Artemis Weekly Digital Finance Fundamentals 2026.02.20

This week we cover Crypto ETFs, Morpho, Hyperliquid, and Figure's new DA

Welcome back to Artemis’ Weekly Digital Finance Fundamentals!

Market Overview: The Weekly Recap

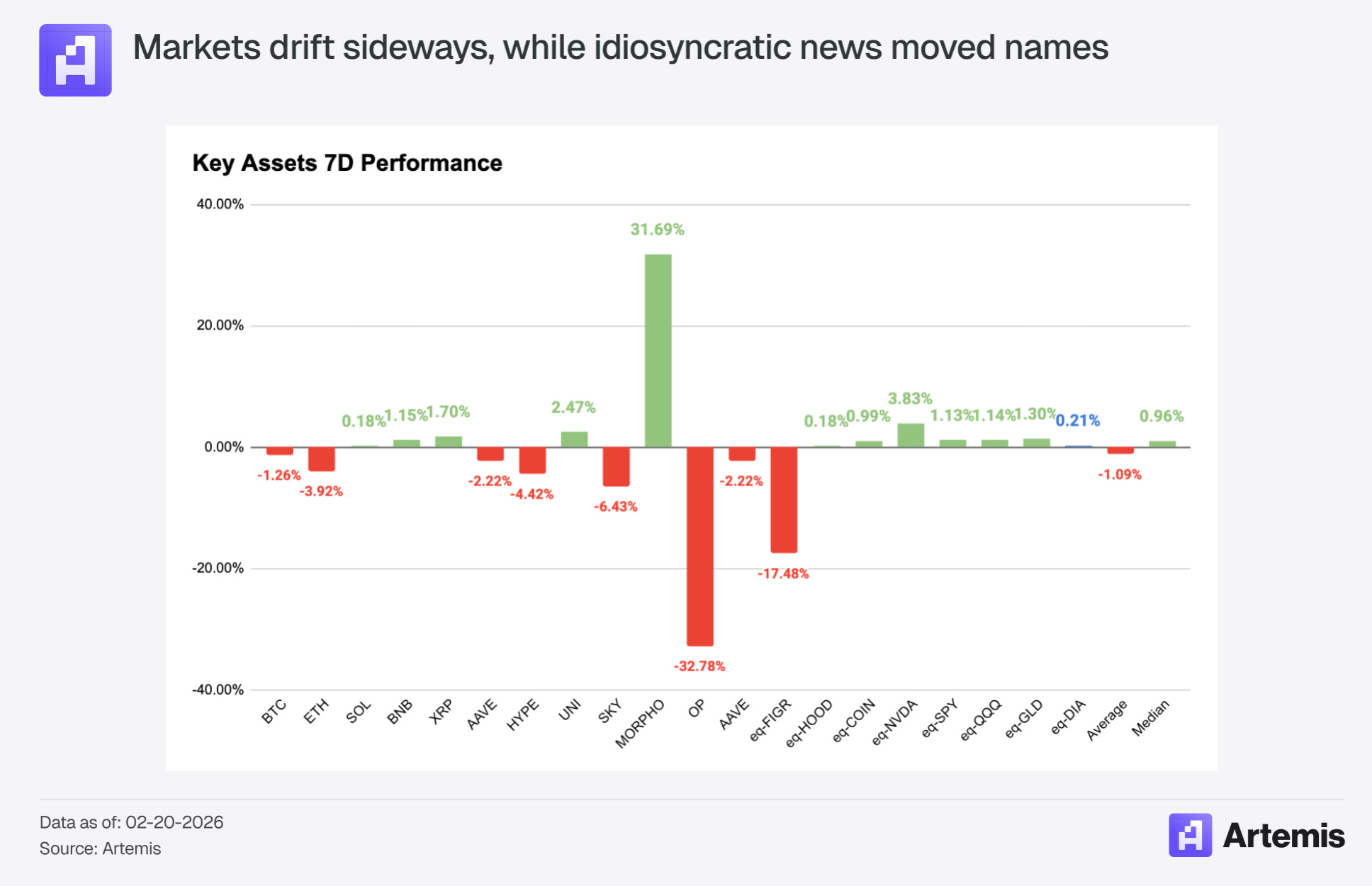

This week’s moves were unusually story-driven. Most of the crypto market drifted — BTC down 1.26%, ETH down 3.92%, equities largely flat — but a few names repriced hard on specific news.

