Artemis Weekly Digital Finance Fundamentals 2026.3.27

This week, we look at Tempo's main net launch, a 72B parameter model trained on a Tao subnet and CRCL's 22% drawdown

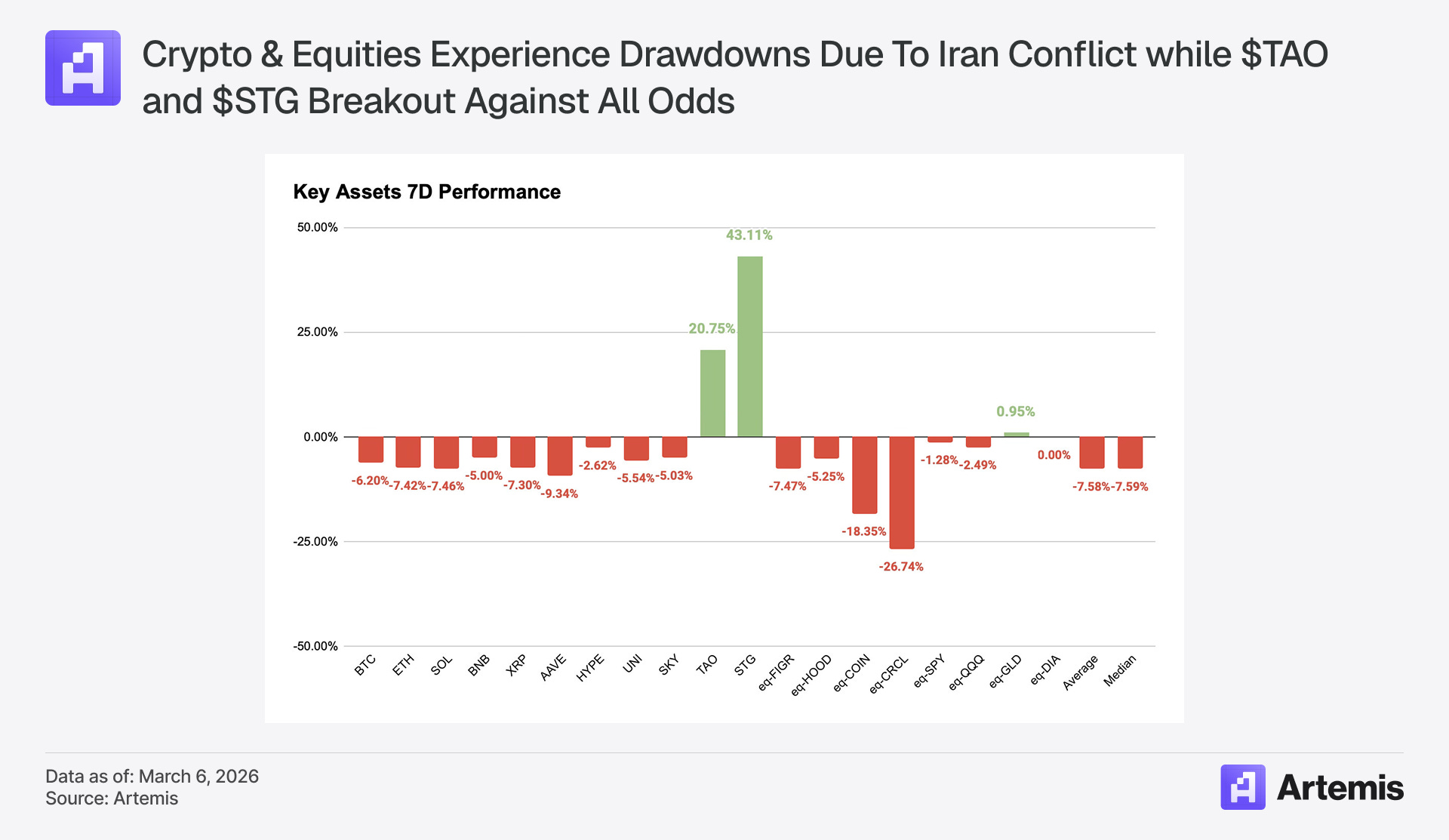

Market Overview: The Weekly Recap

Welcome back to Artemis’ Weekly Digital Finance Fundamentals!

