Bitcoin Needs Its Queen: ETH's Evolution into a Scarce, Productive, and Institutional Reserve Asset

Why ETH Is the Reserve Asset of the Onchain Economy.

Hey Fundamental Investors,

Jon here again from Artemis.

We’ve deep-dived: Strategy, CoreWeave, Coinbase, Circle, and Hyperliquid.

Lately, there’s been renewed interest in Ethereum—especially with the emergence of ETH treasuries. Our fundamental analyst has explored a valuation framework for ETH and built a compelling long-term bull case. As always, we’re happy to connect and exchange ideas—remember to do your own research (DYOR).

Let’s dive into ETH with our fundamental analyst, Kevin Li.

Executive Summary:

Ethereum (ETH) is transforming from a misunderstood asset to a scarce, programmable reserve asset, securing and powering a rapidly institutionalizing on-chain ecosystem.

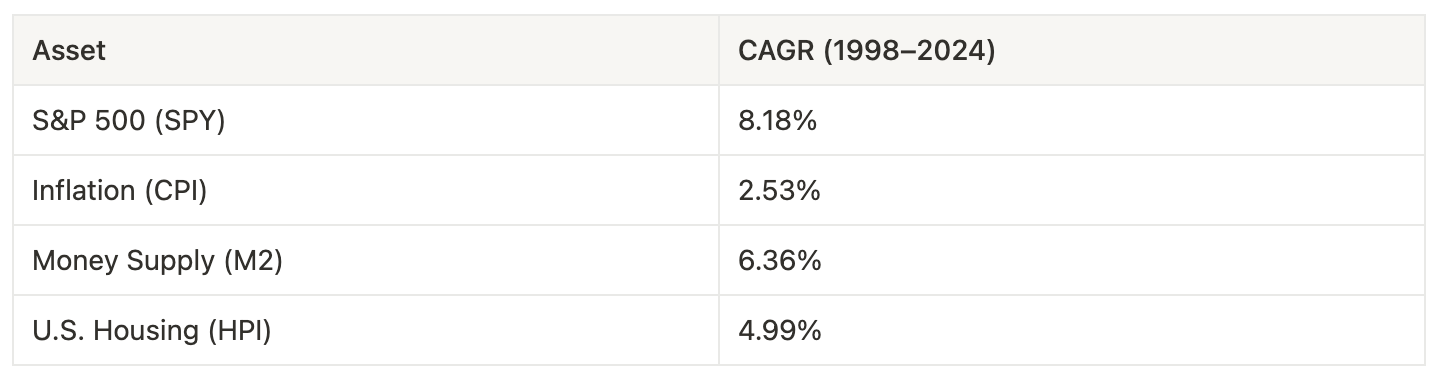

ETH's adaptive monetary policy projects a declining inflation rate—capped at ~1.52% even if 100% of ETH is staked, and trending down to ~0.89% by Year 100 (2125). This is well below the U.S. M2 money supply’s 6.36% annual expansion (1998–2024) and even rivals gold’s supply growth.

Institutional adoption is accelerating, with firms like JPMorgan and BlackRock building on Ethereum—driving sustained demand for ETH to secure and settle value on-chain.

An 88%+ annual correlation between on-chain asset growth and native ETH staking highlights strong economic alignment.

The SEC’s May 29, 2025, policy clarification on staking has reduced regulatory uncertainty. Ethereum ETF filings now include staking provisions, enhancing both returns and institutional alignment.

ETH’s deep composability makes it a productive asset—used in staking/restaking, as DeFi collateral (e.g., Aave, Maker), AMM liquidity (e.g., Uniswap), and as the native gas token across Layer 2s.

While Solana has gained traction in meme coin activity, Ethereum’s stronger decentralization and security position it to dominate high-value asset issuance—a far larger and more durable market.