MORPHO led everything at +31.69%, driven by the Apollo deal covered above. On the other side, OP was the week’s biggest loser at -32.78%. Coinbase announced that Base is forking away from Optimism’s OP Stack to build its own unified, in-house codebase, and taking its sequencer revenue with it — over 8,000 ETH that had previously flowed into Optimism’s treasury. Base was the Superchain’s most important tenant, and now it’s gone independent. The market priced that in immediately.

FIGR, Figure Technology’s blockchain-native lending platform, was down 17.48%, continuing a slide from its January peak of $78. The company is legitimately interesting — it launched a tokenized version of its own stock this week — but the stock had run nearly 40% in January alone and has been correcting ever since. SKY (-6.43%) and UNI (-4.42%) rounded out the losers with no obvious single catalyst beyond general DeFi malaise.

Today We Highlight:

Crypto ETFs: Artemis begins supporting Crypto ETF data as Sui staking ETFs hit the market

Hyperliquid Hits the Forbes FinTech 50

Figure Launches OPEN: New tokenized equity platform could eliminate DAT discounts to NAV.

Morpho: Major institutional integrations drive upside while peers falter in the bear market.

1. Crypto ETFs

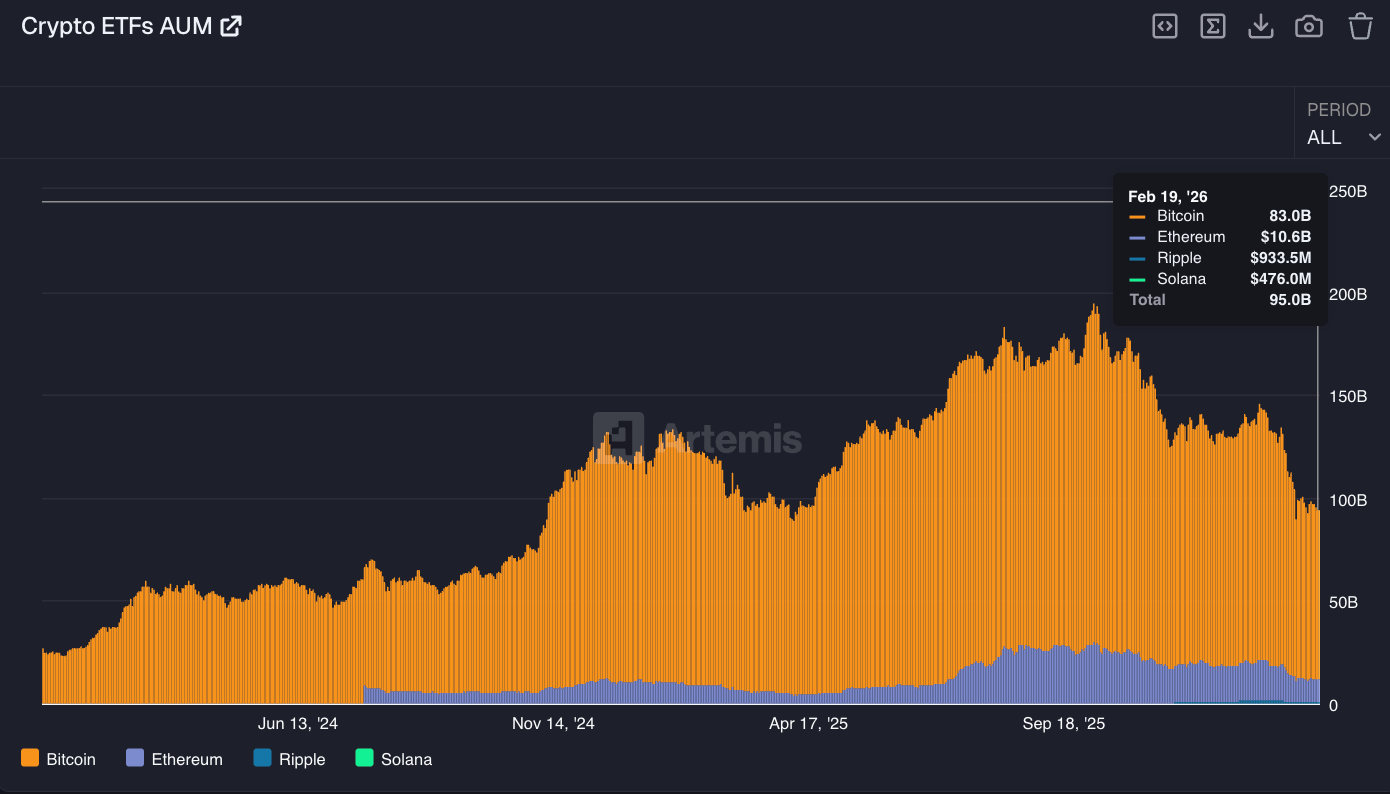

First, we announce that Artemis has expanded its coverage to include ETF-level data — flows, AUM, and more — across four major crypto assets: Bitcoin, Ethereum, Solana, and XRP. This comes at a critical juncture, as institutional digital asset holders like ETFs and digital asset treasuries under closeThe crypto ETF market just had its most eventful few months since the original Bitcoin ETF approvals, and the picture looks very different depending on which asset you’re watching.

The headline numbers from 2025 are deceptively tidy: crypto ETFs pulled in roughly $34 billion in net inflows for the year, nearly matching 2024’s haul. But zoom in, and the story fractures.