Risk-off across the board this week. The S&P 500 dropped −1.7%, the Nasdaq fell −2.4%, and the 2-year Treasury yield climbed to 4.02% as the Fed dot plot shifted to zero cuts for 2026. Oil & Gas remains the YTD leader at +40%, though commodities cooled – gold at ~$4,430, silver at ~$68 (down 44% from its January ATH). In private markets, Kalshi raised $1B at a $22B valuation (Coatue) and Mastercard acquired BVNK for $1.8B.

Crypto followed equities lower. Bitcoin fell −5.8% to ~$66,500, Ethereum −7.5% to ~$1,987, Solana −7.5% to ~$83. AAVE (−9.2%) and MNT (−10.6%) were the hardest hit, while HYPE (−2.9%) held up relatively better. The clear standouts: TAO surged +19.7% on a decentralized AI training milestone and a Jensen Huang endorsement, and STG spiked +46.7% in what appears to be a technically-driven move rather than the fundamentals.

Today We Highlight:

Tempo Mainnet Launch & the Machine Payments Protocol (MPP)

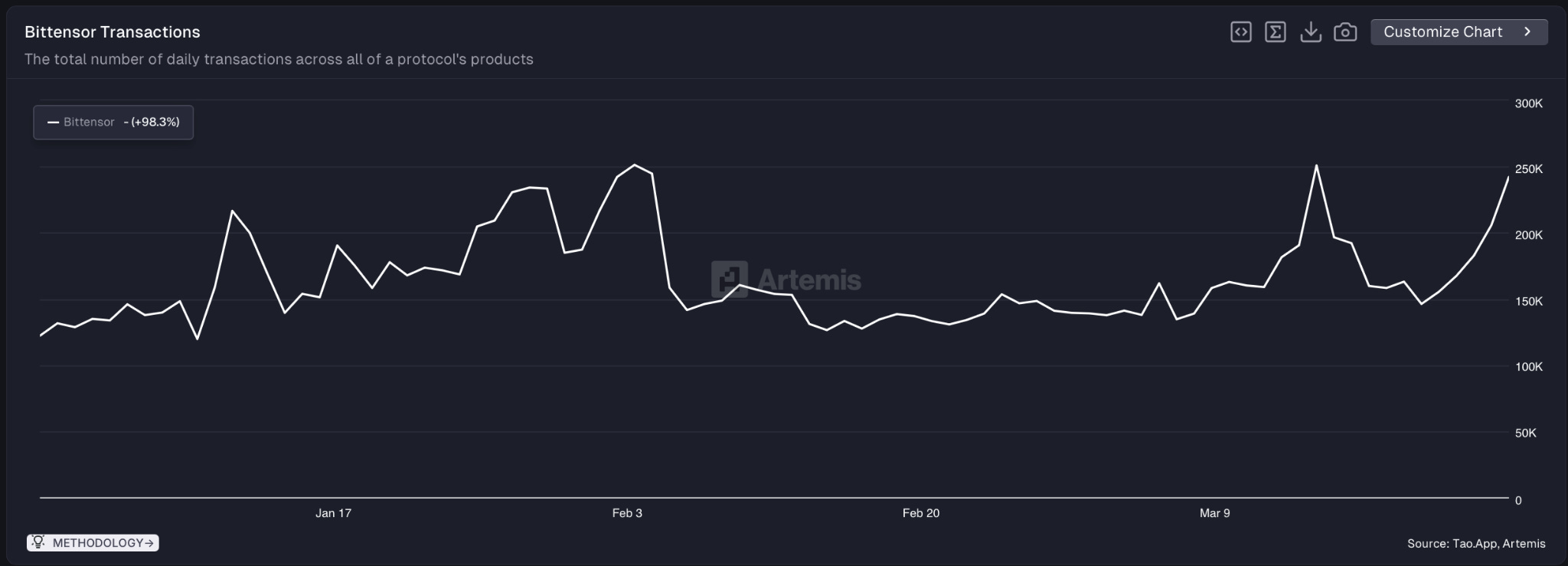

