, which together scale origination across both direct and embedded distribution models. Complementing these origination engines is Figure Connect, FIGR’s blockchain-native capital markets marketplace, which extends the platform downstream by reducing friction between loan originators and institutional investors.

Figure-Branded is the company’s direct-to-consumer lending channel, where borrowers interact directly with the Figure brand and FIGR controls the end-to-end product experience (from digital onboarding and automated underwriting to pricing, servicing, and compliance), monetizing through origination fees, servicing fees, and gain-on-sale economics.

Partner-Branded extends the same technology stack to fintechs, banks, credit unions, and other originators in a B2B2C model, allowing partners to offer modern digital lending products under their own brand while FIGR provides the underlying loan origination system, underwriting, compliance, servicing tools, and data infrastructure, earning technology and ecosystem fees tied to partner loan volumes.

“From a broker perspective, the amount of work per deal is much lower with Figure. The system pulls bank data, income, and valuation automatically. You’re not chasing documents the same way.” (Senior Loan Officer at a Mortgage Origination Partner)

Figure Connect enables Figure-Branded and Partner-Branded loans to be distributed to institutional investors through standardized, programmatic workflows, rather than bespoke bilateral transactions, anchored by Democratized Prime, which enforces uniform underwriting, documentation, and data standards inside Figure’s ecosystem. Blockchain underpins funding and post-origination as a system of record for ownership and settlement, with transactions settling via YLDS, FIGR’s SEC-registered, yield-bearing token. FIGR earns transaction and technology fees, positioning Connect as a marketplace layer that enhances liquidity and execution efficiency in private credit markets.

Competition. Figure operates in a fragmented and uneven competitive landscape that spans mortgage technology, consumer lending, and emerging tokenized credit markets, but it faces no true peer that competes across its full vertical stack. In HELOC origination and technology, its primary competitors are large banks and scaled mortgage platforms such as ICE/Black Knight and Rocket, which benefit from distribution and scale but rely on legacy, non-blockchain systems and prioritize first-lien mortgages rather than HELOCs. In this context, Figure has established itself as the #1 non-bank HELOC lender by leveraging a differentiated, largely automated loan origination system that materially reduces cost and time to fund.

Thesis #1: Figure has a proven core business that benefits from scale economies. As it expands across the $35T home-equity-back market, Figure-Branded/Partner are positioned to grow mid-30s 5Y-CAGR, while expanding the scale moat.

Figure is entering its next phase of growth by extending its proven origination, funding, and distribution platform beyond HELOCs into the broader home-secured lending market. Its core advantage—materially lower fixed costs to originate and distribute loans (allows Figure to profitably serve segments that are structurally uneconomic for traditional lenders). As volumes scale over the next 18 months, these scale economies reinforce cost leadership and expand Figure’s competitive moat, positioning the company to reduce friction and unlock value across a ~$35 trillion U.S. home-equity–backed credit market.

“Initially, Figure did a lot of the operational work for partners. Over time, partners started running their own pipelines inside the platform, which is where the real scalability comes from.” (Former Director of Product at Figure)

This strategy is already supported by a scaled, profitable operating core across Figure-Branded and Partner-Branded channels, with over $19 billion in cumulative originations and more than $1 billion in monthly volume, while maintaining high credit quality (average FICO ~754). Growth has been driven by operational efficiency—not looser underwriting—with loans originated in roughly five days at a fraction of traditional costs. As partners integrate more deeply into the platform and manage their own pipelines, operating leverage improves and technology revenue becomes increasingly recurring.

“Figure is more conservative than some other HELOC fintechs. They don’t stretch the credit box as much, which is why they lose some volume but keep credit quality high.” (Former Director at Figure)

Despite this progress, Figure’s penetration remains well under 1% of the addressable market, not because of weak demand but because traditional mortgage economics impose a high minimum viable loan size. Mortgage origination costs are largely fixed (typically $11k–$12k per loan) meaning unit economics deteriorate sharply as loan balances decline. At those cost levels, a $100k–$200k mortgage can carry origination costs equivalent to 6–12% of principal, rendering such loans uneconomic for most lenders regardless of credit quality. As a result, incumbents rationally concentrate capacity on larger balances, leaving a structurally underserved segment of borrowers and use cases below the industry’s economic floor.

