Artemis Weekly Digital Finance Fundamentals 2026.3.2

This week we cover impactful writing, graveyards of the previous cycle, new SEC filings, and lending protocols' outperformance.

Welcome back to Artemis’ Weekly Digital Finance Fundamentals!

Market Overview: The Weekly Recap

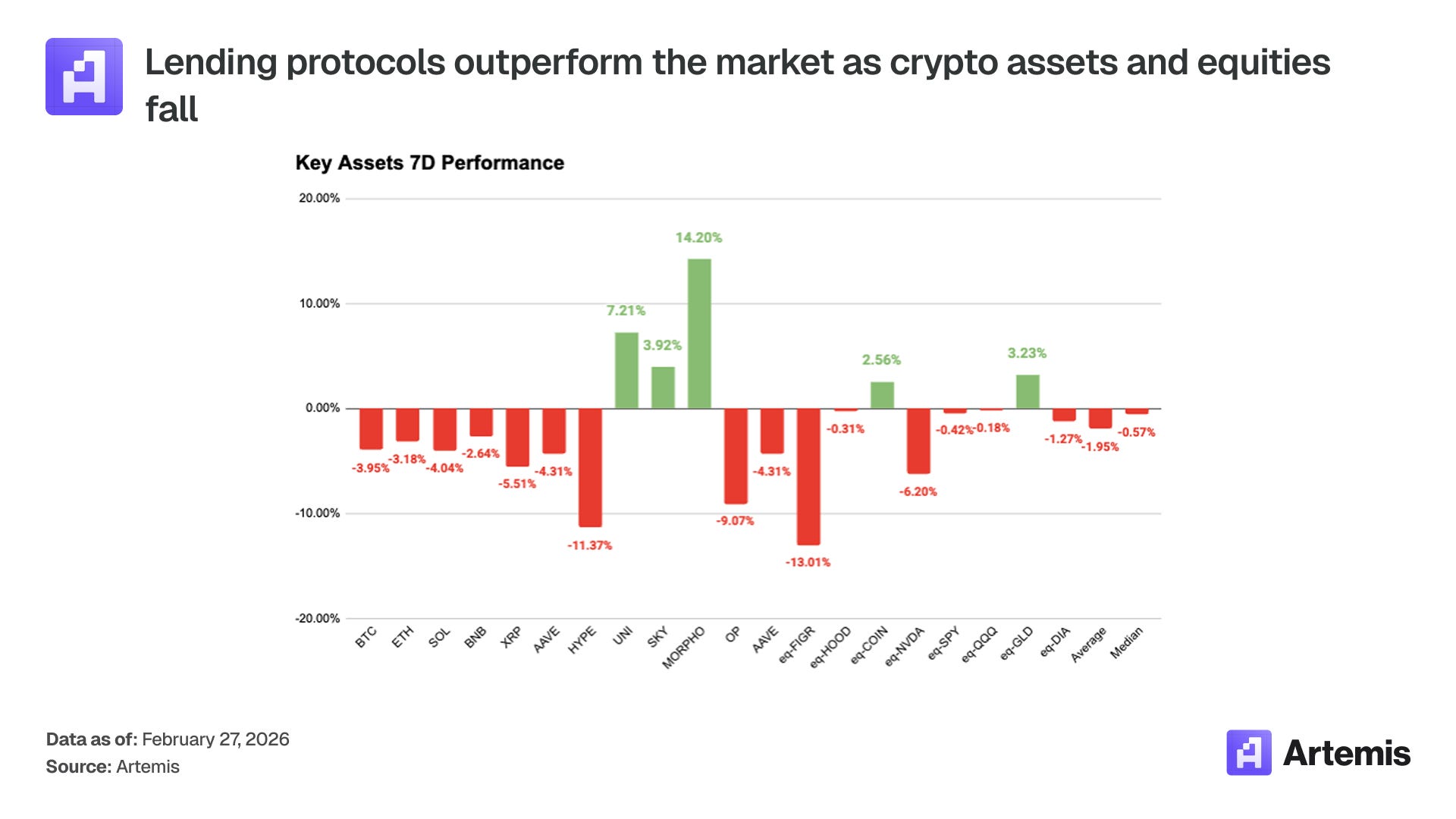

This week’s moves emulated closely what we saw last week: majors drifted lower alongside a risk-off tape. BTC (-3.95%), ETH (-3.18%), and SOL (-3.47%) all closed red on the week, while a handful of idiosyncratic names managed to buck the trend.

MORPHO extended last week’s breakout (+31.69%) with another strong week (+14.20%) following headlines around its collaboration with Apollo Global Management on onchain lending. SKY (+3.92%) and UNI (+7.21%) rounded out the winners as blue-chip DeFi stabilized after last week’s drawdown.