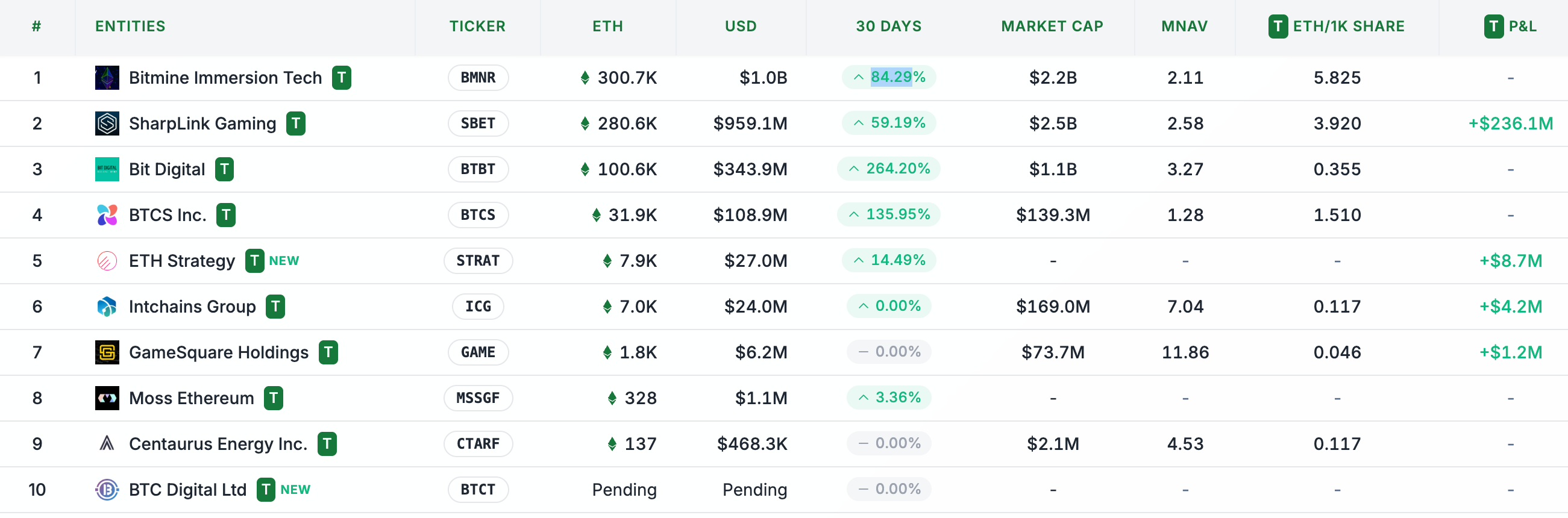

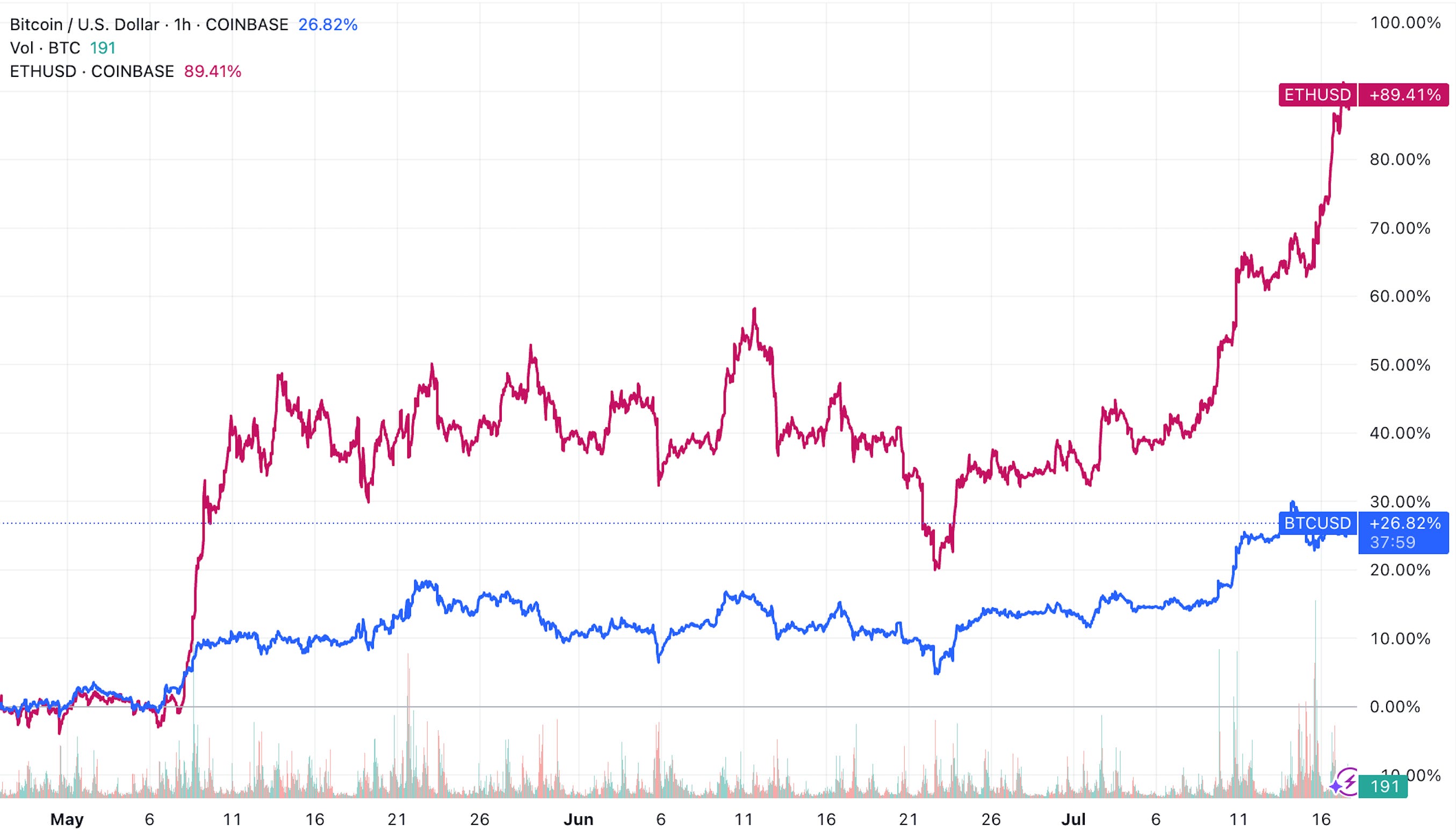

The rise of Ethereum treasury plays, kicked off by Sharplink Gaming ($SBET) in May 2025, has led to over 730,000 ETH held by public companies. This new demand vector mirrors Bitcoin’s 2020 treasury wave and has contributed to ETH’s recent outperformance against BTC.

