Artemis Weekly Digital Finance Fundamentals 2026.4.11

This week: the Iran ceasefire rally, Morgan Stanley's MSBT launch, Strategy at 767K BTC, and the CLARITY Act Senate countdown.

Market Overview: The Weekly Recap

Geopolitics dominated again — but this week it broke the other way. After five weeks of war-driven compression, Tuesday night’s (April 7, 2026) Trump-Iran ceasefire announcement triggered one of the sharpest single-day risk reversals in recent memory. The Dow surged 1,325 points (+2.85%) on Wednesday, its best day since April 2025. The S&P 500 jumped 2.51% to 6,782, breaching its 200-day moving average for the first time since the conflict began. WTI crude collapsed 16.4% to $94.41 — its biggest daily drop since April 2020 — as Iran confirmed it would allow passage through the Strait of Hormuz for the two-week truce period. The deal is fragile: Iran’s parliament speaker briefly claimed a US violation Wednesday afternoon, and JPMorgan cautioned that “a two-week pause is not a resolution.” The clock expires April 22.

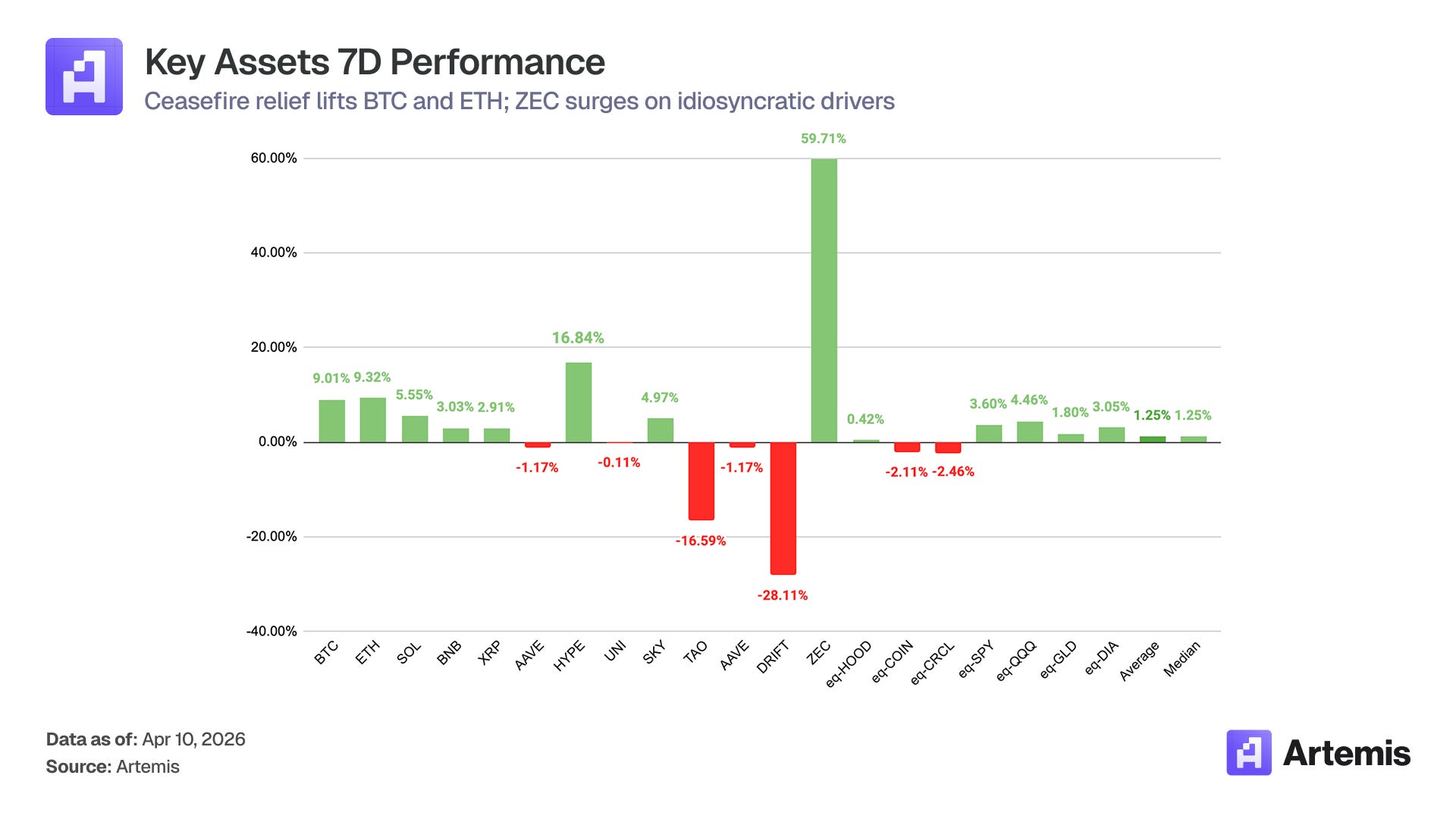

Crypto finally caught a bid. BTC surged from ~$68K to ~$72.7K on the ceasefire news, finishing the week up ~9% and triggering nearly $600M in leveraged liquidations — over $400M from shorts that had piled in during weeks of range-bound drift. ETH gained ~9.3% on the week. The standout was ZEC, up a striking +59.7%, though on idiosyncratic rather than macro drivers. HYPE continued its strong run, up +16.8%, while SKY gained +4.97%. On the losing side, DRIFT extended its post-exploit collapse, down another -28.1% on the week following the $285M April 1 hack, and TAO gave back -16.59% after its recent surge. Equities proxies tracked closely with the relief rally: eq-COIN +3.6%, eq-QQQ +4.46%, while eq-HOOD (-2.11%) and eq-CRCL (-2.46%) lagged on continued CLARITY Act yield-ban uncertainty.

The week’s average across tracked assets came in at +1.25%, median +1.25% — a modest but real improvement from the prior four weeks.

Today We Highlight:

Morgan Stanley MSBT — the first US bank spot Bitcoin ETF

CLARITY Act: Senate returns April 13 — the next major catalyst

Corporate Bitcoin buying: Strategy crosses 767K BTC as DAT total nears 900K

Artemis Analyst Sector Deep-Dives: Agentic Payments, Lending, Trading, Neobanks, and Prediction Markets

1. Morgan Stanley MSBT: the first US bank spot Bitcoin ETF