The October 10th market shock cracked the veneer. Total outflows since that date hit $3.2 billion — and they were brutally concentrated in Bitcoin and Ethereum. IBIT alone, BlackRock’s Bitcoin behemoth that was briefly flirting with $100 billion in AUM, watched assets retreat sharply as price support repeatedly failed to hold. Excluding IBIT, every other U.S. spot Bitcoin ETF collectively bled $3.2 billion in net outflows across the full year — a sobering stat that reveals just how much of the “Bitcoin ETF success story” is really just one fund doing all the heavy lifting.

The more interesting subplot is what’s happening at the margins. XRP and Solana ETFs, which both launched in November, generated notable activity despite debuting at what one strategist called a “disadvantageous time” — with macro conditions already souring. Yet investors kept buying. XRP ETFs crossed $1 billion in cumulative inflows. Solana products, notably among the first U.S. ETFs to pass staking rewards directly to investors, accumulated nearly $880 million in AUM since launch. During weeks when Bitcoin and Ethereum products were hemorrhaging capital, XRP and Solana ETFs recorded their largest weekly inflows since inception — a rotation that looks less like irrational exuberance and more like institutional investors quietly taking a view on what the next cycle’s winners might be.

The structural story hasn’t changed: ETFs have made crypto genuinely accessible to institutional capital, and the product menu keeps expanding. Just this week, Canary Capital and Grayscale both launched spot Sui ETFs (SUIS and GSUI), offering regulated exposure to SUI alongside roughly 7% staking rewards passed through to investors via NAV. Dogecoin already has three spot ETFs trading, the most recent being 21Shares’ Foundation-endorsed TDOG, which launched on Nasdaq in January. Cardano, Polkadot, and Avalanche are all still in the queue. Analysts project more than 100 new crypto ETFs could launch in 2026. Whether that reflects genuine broadening demand or just issuers throwing product at the wall is probably the defining question for crypto markets this year.