Not long ago, Bitcoin was widely dismissed as a legitimate store of value—its thesis as “digital gold” seemed outlandish to many. Today, Ethereum (ETH) faces a similar identity crisis. Frequently misunderstood, ETH has underperformed in annual returns, missed key meme cycles, and experienced slowed retail adoption across much of the crypto ecosystem.

A common criticism is that ETH lacks clear mechanisms for value accrual. Skeptics argue that the rise of Layer 2 solutions cannibalizes base layer fees, weakening ETH’s role as a monetary asset. When ETH is viewed primarily through the lens of transaction fees, protocol revenue, or “real economic value,” it begins to resemble a cloud computing security—more akin to Amazon stock than a sovereign digital money.

In my view, this framing constitutes a category error. Evaluating ETH purely through the lens of cash flows or protocol fees conflates fundamentally different asset classes. Instead, it is better understood through a commodity-like framework, more akin to Bitcoin. More precisely, ETH constitutes a distinct asset class: a scarce yet productive, programmable reserve asset whose value accrues through its role in securing, settling, and powering an increasingly institutionalized, composable onchain economy.

Fiat Debasement: Why the World Needs Alternatives

To fully appreciate ETH's evolving monetary role, it's essential to contextualize it within the broader economic environment, especially in an era marked by fiat debasement and monetary expansion. Driven by persistent government stimulus and spending, inflation is often understated. Although official CPI figures suggest inflation hovers around 2% annually, this metric is subject to revision and may obscure the real erosion of purchasing power.

Between 1998 and 2024, CPI inflation averaged 2.53% per year. In contrast, the U.S. M2 money supply expanded at 6.36% annually, outpacing inflation, home prices, and approaching the S&P 500’s 8.18% return. This even suggests that much of the equity market’s nominal growth may stem more from monetary expansion than productivity gains.

The rapid increase in money supply reflects growing government reliance on monetary stimulus and fiscal spending programs to manage economic instability. Recent legislation such as Trump’s “Big Beautiful Bill” (BBB) has introduced aggressive new spending measures that are widely viewed as inflationary. Meanwhile, the rollout of the Department of Government Efficiency (DOGE), heavily championed by Elon Musk, appears to have underdelivered. These developments have contributed to a growing consensus that existing monetary systems are inadequate and that a more reliable store-of-value asset or form of money is urgently needed.

What Makes a Store of Value—and Where ETH Fits

A credible store of value typically satisfies four criteria:

Durability – It must withstand the test of time without degradation.

Value Preservation – It should preserve purchasing power across market cycles.

Liquidity – It must be easily tradable in active markets.

Adoption and Trust – It must be broadly trusted or adopted.

Today, ETH excels in durability and liquidity. Its durability stems from Ethereum’s decentralized and secure network. Liquidity is also high: ETH is the second-most traded crypto asset, with deep markets on both centralized and decentralized exchanges.

However, value preservation, adoption, and trust remain debatable criteria when evaluating ETH through a purely traditional "store of value" lens. This is precisely where the concept of a "scarce programmable reserve asset" becomes more fitting, highlighting ETH's active role and unique mechanisms for value maintenance and trust-building.

ETH's Monetary Policy: Scarce Yet Adaptive

One of the most debated aspects of ETH’s role as a store of value is its monetary policy, particularly its approach to supply and inflation. Critics often point to Ethereum’s lack of a fixed supply cap. However, this critique overlooks the architectural sophistication of Ethereum’s adaptive issuance model.