On April 8, Morgan Stanley launched the Morgan Stanley Bitcoin Trust (MSBT) on NYSE Arca, becoming the first major US bank to issue its own spot Bitcoin ETF. The fund drew ~$34M in net inflows on day one. Bloomberg ETF analyst Eric Balchunas placed the debut in the top 1% of all ETF launches and projects $5B AUM in year one.

Why does the fee matter?

MSBT launches at 0.14% — 11 basis points below BlackRock's IBIT at 0.25%. On a $100K investment that's $110/year in savings. Narrow in absolute terms, but it sets a new floor. Fee compression in Bitcoin ETFs is accelerating, and Morgan Stanley just fired the loudest shot yet.

Why is Morgan Stanley's distribution so powerful?

Morgan Stanley's 16,000 wealth advisors oversee $9.3 trillion in client assets. Previously they could recommend third-party Bitcoin ETFs; now they can recommend one that keeps the fee in-house. That internal incentive shift is structural — and it means new long-duration capital gets directed to MSBT rather than existing funds. The first week of flows will be the real tell.

Is MSBT a standalone product or something bigger?

It's the wedge. Morgan Stanley filed for Ethereum and Solana trusts in January, applied to the OCC for a National Trust Bank Charter in February covering custody and staking, and plans to launch retail spot crypto trading on E*Trade in H1 2026. The pattern is clear: Morgan Stanley is building a full-stack digital asset business under its own brand. MSBT is how they get distribution.

Custody: Coinbase (cold storage).

Cash custody and administration: BNY Mellon.

Authorized participants: Jane Street, Virtu Americas, Macquarie Capital.

Benchmark: CoinDesk Bitcoin Benchmark 4PM NY Settlement Rate.

What this means for the Bitcoin ETF landscape?

IBIT remains structurally protected by its liquidity depth and options ecosystem, most active traders won't leave for 11bps. But the long-duration capital flowing through wirehouse advisors is a different market entirely. The landscape is bifurcating: IBIT for traders, MSBT for allocators.

2. CLARITY Act: Senate returns April 13 — what to watch

The Senate returns from Easter recess on April 13 with the CLARITY Act heading for Senate Banking Committee markup in the final weeks of April. This is the most consequential near-term regulatory catalyst for crypto — and the one most likely to move individual names.