Bittensor (TAO): Covenant-72B and the Decentralized AI Training Milestone

Circle (CRCL) Crashes 22% Potentially Due To Changes In The Clarity Act

1. Tempo Mainnet Launch & the Machine Payments Protocol (MPP)

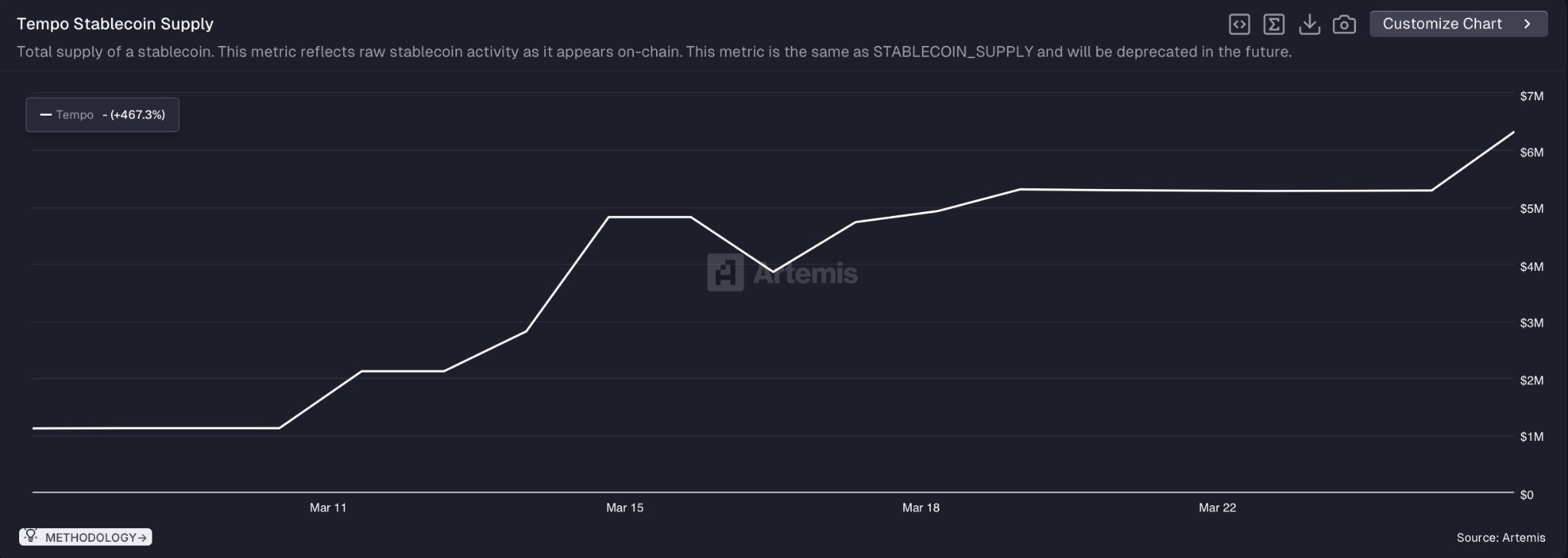

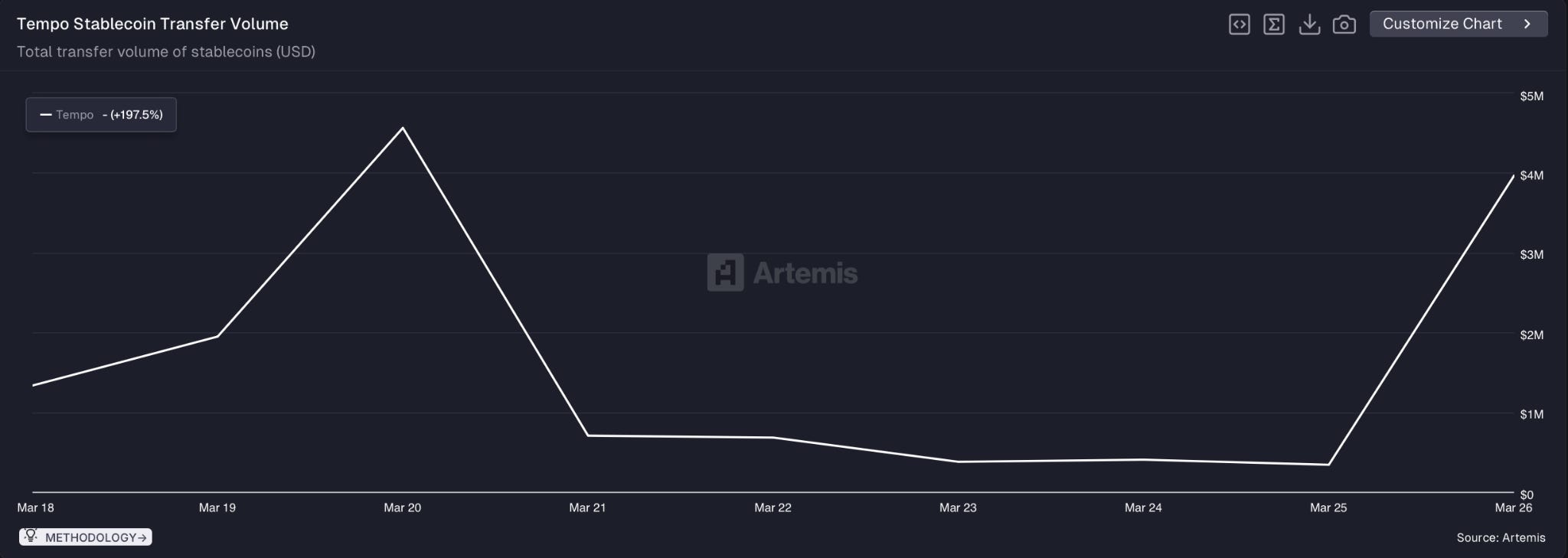

On March 18, Tempo – the payments-focused Layer 1 incubated by Stripe and Paradigm – launched its mainnet. In its first 8 days, stablecoin supply grew from zero to $6.3 million, with $14.3 million in cumulative transfer volume.

For comparison, other recent chain launches attracted significantly more stablecoin capital in their first week: Monad $242M (Nov 2025), Base $75M (Aug 2023), MegaETH ~$36M (Feb 2026). Those chains also saw much higher turnover—Monad at ~18.5x velocity and Base at ~15x, driven by DeFi activity and liquidity incentives. Tempo came in at ~2.6x. However, the gap makes sense: Tempo isn’t competing for DeFi TVL. Its flows are payments, not AMM swaps.