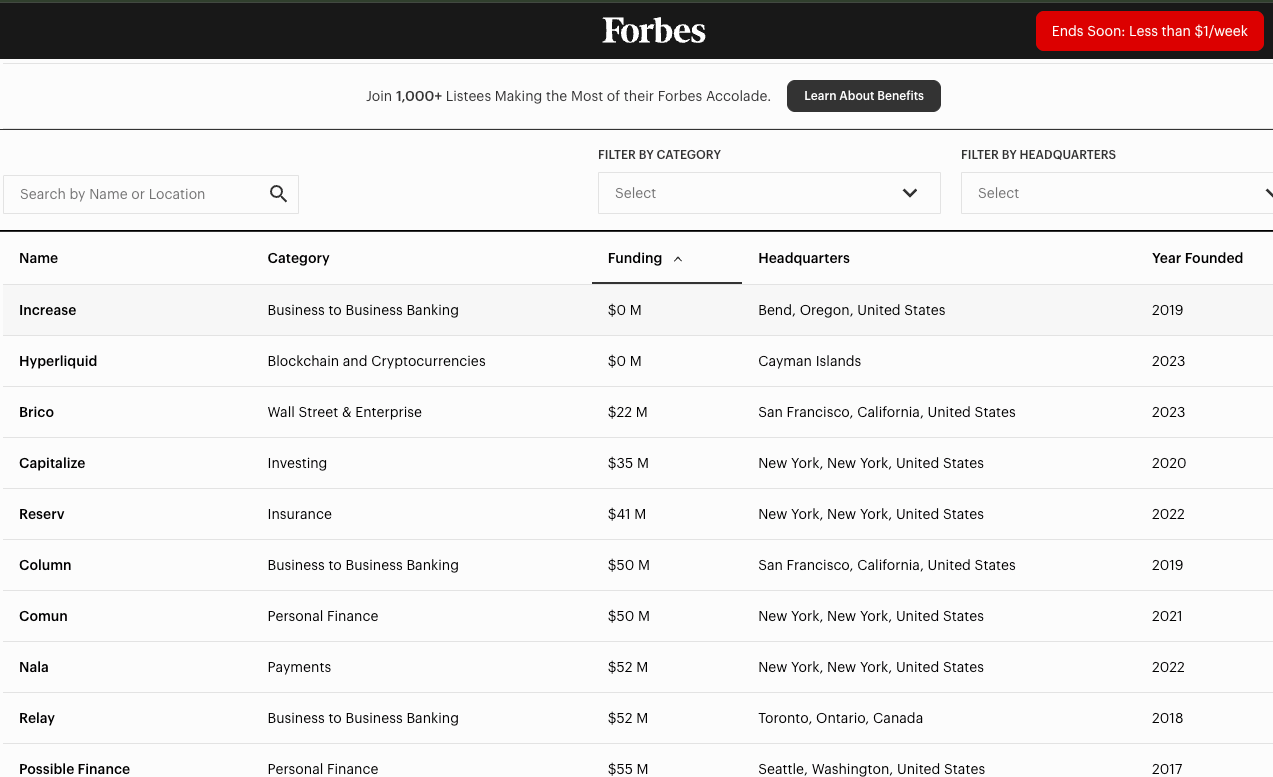

2. Hyperliquid Lands on the Fintech 50 Despite $0 in VC Funding

In a sector often defined by mega-raises and venture-backed hype, Hyperliquid is proving that execution is king. The DEX officially landed on the Forbes Fintech 50 this week, standing out with a reported $0 in external funding. While competitors spend cycles on roadshows and dilutive rounds, Hyperliquid has quietly built a dominant perp-stack that now rivals CEXes.

It’s a sobering reminder for the industry: you don’t need a massive VC war chest to build a top-tier financial platform, you just need a product that people actually want to trade.

Hyperliquid.

3. Figure’s OPEN: A Structural Fix for DAT Discounts

Figure Technology Solutions officially launched its On-chain Public Equity Network (OPEN) this week, debuting its own Series A Blockchain Common Stock in an upsized $150M secondary offering. This is not just a “tokenized” wrapper for traditional shares; these are blockchain-native securities registered on the Provenance Blockchain and traded on Figure’s Alternative Trading System (ATS).

What makes Figure’s ATS Unique?

Trading on a public blockchain improves upon traditional markets by offering 24/7 liquidity, direct lending capabilities, and lower costs through the elimination of middlemen.

Implications for DATs

Figure CEO Mike Cagney views the OPEN ATS as a structural cure for the “discount to NAV” plaguing Digital Asset Treasuries (DATs). By listing blockchain-native equity alongside traditional Nasdaq shares, DATs can enable a powerful arbitrage mechanism: managers can run tenders allowing investors to swap discounted shares for underlying crypto, forcing the market price back to par.

Beyond NAV, these on-chain shares offer superior capital efficiency. Cagney notes that “better collateral value and stock loan economics” create natural buying pressure, as holders can use shares as programmable collateral.