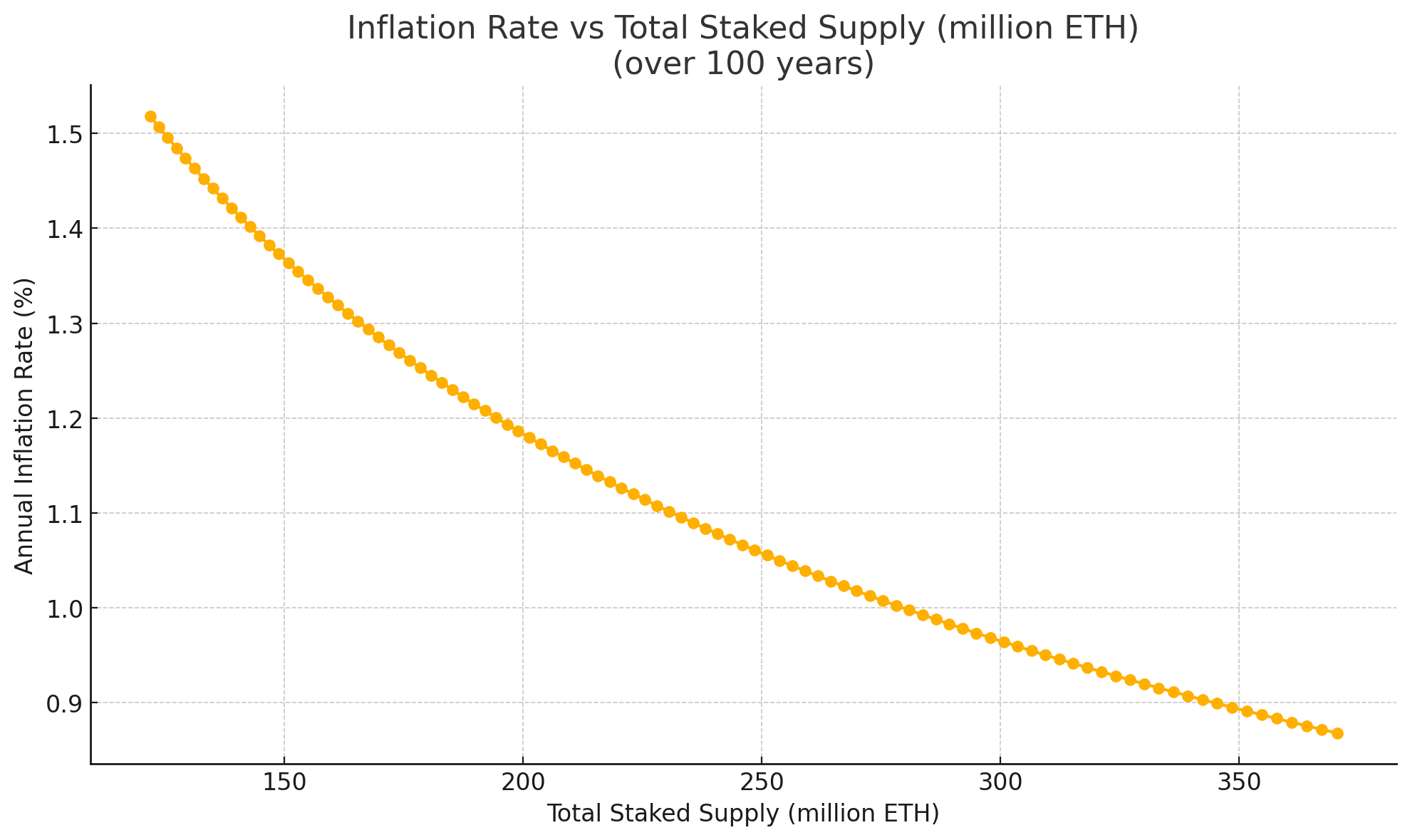

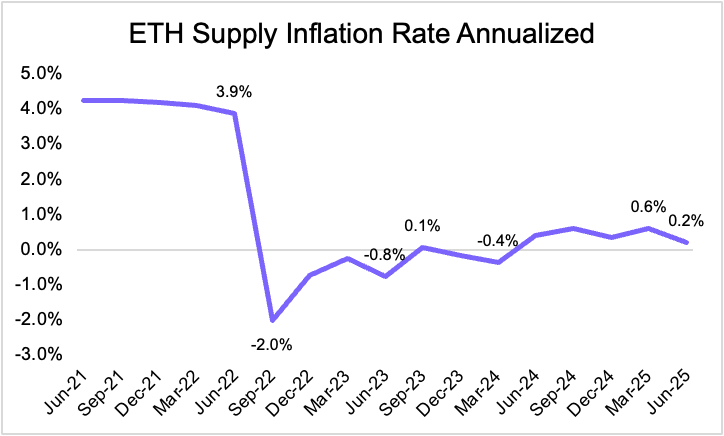

ETH issuance is dynamically linked to the amount of ETH staked. While issuance does rise as staking participation increases, the relationship is sublinear: the inflation rate grows more slowly than the total amount staked. This is because issuance is inversely proportional to the square root of total ETH staked, creating a natural moderatin effect on inflation.