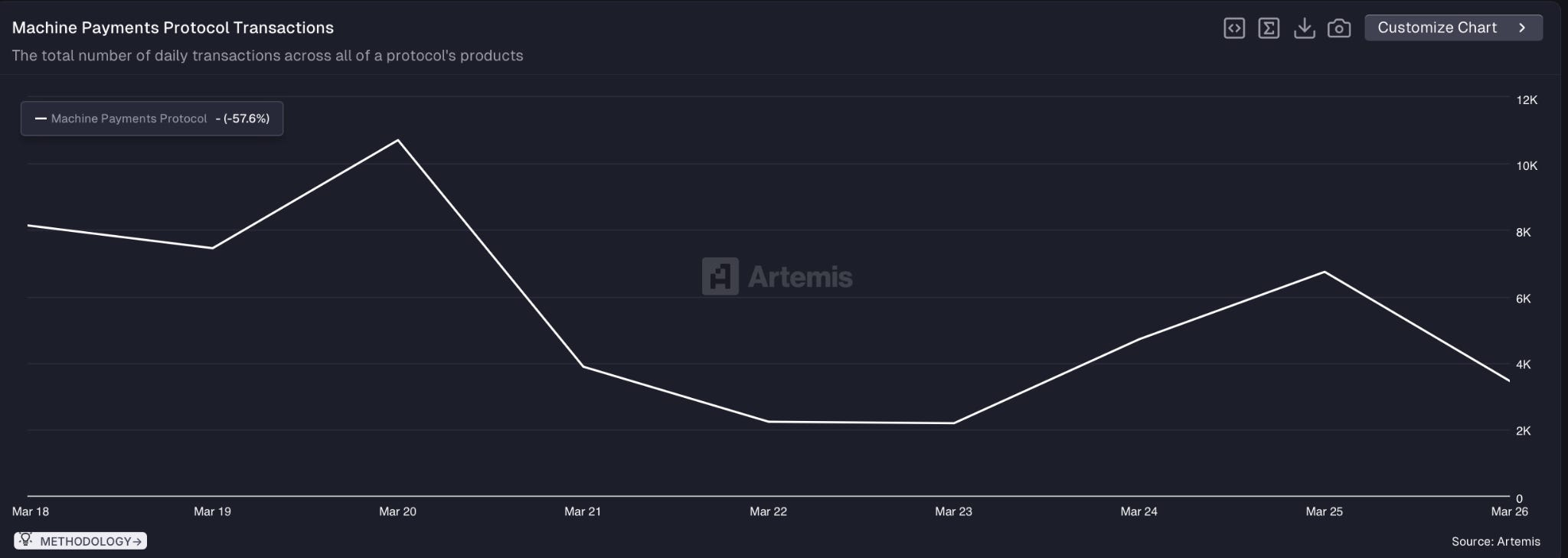

Launching alongside the chain is the Machine Payments Protocol (MPP), which can be thought of as a universal checkout layer for AI agents. When software needs to pay for an API call, a compute job, or a data query, MPP handles the request, authorization, and settlement. 100+ services are integrated at launch, including Alchemy, Dune Analytics, Merit Systems, and Parallel Web Systems.

Early MPP usage: ~49,000 transactions, 1,156 buyers, and 61 sellers (service providers) in 8 days. Dollar volume is tiny (~$7,300) because these are microtransactions by design.

2. Bittensor (TAO): Covenant-72B and the Decentralized AI Training Milestone

Bittensor’s TAO token surged +26% over the past 7 days and +102% over the past month, pushing above $350 with daily volumes exceeding $900 million and vaulting it to the 26th largest cryptocurrency by market cap. The catalyst: Covenant-72B, a 72-billion-parameter large language model fully trained on Bittensor’s decentralized Subnet 3 by over 70 contributors using commodity internet hardware.

Covenant-72B was pre-trained permissionlessly across 70+ global contributors and achieved a 67.1 MMLU score, confirmed in a March 2026 arXiv paper as the largest decentralized LLM pre-training run on record. The result is significant because it demonstrates that meaningful model training can happen across a decentralized network of commodity hardware, rather than requiring centralized data center clusters.

The rally accelerated after Nvidia CEO Jensen Huang responded to investor Chamath Palihapitiya’s description of the breakthrough by calling Bittensor “a modern version of Folding@home.” On the institutional side, Grayscale’s S-1 filing from December 2025 to convert its Bittensor Trust into a spot TAO ETF remains pending and represents a potential catalyst for regulated institutional access.

3. Circle (CRCL) Crashes 22% Potentially Due To Changes In The Clarity Act

Circle’s stock fell −22% on the week ($126 → $98), with the bulk of the damage coming on March 24 when CRCL dropped 20% in a single session—its largest one-day decline since listing in June 2025. Coinbase, Circle’s primary distribution partner, fell 8% on the same day before partially recovering.