The Bottom Line

This model aligns economic incentives to eliminate the NAV discount, much like the GBTC conversion did for Bitcoin. If Figure’s ATS attracts sufficient liquidity, it creates a new playbook: owning a DAT provides amplified crypto exposure with the added utility of stock loan economics. It’s a potential structural fix that could turn a persistent downside risk into a premium.

4. Morpho

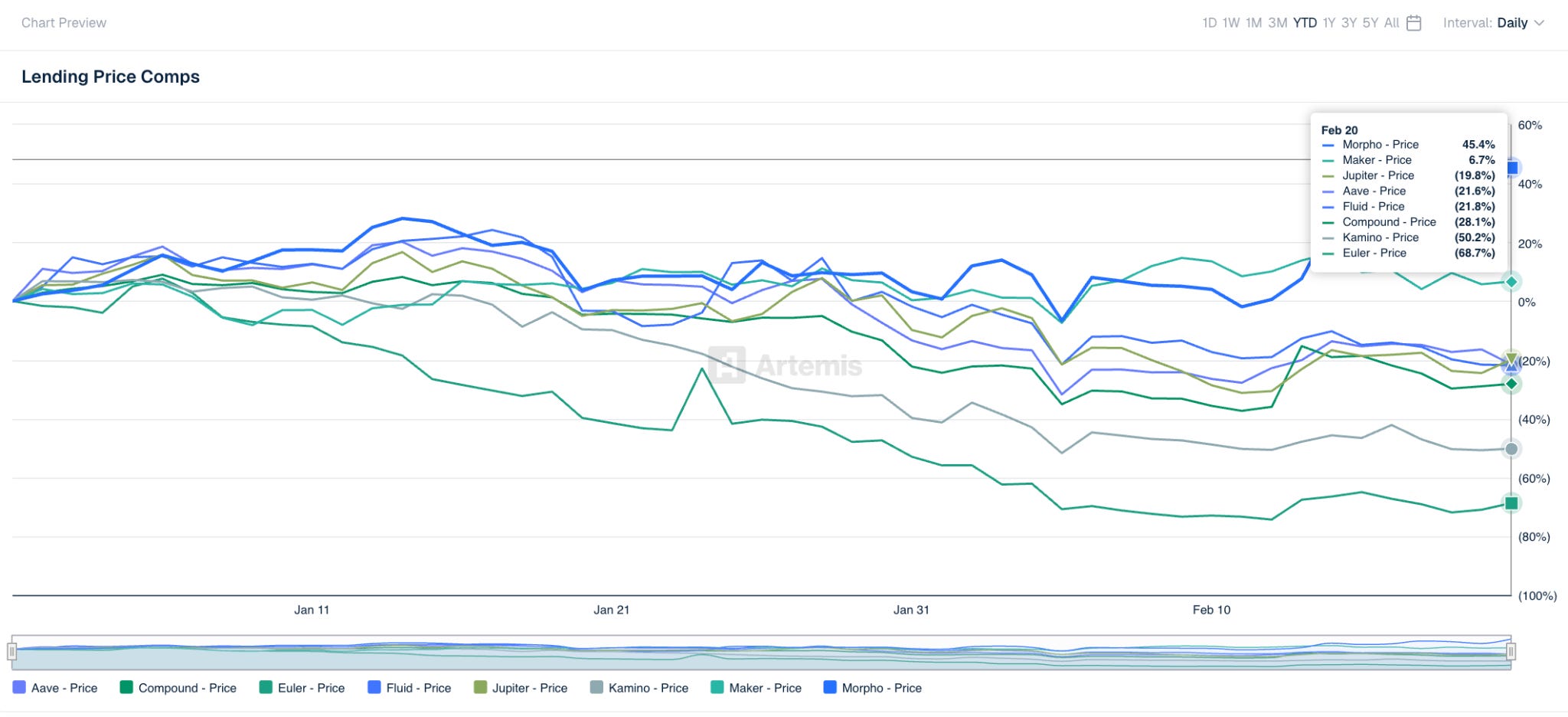

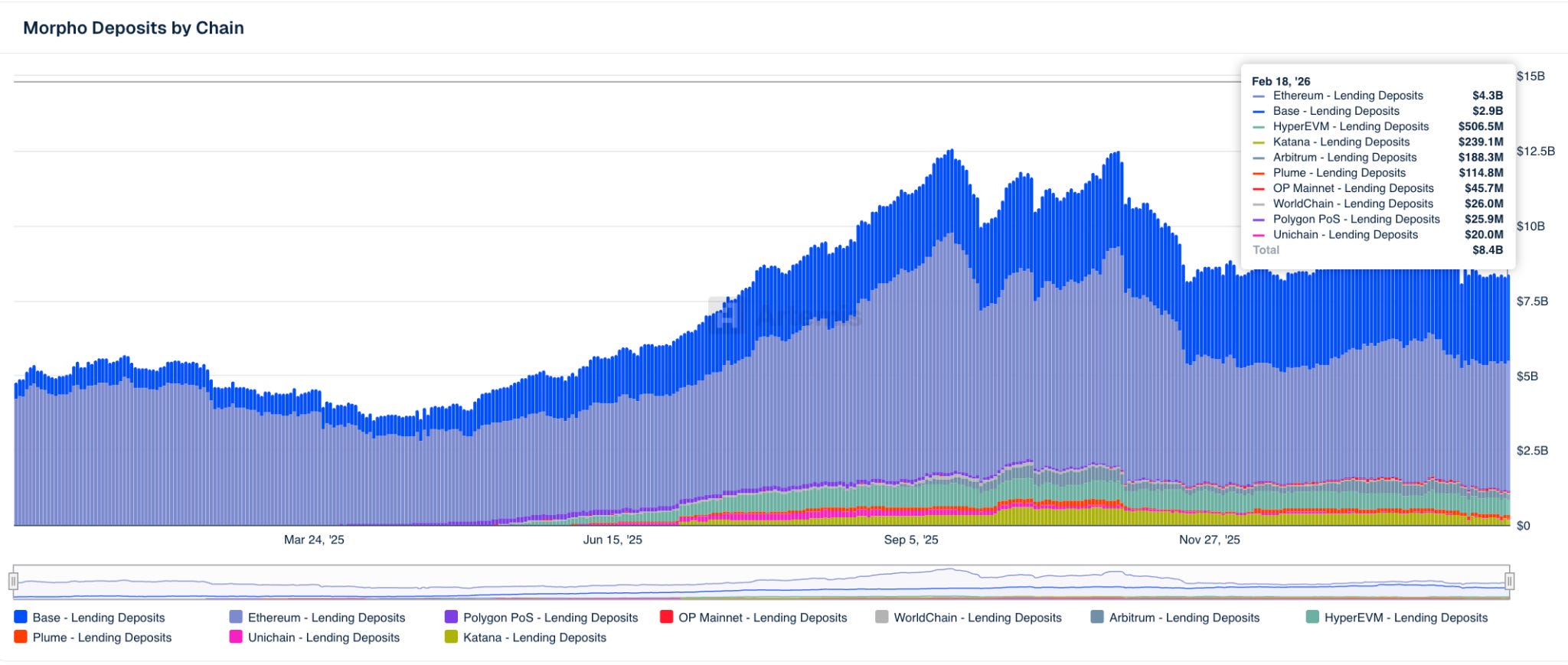

While most of the crypto market has been licking its wounds since October, MORPHO has been doing something unusual — going up. The token rebounded from a low of $0.97 on February 6 to around $1.54 today BanklessTimes, bucking the broader altcoin malaise. The move isn’t hard to explain: Morpho has spent the last several months accumulating a roster of institutional integrations that reads less like a DeFi protocol and more like a piece of core financial infrastructure. To put it into perspective, MORPHO is up 45% YTD, while its peers are down 20% or more.

Morpho’s core bet is on becoming the lending infrastructure layer that exchanges, banks, and fintechs embed into their own products — invisibly, under the hood. In 2025, deposits climbed from $5B to $13B, and active loans hit $4.5B. Coinbase integrated Morpho to power its crypto-backed lending product. Gemini, Crypto.com, Bitget, and Ledger followed. Société Générale became the first regulated bank to use DeFi to extend its loan book, building lending markets for its MiCA-compliant stablecoins directly on Morpho. Then last week, most importantly, Apollo Global Management announced it would acquire up to 90 million MORPHO tokens over 48 months — a ~$112M commitment at current prices, structured to give one of the world’s largest alternative asset managers a direct governance stake in the protocol.