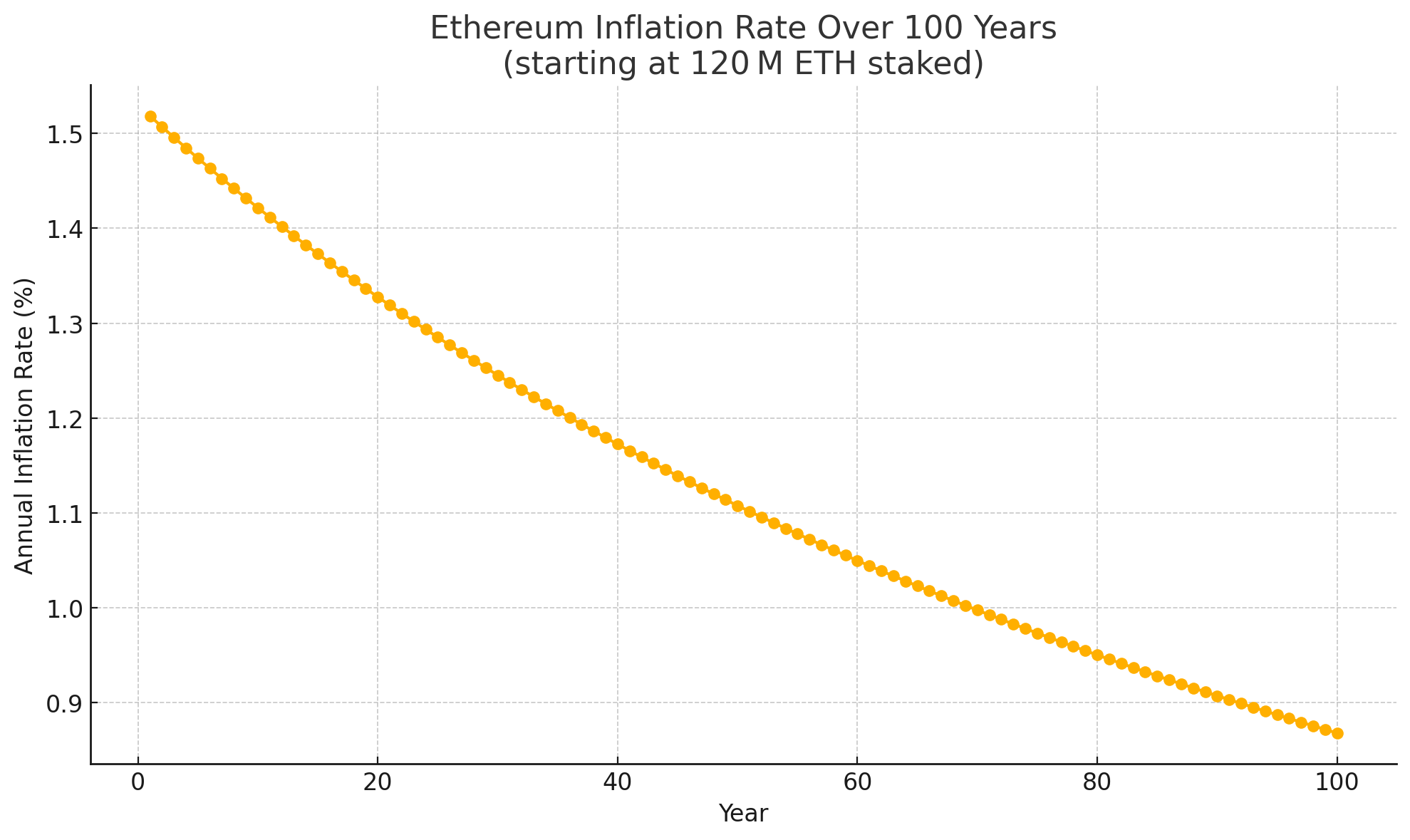

This mechanism introduces a soft ceiling on inflation that declines gradually over time, even as staking participation increases. In a modeled worst-case scenario—where 100% of ETH is staked—annual inflation is capped at approximately 1.52%.

Importantly, even this worst-case issuance rate declines over time as the total ETH supply increases, following an exponential decay curve. Assuming 100% staking and no ETH burn, projected inflation would trend as follows:

Year 1(2025): ~1.52%

Year 20(2045): ~1.33%

Year 50(2075): ~1.13%

Year 100(2125): ~0.89%

Even under these conservative assumptions, Ethereum’s declining inflation curve reflects a built-in form of monetary discipline—bolstering its credibility as a long-term store of value.The picture improves further when factoring in Ethereum’s burn mechanism, introduced via EIP-1559. A portion of transaction fees is permanently removed from circulation, meaning net inflation can fall significantly below gross issuance—and at times even become deflationary. In practice, since Ethereum’s transition from proof-of-work to proof-of-stake, net inflation has consistently remained below issuance and has periodically dipped into negative territory.

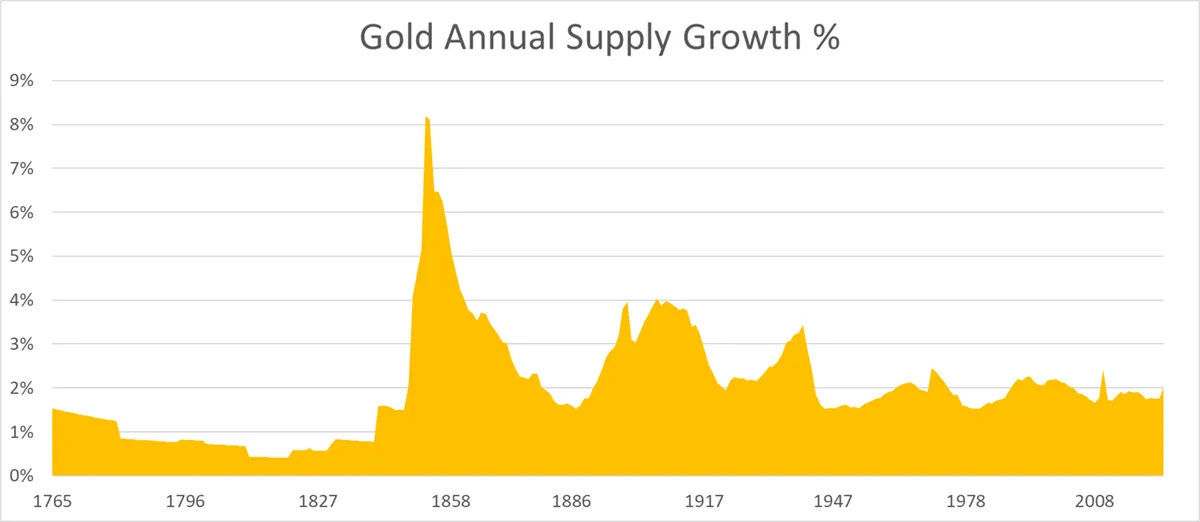

In contrast to fiat currencies like the U.S. dollar—whose M2 money supply has grown at an average rate exceeding 6% annually—Ethereum’s structurally constrained (and potentially deflationary) supply profile strengthens its appeal as a value asset. Notably, Ethereum’s maximum supply growth now rivals—or even falls below—that of gold, further reinforcing its position as a sound monetary asset.