Figure’s model alters this constraint by materially reducing fixed origination costs and cycle time, shifting the break-even point downward. By compressing production costs to roughly ~$1k per loan and reducing time-to-close from weeks to days, Figure enables profitable origination at loan sizes that are systematically avoided by traditional lenders. This does not merely reallocate existing volume; it activates latent demand from creditworthy borrowers whose financing needs fall below incumbent thresholds. As Figure scales, this dynamic expands the effective servable market, allowing penetration to grow through demand creation rather than direct displacement, an outcome that supports sustained volume growth alongside margin expansion.

“I think, particularly as you move from analog to digital, the holy grail there is two things. One is providing the stereotypical the term is a 10x better experience, but if you can provide a meaningfully better consumer experience in a digital environment that is step one towards building a big business. And the second thing is, oftentimes that 10x experience is consistent with removing friction from a process.” (Invest Like The Best Podcast, Modest Proposal)

Our base case assumes Figure reaches approximately $20 billion in annual originations by 2030. This outcome requires less than 1% penetration of total U.S. home-secured lending flow and roughly 4% penetration of the economically addressable segment where Figure’s low-cost model is most relevant. Given the company’s current ~$12 billion annualized run rate origination, early-stage partner adoption, and expanding product set within mortgage, this implies low-teens annual growth—well below historical execution. Importantly, this volume level can be achieved primarily through deeper penetration of existing partners and activation of smaller-balance demand that traditional lenders structurally avoid, rather than through aggressive market share capture. At $20 billion of volume, Figure’s scale economies and operating leverage remain firmly intact, supporting continued margin expansion and moat deepening beyond the forecast horizon.

Thesis #2: FIGR’s marketplace transition creates a scalable platform with network effects, supporting further growth with high margins.

Figure Connect has already demonstrated early product–market fit as a capital-markets marketplace, with approximately $3 billion of cumulative transaction volume since its launch in mid-2024.

The goal was never just to do HELOCs. Provenance and DART were designed to support any financial asset marketplace, not just mortgages.” (Former Director of Product at Figure)

Notably, this volume has been achieved while the platform remains in its formative stage, limited to Figure-originated loans and only beginning to benefit from structural liquidity enhancements such as the guarantor vehicle. Connect’s core value proposition is not tokenization for its own sake, but rather execution certainty, asset standardization through Democratized Prime, and reliable liquidity, features that directly address the primary friction points in private credit markets. Democratized Prime, defines uniform underwriting criteria, documentation standards, and data structures so that assets are consistently formatted and readily tradable. While blockchain is not central to borrower-side origination, it plays a critical role at funding and post-origination by acting as a system of record for ownership, settlement, and transfer. Transactions settle using YLDS, Figure’s SEC-registered, yield-bearing token, enabling atomic settlement and balance-based monetization rather than transaction-by-transaction fees. As these capabilities mature and adoption broadens, Connect’s relevance to both originators and investors should continue to increase.

“Democratized Prime was about forcing standardization—same underwriting, same docs—so assets could actually trade at scale instead of every deal being bespoke.” (Former Director of Product at Figure)

Looking ahead, Figure Connect is well positioned to scale annual marketplace transaction volumes to approximately $9 billion by 2030. This should be driven by: (1) deeper routing of Figure-Branded and Partner-Branded production through the marketplace, (2) onboarding of non-Figure LOS assets, allowing marketplace volumes to scale independently of origination software adoption, and (3) expanding investor participation as liquidity deepens and execution risk declines.

From a monetization perspective, Figure Connect’s economics extend beyond a narrow “trading fee” construct. The platform generates ecosystem and technology revenues, including transaction execution fees, platform access fees, program fees tied to securitization and distribution, and ancillary technology services embedded in the capital-markets workflow. Combining $9 billion of annual marketplace transactions, substantially higher recurring balances distributed and managed through Connect, and expanded participation across multiple asset classes, Figure Connect could plausibly generate ~$300–320 million of annual revenue by 2030. This implies an effective monetization rate in the low-single-digit percent range.

Optionalities. Beyond its core HELOC and mortgage businesses, Figure’s long-term optionality lies in evolving from a lender into foundational capital-markets infrastructure. Management has consistently framed the platform as asset-agnostic, enabling expansion into additional consumer and commercial credit products, third-party loan distribution, and standalone servicing and settlement services. As Figure Connect scales, the same blockchain rails that compress credit settlement from weeks to minutes could be extended to tokenized equities and other real-world assets, creating a unified on-chain marketplace for issuance, clearing, custody, and secondary trading.