The Apollo deal deserves more than a headline. This is a 48-month structured acquisition with transfer restrictions — not a fund taking a speculative flier. Apollo manages over $600 billion in assets and has been loudly positioning itself in private credit and on-chain lending. RWA deposits on Morpho grew from near zero at the start of 2025 to $400M by Q3, with assets from managers like Apollo and Fasanara already being used as collateral. The upcoming V2 adds fixed-rate, fixed-term loans — the kind of instrument structure institutions can actually underwrite. The risks are real: token unlocks run to 2028, fee distribution to tokenholders isn’t yet active, and MORPHO remains a DeFi altcoin in a risk-off market. But in a sea of down-only charts, the fundamental story behind this price action is unusually coherent.

Charts of the Week

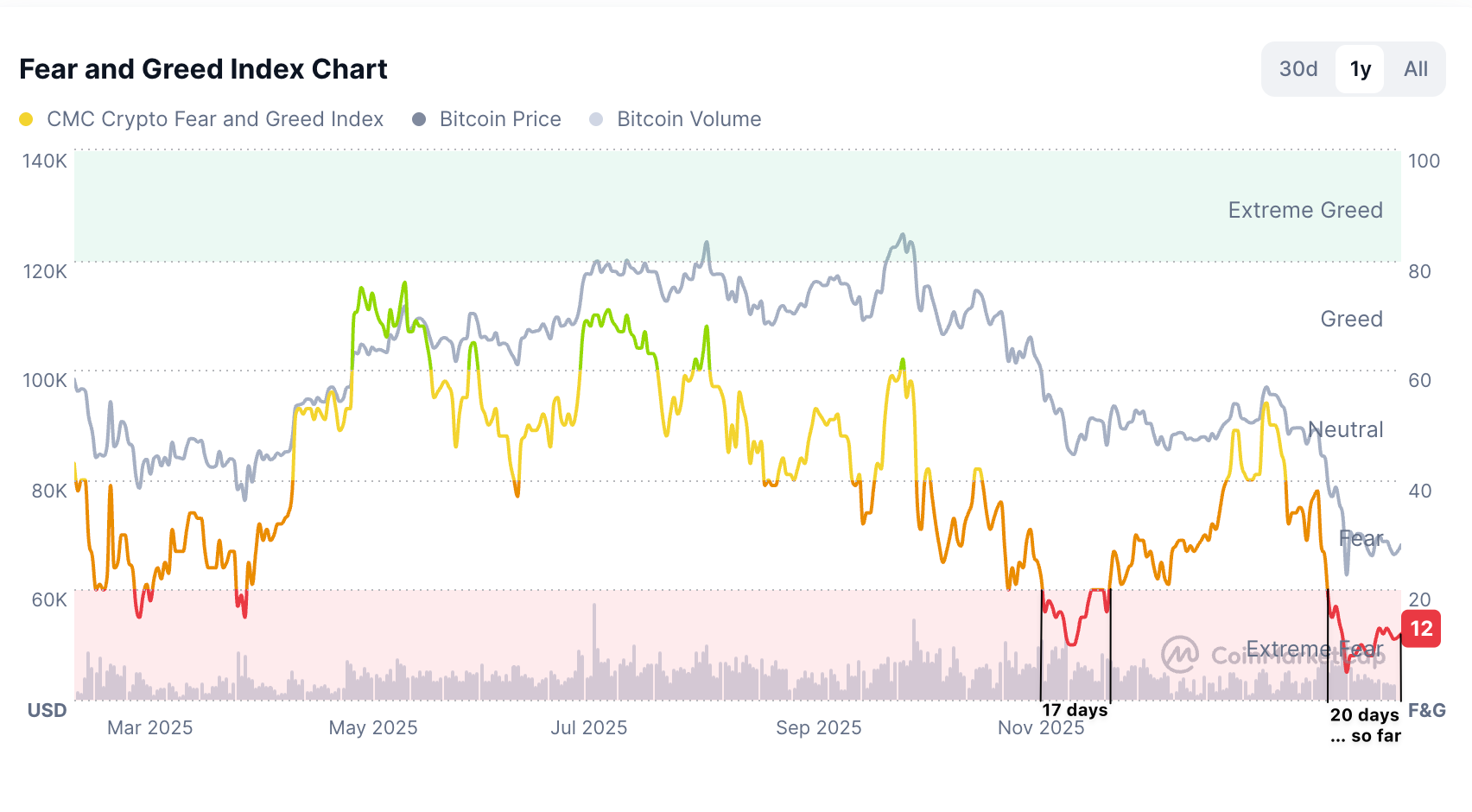

Fear and Greed Index — Crypto Fear and Greed Index extends its longest consecutive run in the “Extreme Fear” region at 20 days.