What's actually been agreed?

The yield language is "99% resolved" per Senators Tillis and Alsobrooks: passive yield banned, activity-based rewards permitted. That same logic is now baked into the FDIC's GENIUS Act proposed rule — the two regulatory tracks are moving in deliberate lockstep.

What's still unresolved?

Two things.

First, DeFi scope — the “digital asset service providers” language leaves it ambiguous whether protocols like Aave or Morpho are in scope, and that ambiguity alone is a headwind for the sector.

Second, token classification provisions that determine the SEC vs. CFTC jurisdictional split. XRP has been the primary beneficiary of optimism on this front.

On the winners side: Coinbase benefits most clearly, as the yield ban improves USDC distributor margins while its OCC trust charter positions it as the institutional plumbing layer the new framework requires. Circle's $900M+/year revenue share from Coinbase is untouched, though the retail yield acquisition story weakens. Tether is largely unaffected — its model already aligns with the framework.

Why does the timing matter now?

Market participants have been treating CLARITY as a second-half 2026 story. With the Senate back April 13, final-week markup sessions in April are now realistic. That timeline repricing alone could move names.

3. Corporate Bitcoin buying: Strategy crosses 767K BTC as DAT total nears 900K

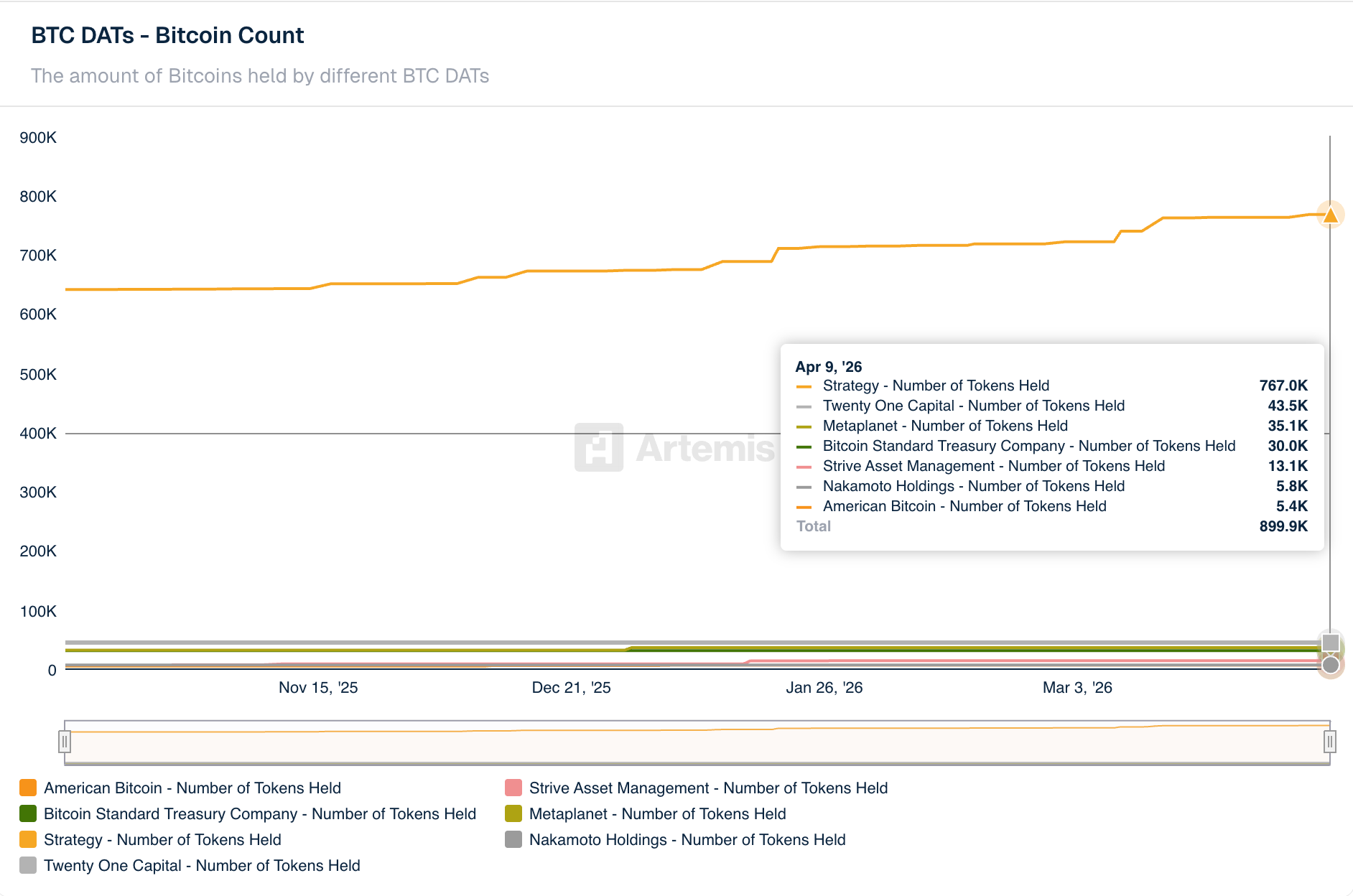

Strategy added another ~4,871 BTC early in the week, pushing its total to 767K BTC as of April 9 — extending its lead as the dominant corporate holder by a wide margin. The broader Digital Asset Treasury (DAT) cohort now collectively holds ~899.9K BTC across seven tracked entities, approaching the psychologically significant 900K mark. That's roughly 4.3% of total Bitcoin supply sitting on corporate balance sheets.

How does Strategy compare to everyone else?

The gap is extraordinary. Twenty One Capital sits at 43.5K, Metaplanet at 35.1K, Bitcoin Standard Treasury Company at 30K, Strive at 13.1K, Nakamoto Holdings at 5.8K, and American Bitcoin at 5.4K. The next six combined don't reach 20% of Strategy's stack.