Institutional Adoption and Trust

While Ethereum’s monetary design effectively addresses supply dynamics, its real-world utility as a settlement layer is now a primary driver of adoption and institutional trust. Major financial institutions are building directly on Ethereum: Robinhood is developing a tokenized equity platform, JPMorgan is launching its deposit token (JPMD) on Base—an Ethereum Layer 2—and BlackRock is tokenizing a money market fund on the network with BUIDL.

This onchain process is driven by strong value propositions that solve legacy inefficiencies and unlock new opportunities:

Efficiency and Cost Reduction: Traditional finance relies on intermediaries, manual steps, and slow settlements. Blockchain streamlines these with automation and smart contracts, cutting costs, errors, and processing times—from days to seconds.

Liquidity and Fractional Ownership: Tokenization enables fractional ownership of illiquid assets like real estate or art, widening investor access and freeing up locked capital.

Transparency and Compliance: Blockchain’s immutable ledger ensures a verifiable audit trail, simplifying compliance and reducing fraud through real-time visibility into transactions and asset ownership.

Innovation and Market Access: Composable on-chain assets allow for new products—like automated lending or synthetic assets—creating fresh revenue streams and expanding financial reach beyond legacy systems.

ETH Staking as Security and Economic Alignment

This on-chain migration of traditional financial assets underscores two primary drivers of ETH demand. First, the growing presence of real-world assets (RWAs) and stablecoins increases on-chain activity, driving up demand for ETH as a gas token. More importantly, as Tom Lee observes, institutions may need to acquire and stake ETH to help secure the infrastructure they depend on, thereby aligning their interests with Ethereum’s long-term security. In this context, stablecoins represent Ethereum’s “ChatGPT moment,” a major breakthrough use case that demonstrates the platform’s transformative potential and broad utility.

As more value is settled on-chain, the alignment between Ethereum’s security and its economic value becomes increasingly important. Ethereum’s finality mechanism, Casper FFG, ensures that blocks are finalized only when a supermajority—two-thirds or more—of staked ETH reaches consensus. While an attacker controlling at least one-third of staked ETH wouldn’t be able to finalize malicious blocks, they could disrupt finality altogether by breaking consensus. In such scenarios, Ethereum would still propose and process blocks, but without finality, those transactions could be reversed or reordered, introducing serious settlement risk for institutional use cases.

Even when operating on Layer 2s, which depend on Ethereum for final settlement, institutional actors rely on the base layer’s security. Far from undermining ETH, Layer 2s enhance its value by driving demand for base-layer security and gas. They submit proofs to Ethereum, pay base fees, and often use ETH as their native gas token. As execution scales on rollups, Ethereum accrues value through its foundational role in providing secure settlement.

In the long term, many institutions are likely to move beyond passive staking via custodians and begin operating their own validators. While third-party staking solutions offer convenience, running validators allows institutions greater control, improved security, and direct participation in consensus. This is particularly valuable for stablecoin and RWA issuers, as it enables them to capture MEV, ensure reliable transaction inclusion, and leverage private execution—capabilities crucial to maintaining operational reliability and transactional integrity.

Importantly, broader institutional involvement in validator operations can help address one of Ethereum’s current challenges: the concentration of stake among a few large operators, such as liquid staking protocols and centralized exchanges. By diversifying the validator set, institutional participation contributes to Ethereum’s decentralization, enhances its resilience, and strengthens the trustworthiness of the network as a global settlement layer.

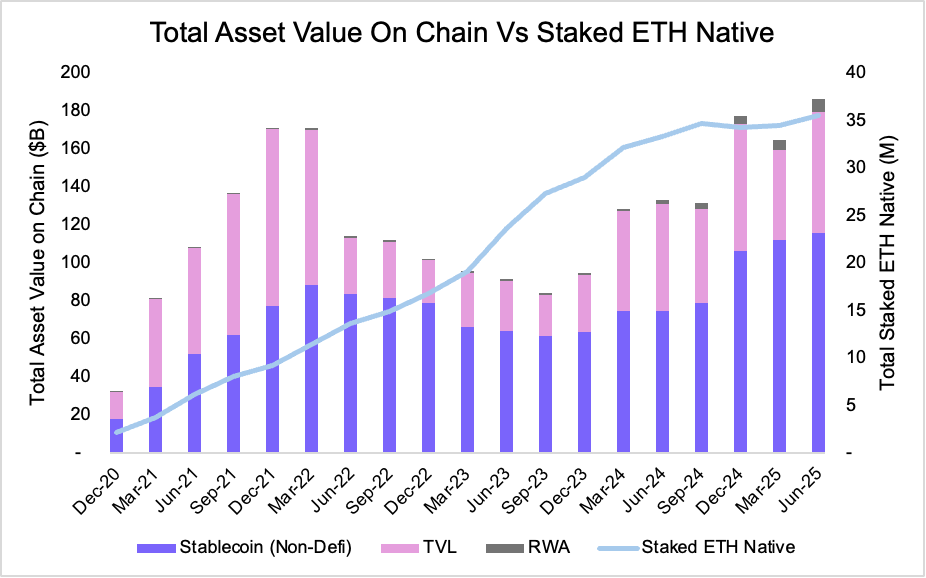

A compelling trend from 2020 to 2025 reinforces this incentive alignment: the growth of on-chain assets has closely tracked the rise in staked ETH. As of June 2025, the total supply of stablecoins on Ethereum reached a record $116.06 billion, while tokenized real-world assets (RWAs) climbed to $6.89 billion. In parallel, staked ETH grew to 35.53 million ETH, a significant increase that highlights how network participants scale security alongside on-chain value.