Valuation Framework and Scenarios

High (Upside Case):

Assumes accelerated marketplace adoption, with Figure Connect reaching ~$15 billion in volume by 2030, and Branded/Partner volumes growing near 40%, translating into incremental operational efficiencies improving margins.

Exit in December 2029 at a 35× P/E multiple (based on 2030 earnings).

Price target of $232 per share and an implied 42% 5-Year IRR.

Base Case:

Assumes continued execution and adoption, with consolidated volumes compounding in the low-30s range over the next five years and spreads remaining at current levels.

Figure Connect scales to approximately $10 billion in volume, reaching $320M+ in revenues.

Exit at the end of 2029 at a 30× P/E multiple (looking to 2030 earnings), resulting in a price target of $116 per share, an implied 107% upside with a 20% 5-Year IRR.

Low (Downside Case):

Assumes the thesis does not play out: growth fails to materialize, marketplace adoption stalls, and consolidated volume growth decelerates to mid–single digits.

Exit the investment in December 2027 with a 20x forward P/E, reflecting limited growth visibility.

Results in a price target of $22 per share, implying approximately 61% downside from current levels, translating into a -37% IRR in the same period.

Management Overview

Management quality is a central pillar of this investment case, particularly given the company’s asymmetric downside if the business fails to scale. The team is disciplined, capital-markets fluent, and execution-oriented, with a focus on reliability, standardization, and liquidity rather than narrative-driven innovation. The transition from founder-led building to professionalized execution appears well timed: Mike Cagney provides strategic continuity as Executive Chairman, while day-to-day leadership is focused on scaling partnerships and converting early product–market fit into capital-light economics.

Mike Cagney, Co-Founder (2018); Executive Chairman (since April 2024): Cagney is a serial fintech founder who previously founded or co-founded Finaplex (acquired by Broadridge), Cabezon Investment Group, SoFi, Provenance Blockchain, and Figure. He founded Figure in 2018 and led it as CEO through its build-out and initial scale before transitioning to Executive Chairman in April 2024. He stepped down as CEO of SoFi in 2017 following workplace-culture controversies that became a distraction to the company, after which he shifted focus to building blockchain-native financial infrastructure at Figure. As Executive Chairman, he maintains strategic oversight and long-term control while day-to-day execution sits with the operating team.

Michael Tannenbaum, CEO (since April 2024): Tannenbaum was appointed CEO in April 2024 as Figure entered its institutional-scaling and public-company phase. His mandate is execution rather than invention: professionalizing operations, scaling partner distribution, and ensuring liquidity depth on Figure Connect so marketplace revenues outgrow balance-sheet activity. His appointment signals a deliberate shift from founder-led building to repeatable, enterprise-grade execution—critical for validating the marketplace model and supporting a higher multiple.

Macrina Kgil, CFO (since December 2024): Kgil joined as CFO in December 2024, coinciding with Figure’s transition to public markets and increasing investor scrutiny. Her role is central to articulating the economic logic of the platform: marketplace take rates, capital efficiency, margin durability, and returns on invested capital as Figure de-emphasizes lending. The timing of her hire reinforces management’s confidence that the business is moving from experimentation to measurable, scalable monetization.

Note on Recent Secondary Offer. What Happened? On November 17, 2025 Figure announced that it had filed a registration statement for a proposed offering of “Series A Blockchain Common Stock,” a first-of-its-kind, blockchain-native class of equity securities that will trade on its own alternative trading system and settle on the Provenance Blockchain. The offering is structured as a non-dilutive secondary transaction in which existing shareholders will sell shares and the company will hold an equivalent number of Class A shares in treasury, with the new blockchain stock convertible one-for-one into traditional Nasdaq-listed Class A stock. Timing for pricing and closing is subject to SEC approval. This initiative supports Figure’s strategy of embedding capital-markets infrastructure on-chain: enabling 24/7 trading, self-custody settlement, direct lending/borrowing through Democratized Prime, and settlement in YLDS, all intended to catalyze adoption of decentralized settlement and marketplace mechanics beyond loan products.

Disclosure: This material is provided for informational purposes only and does not constitute investment advice, financial advice, trading advice, or any other form of advice. The views expressed are those of the authors and should not be relied upon as a recommendation to buy, sell, or hold any asset. The authors or affiliated entities may hold positions in the assets discussed. You should conduct your own research and consult appropriate financial professionals before making any investment decisions.