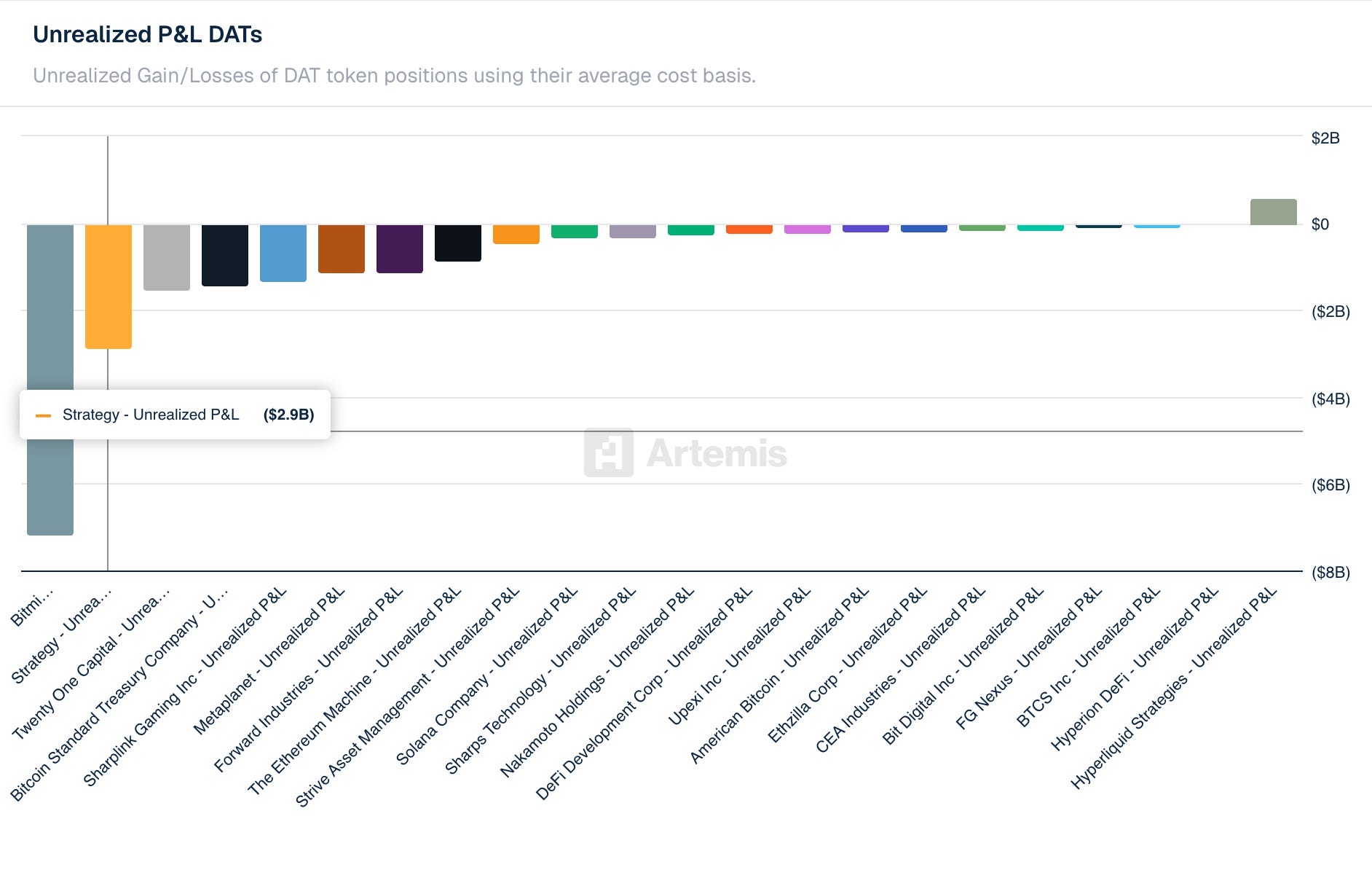

Are these companies actually making money?

Not yet, at current prices. Strategy is sitting on approximately -$2.9B in unrealized losses against its blended cost basis. Most of the DAT cohort accumulated heavily during BTC’s $80K–$100K+ run in late 2025, meaning the majority are currently offside. The ceasefire rally this week provided partial relief, but a sustained break above $80K is what most of these balance sheets need to return to breakeven.

The accumulation continues regardless. Strategy’s behavior through the drawdown reflects the thesis it has always operated on: price is irrelevant at the margin, supply absorption is the objective.