The catalyst might’ve been a report that the latest text of the Clarity Act proposal in Congress would prohibit platforms from offering yield “directly or indirectly” for holding a stablecoin in a manner that resembles a bank deposit. That’s a direct threat to Circle’s business model around USDC rewards and to the broader embedded yield thesis—if platforms can’t pass yield through to end users, the competitive dynamics of stablecoin distribution change materially.

ARK Invest's Lorenzo Valente pushed back: the Clarity Act doesn't ban Circle from paying distributors like Coinbase — it bans retail passthrough of yield. Circle pays Coinbase over $900M/year in revenue share, roughly half of Circle's total revenue. That relationship is untouched. The bull case: if Coinbase can no longer share yield with users but still collects it from Circle, distributor margins on USDC improve — strengthening their incentive to grow supply. The bear case: without yield as a user acquisition tool, platforms lose a key reason retail holds USDC over alternatives. ARK bought $16 million of CRCL on the dip.

Adding to the policy uncertainty: David Sacks’ 130-day term as Trump’s “crypto czar” officially ended on March 26. Sacks is transitioning to co-chair the President’s Council of Advisors on Science and Technology (PCAST) alongside Michael Kratsios, a role that covers a broader technology mandate but moves him meaningfully further from the direct policy influence he held as the administration’s point person on crypto and AI.