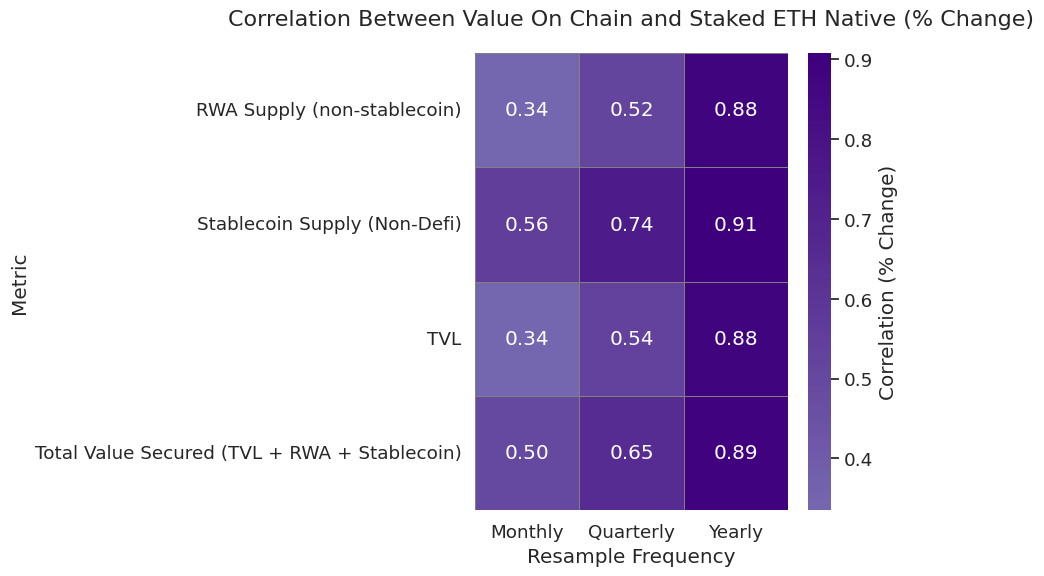

Quantitatively, the correlation between on-chain asset growth and native ETH staking has remained above 88% annually across major asset classes. Stablecoin supply, in particular, closely tracks staked eth growth. While quarterly correlations exhibit more variability due to short-term fluctuations, the broader trend holds—as assets move on-chain, the incentive to stake ETH increases.

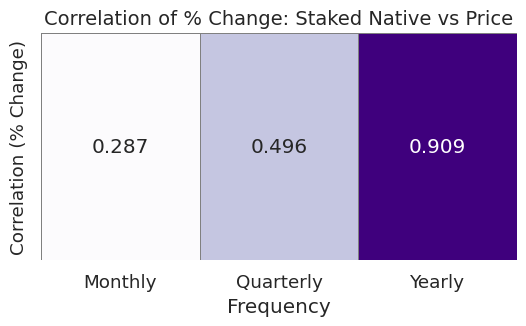

Further, this increase in staking also contributes to ETH’s price dynamics. As more ETH is staked and removed from liquid circulation, ETH supply tightens, particularly during periods of heightened on-chain demand. Our analysis shows a 90.9% correlation between staked ETH and ETH price at yearly frequency, and a 49.6% correlation on a quarterly basis, supporting the view that staking not only secures the network but also creates favorable supply/demand pressure on ETH itself in the long run.

A recent policy clarification from the SEC has eased regulatory uncertainty around Ethereum staking. On May 29, 2025, the SEC’s Division of Corporation Finance stated that certain protocol staking activities—when limited to non-entrepreneurial roles like self-staking, delegated staking, or custodial staking under specific conditions—do not constitute securities offerings. While more complex arrangements remain fact-dependent, this clarification has encouraged institutions to participate more actively. Following the announcement, Ethereum ETF filings began including staking provisions, allowing funds to earn rewards while contributing to network security. This not only enhances return profiles, but further anchors institutional adoption and trust with Ethereum’s long-term adoption.

Composability and ETH as a Productive Asset

Another defining characteristic that sets ETH apart from pure store of value asset like gold and Bitcoin is its composability, which itself drives demand for ETH. While gold and BTC are non-productive asset, ETH is natively programmable. It plays an active role in the Ethereum ecosystem, powering decentralized finance (DeFi), stablecoins, and Layer 2 networks.

Composability refers to the ability of protocols and assets to interoperate seamlessly. In Ethereum, this makes ETH not only a monetary asset but also a foundational building block for on-chain applications. As more protocols are built around and on top of ETH, the demand for ETH increases—not just as gas, but as collateral, liquidity, and staking capital.

Today, ETH is used in a variety of critical functions:

Staking & Restaking – ETH secures Ethereum itself and can be restaked to provide security to oracles, rollups, and middleware via EigenLayer.

Collateral in Lending & Stablecoins – ETH backs major lending protocols like Aave and Maker, and is foundational to overcollateralized stablecoins.

Liquidity in AMMs – ETH pairs dominate decentralized exchanges like Uniswap and Curve, enabling efficient swaps across the entire ecosystem.