Charts of the Week

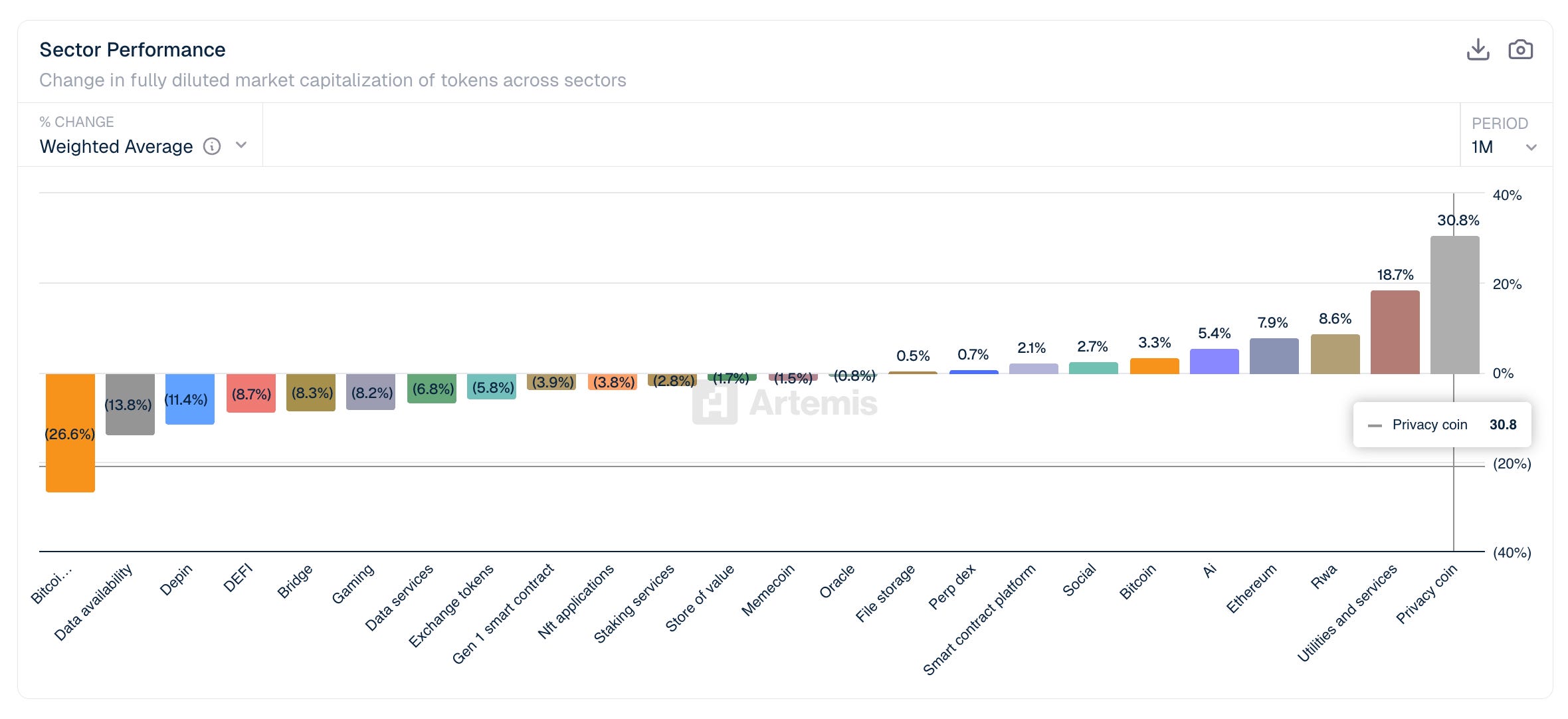

Privacy Coins lead all sectors in performance

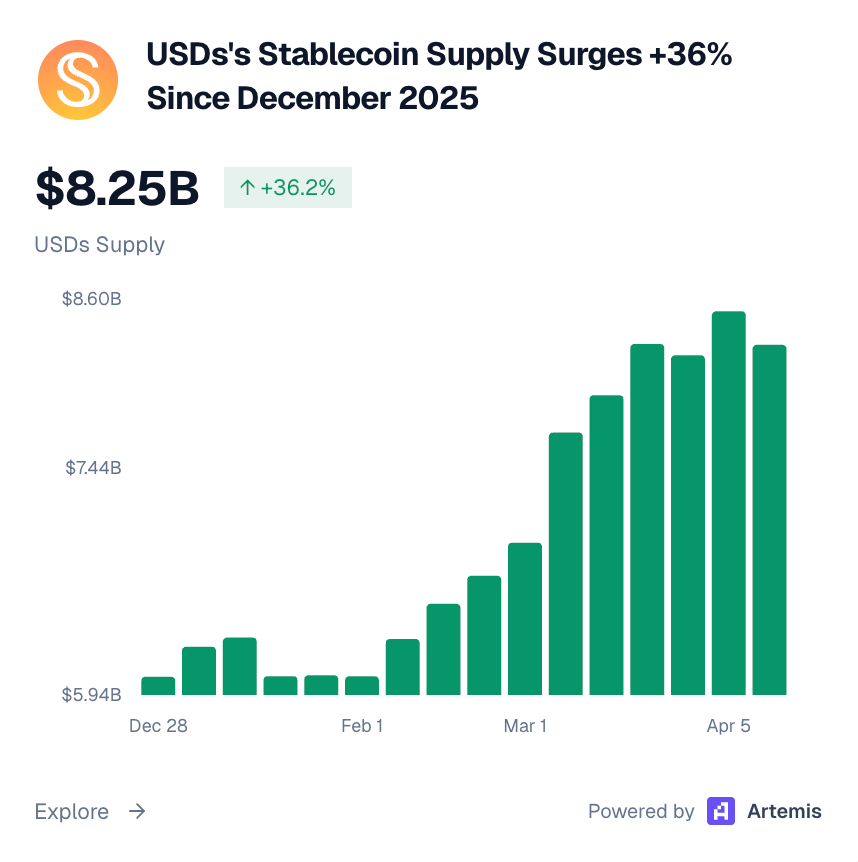

USDs Stablecoin Supply Surges +36% since December 2025

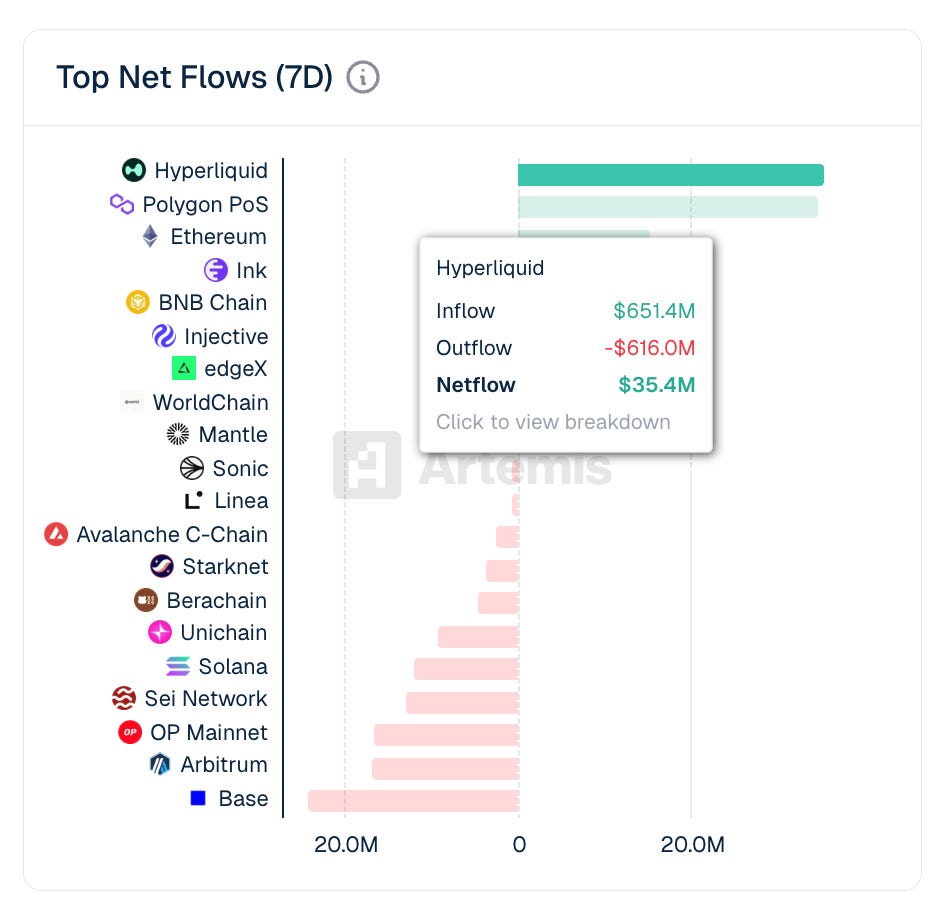

Hyperliquid leads 7D Top Net Flows Chart

Other notable news

Polymarket exchange upgrade — Rebuilt trading engine, new smart contracts, and a native Polymarket USD collateral token replacing USDC.e, rolling out over 2-3 weeks. Comes as daily fees hit $1.9M.

Polygon Labs — $100M stablecoin payments raise — Early talks to raise $100M for a regulated stablecoin payments business. Would put Polygon in direct competition with Stripe/Paradigm-backed Tempo, which launched mainnet last month.