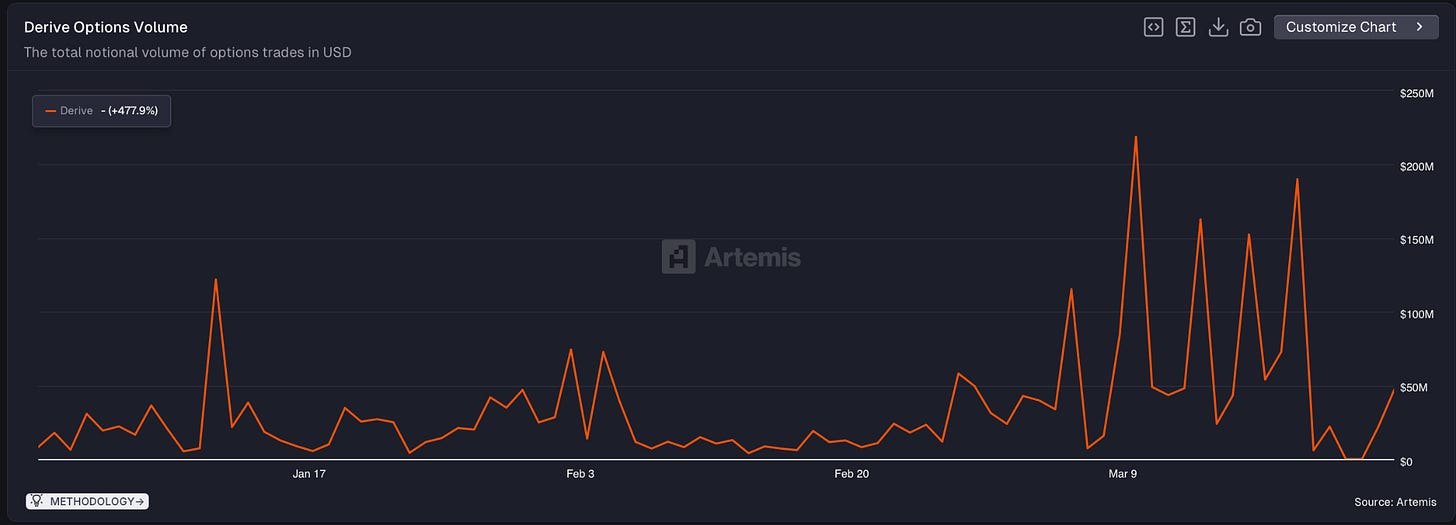

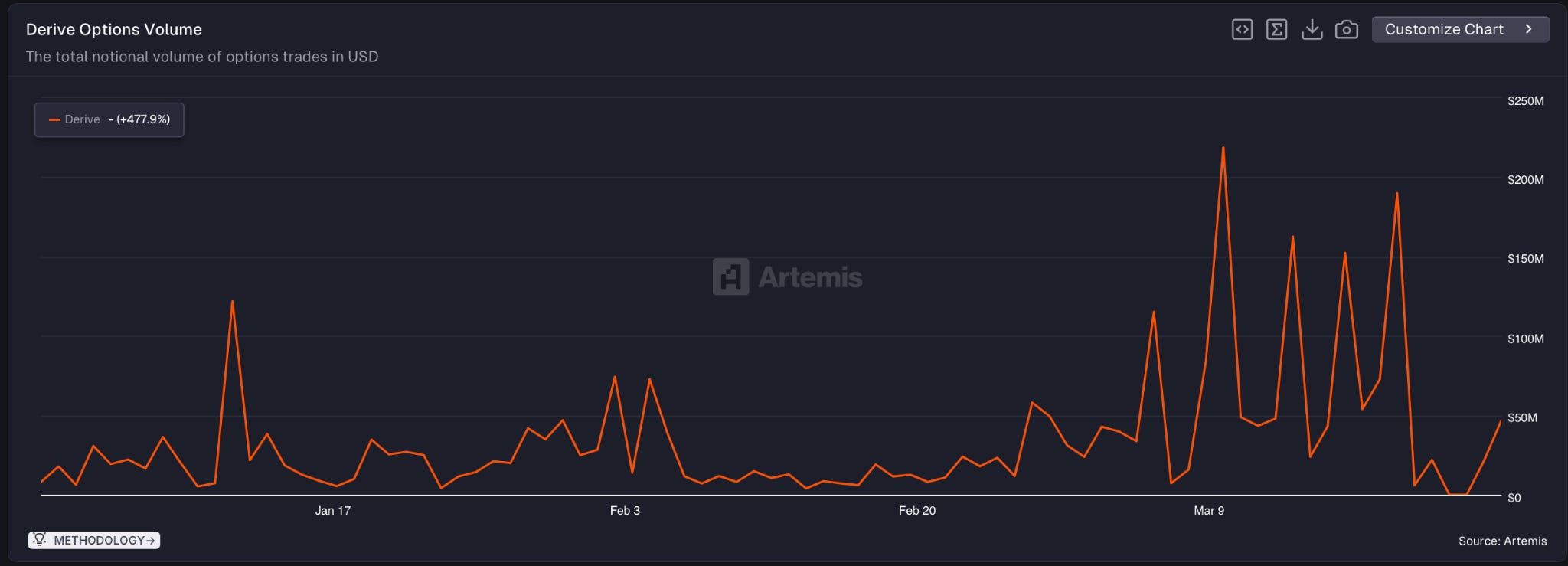

Charts of the Week

Rapid-fire visual data points.

Onchain options volume showed signs of scaling. DeriveXYZ surpassed $600 million in weekly volume for the first time last week, approaching the $1 billion mark. The inflection suggests structured products and volatility markets are beginning to find product-market fit onchain.

Other Notable News

Mantle became the fastest chain to reach $1 billion in Aave deposits (18 days), compared to Polygon (24 days) and Ethereum (58 days, excluding early plasma/Avalanche deployments). Last week, Mantle’s Aave deployment ranked as the 3rd largest by deposits, overtaking Arbitrum and Base. Contributing factors include Mantle Vault yield on Bybit, a large treasury, and Tether’s tokenized gold/USDT0 integration.

Thanks for reading! Stay ahead this week by using the Artemis Terminal or pulling live data with =ART() in Excel.

Disclaimer: The authors of this content, as well as affiliates of Artemis Analytics, may have financial interests in the protocols or tokens mentioned. This does not constitute investment advice or a recommendation to buy, sell, or hold any asset. The information provided is for educational purposes only and should not be relied upon for financial, legal, or tax decisions. Readers should assess their own circumstances before making any financial choices. Views expressed may change without notice, and Artemis Analytics is not liable for any losses resulting from the use of this content.