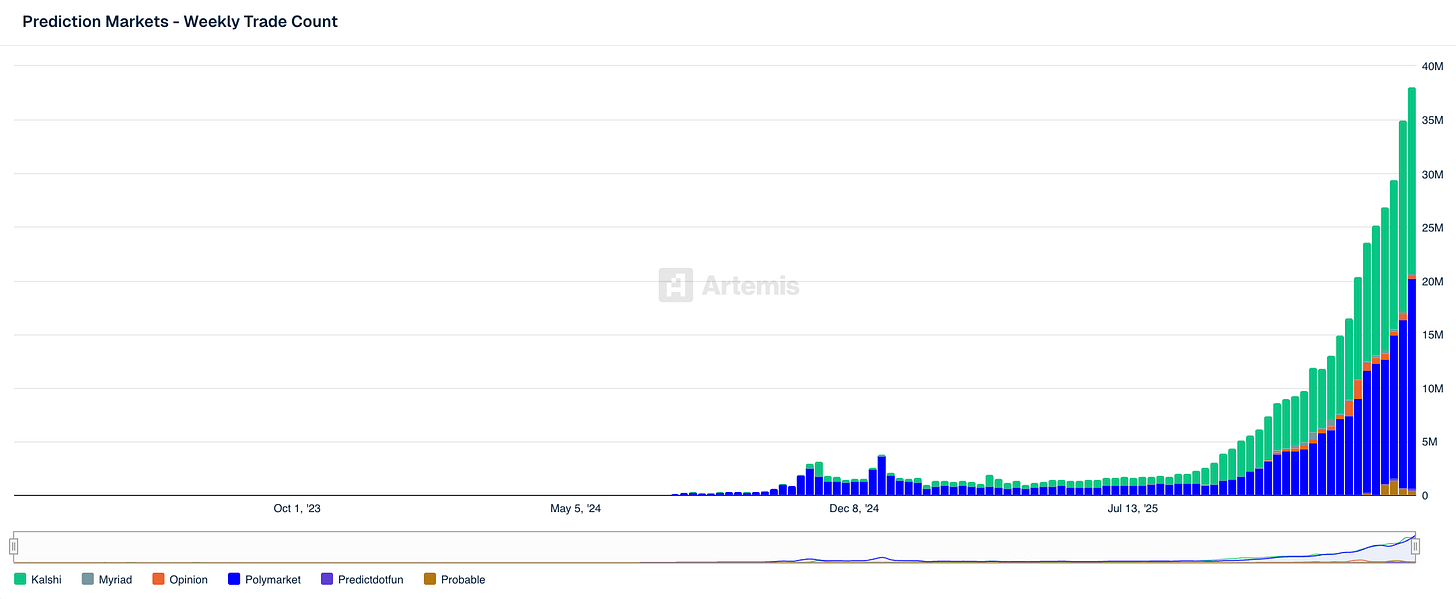

Prediction Market Usage Accelerates — No, this is not a cumulative chart, week over week prediction market trade counts continued to increase even after the Superbowl

Other Notable News

Thanks for reading! Stay ahead this week by using the Artemis Terminal or pulling live data with =ART() in Excel.

Disclaimer: The authors of this content, as well as affiliates of Artemis Analytics, may have financial interests in the protocols or tokens mentioned. This does not constitute investment advice or a recommendation to buy, sell, or hold any asset. The information provided is for educational purposes only and should not be relied upon for financial, legal, or tax decisions. Readers should assess their own circumstances before making any financial choices. Views expressed may change without notice, and Artemis Analytics is not liable for any losses resulting from the use of this content.

Curious where you guys are at with $LINK/$GLNK given the infrastructure they have built up?