ZachXBT — North Korean IT worker network — Data from an internal DPRK payment server exposed 390 accounts running ~$1M/month through fake identities and crypto-to-fiat networks. The most detailed public view of North Korea’s crypto laundering infrastructure to date.

Canary Capital PEPE ETF S-1 — Filed following prior MOG and Pengu filings. Whether the SEC engages substantively will signal how far the new regulatory posture actually extends.

France crypto wallet declaration law — Taxpayers holding >€5K in self-custody must now declare to tax authorities. Significant expansion of crypto surveillance in the EU’s largest retail crypto market.

Coinbase ASIC license — First crypto exchange to secure an Australian Financial Services Licence. Consistent with the broader Coinbase institutional buildout narrative this week.

Roman Storm / Tornado Cash — Prosecutors rejected the bid to dismiss charges; retrial on money laundering and sanctions counts stays open. The most-watched smart contract developer liability case remains live.

Thanks for reading! Stay ahead this week by using the Artemis Terminal or pulling live data with =ART() in Excel.

Disclaimer: The authors of this content, as well as affiliates of Artemis Analytics, may have financial interests in the protocols or tokens mentioned. This does not constitute investment advice or a recommendation to buy, sell, or hold any asset. The information provided is for educational purposes only and should not be relied upon for financial, legal, or tax decisions. Readers should assess their own circumstances before making any financial choices. Views expressed may change without notice, and Artemis Analytics is not liable for any losses resulting from the use of this content.