Gas Across Chains – ETH is the native gas token for most Layer 2s, including Optimism, Arbitrum, Base, zkSync, and Scroll.

Interoperability – ETH is bridged, wrapped, and used in non-EVM chains such as Solana, Cosmos (via Axelar), and others—making it one of the most widely transferrable assets on-chain.

This deep, integrated utility makes ETH a scarce but productive reserve asset. As ETH becomes more embedded in the ecosystem, switching costs rise and network effects strengthen. In some sense, ETH is arguably more comparable to gold than Bitcoin. Much of gold’s value comes from industrial and jewelry applications—not just investment. Bitcoin, by contrast, lacks this kind of functional utility.

Ethereum vs. Solana: The Layer-1 Divergence

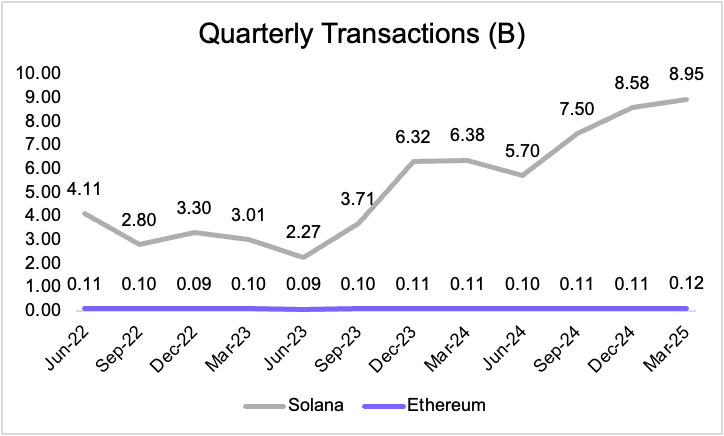

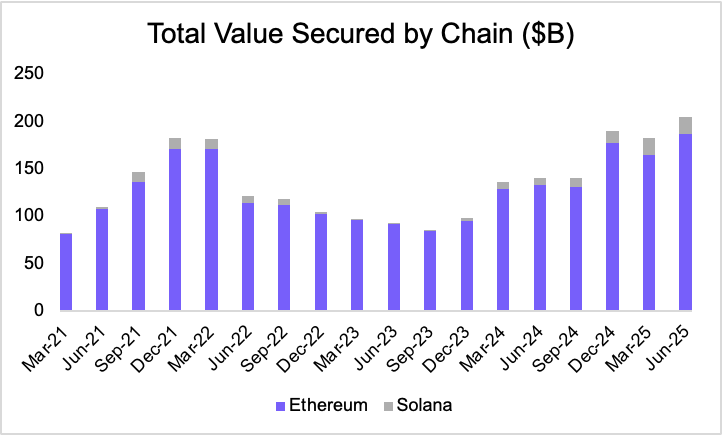

During this cycle, Solana appears to be the biggest winner in the Layer 1 space. It has effectively captured the meme coin ecosystem, creating a vibrant network for new tokens to launch and gain traction. While this momentum is real, Solana remains less decentralized than Ethereum due to its limited validator set and high hardware requirements for participation.

That said, demand for Layer 1 blockspace will likely become stratified. In this layered future, both Solana and Ethereum can thrive. Different assets will require different trade-offs between speed, efficiency, and security. Over the long term, however, Ethereum—due to its stronger decentralization and security guarantees—is likely to capture a larger share of asset value, while Solana may capture more transactional frequency.

However, in the financial markets, the market for assets seeking robust security is magnitudes larger than that for those prioritizing execution speed alone. This dynamic favors Ethereum: as more high-value assets move on-chain, Ethereum’s role as the foundational settlement layer becomes increasingly valuable.

Treasury Momentum: ETH’s MicroStrategy Moment

While on-chain assets and institutional demand are long-term structural drivers for ETH, Ethereum treasury plays—much like how MicroStrategy (MSTR) has leveraged Bitcoin—could become a sustained catalyst for ETH as an asset. A key turning point in this trend was Sharplink Gaming ($SBET) announcing its Ethereum treasury strategy at the end of May, led by Ethereum co-founder Joseph Lubin.

Treasury plays serve as vehicles for tokens to access traditional finance (TradFi) liquidity while simultaneously increasing the asset value per share for the companies involved. Since the emergence of Ethereum-based treasury strategies, these treasury companies have accumulated over 730,000 ETH, and ETH has begun to outperform Bitcoin—an uncommon occurrence in this cycle. We believe this marks the beginning of a broader trend in Ethereum-focused treasury adoption.

Stay tuned for our upcoming research report, which will dive deeper into the evolving landscape of Ethereum treasury adoption!

Conclusion: ETH Is the Reserve Asset of the Onchain Economy

Ethereum’s evolution embodies a broader paradigm shift in the conceptualization of monetary assets within a digital economy. Much like how Bitcoin overcame early skepticism to earn recognition as “digital gold,” Ether (ETH) is establishing its distinct identity—not by emulating Bitcoin’s narrative, but by maturing into a more versatile and foundational asset. ETH is not simply analogous to a cloud computing security, nor is it limited to serving as a utility token for transaction fees or a source of protocol revenue. Rather, it represents a scarce, programmable, and economically essential reserve asset—one that underpins the security, settlement, and functionality of a progressively institutionalized on-chain financial ecosystem.