On the downside, HYPE was the week’s biggest loser (-11.37%) as volume stayed sluggish and the broader market continued to trend lower. FIGR (Figure Technology’s blockchain-native lending platform) fell -13.01%, extending last week’s decline and now down ~67% from its January 2026 ATH. Despite strong Q4 2025 earnings (revenue, net income, and EBITDA all up sharply YoY), investors appear to be pricing a tougher forward setup for growth and durability in a tighter funding regime.

Today We Highlight:

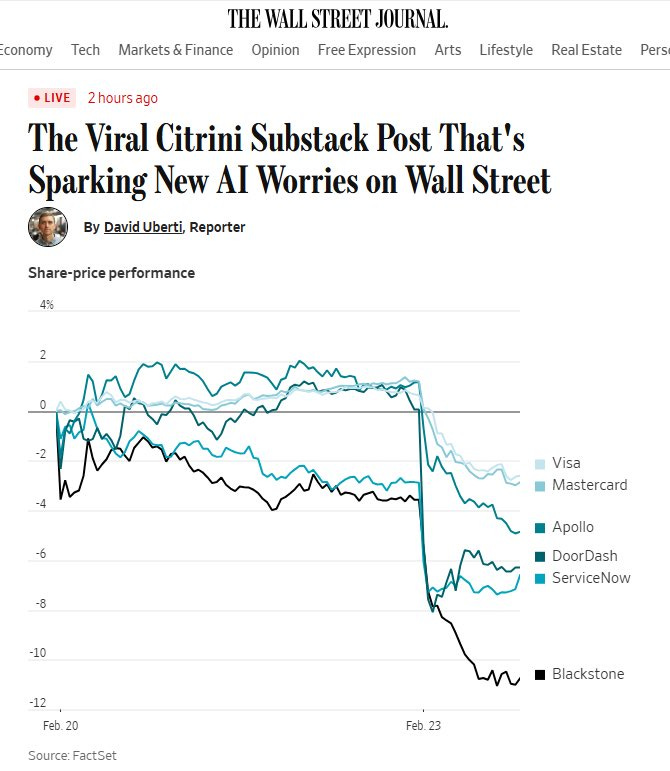

Citrini Research’s viral AI “doom-loop” memo catalyzed a sharp, correlated drawdown across “AI-adjacent” equities—less about fundamentals, more about positioning and reflexivity.

Jane Street was sued in connection with Terra/Luna, reviving the unresolved question at the heart of 2022’s collapse: where the line sits between market-making, opportunistic trading, and manipulation in thin, reflexive systems.

SEC guidance easing net capital treatment for “payment stablecoins” nudges them closer to cash status, aligning regulatory plumbing with how stablecoins already function as settlement money onchain.

1. How a Substack Article Caused the Market to Panic

A viral Substack post from Citrini Research sketched a near-future scenario where AI-driven productivity gains paradoxically trigger a demand shock: mass labor displacement → collapsing consumption → margin compression across “AI beneficiary” and “AI exposed” businesses alike. The memo name-checked specific public companies and, critically, named specific companies and products as part of their memo.

The result was immediate: a synchronized tape move across a basket of consumer/fintech/software names cited in the scenario (payments rails, delivery, ITSM, alternative asset managers, etc.). Reactions varied with many touting the research piece as informative and well-written to others such as Ed Zitron offering counter-commentary citing that the piece “profoundly pissed me off.”

Regardless of public praise or pushback, many of the industries and specifically named equities in the Citrini Research piece tumbled at market open on Monday, February 23rd.

2. Jane Street, Terra/Luna, and the Reminder That “Old Crypto” Risk Still Clears the Tape

A court-appointed administrator winding down Terraform Labs filed a lawsuit in Manhattan federal court accusing Jane Street (and specific individuals) of using material nonpublic information to trade around the May 2022 TerraUSD/Luna unwind, alleging the firm’s activity accelerated the collapse and generated large profits. Jane Street denied wrongdoing, framing the suit as an attempt to shift blame for a broader fraud.

Over the next ~48 hours (Feb 24 → Feb 25), crypto snapped into a relief rally: Bitcoin rebounded from roughly the $62.9k area on Feb 24 back toward $69k on Feb 25—about ~10% off the lows, with risk beta improving broadly across majors.

3. SEC Staff Guidance: Payment Stablecoins Move “Closer to Cash” for Broker-Dealer Net Capital

On Feb. 19, 2026, SEC Trading & Markets staff added a new FAQ (Q5) on broker-dealer financial responsibility stating they “will not object” if a broker-dealer treats a proprietary position in a “payment stablecoin” as having a “ready market” under Rule 15c3-1 and applies only a 2% haircut to the greater of the long/short position when computing net capital.

Why institutional desks should care

This is a narrow, staff-level step — but it directly hits the constraint that has kept a lot of regulated market infrastructure on the sidelines: capital drag.

2% haircut vs. punitive treatment changes economics. Under net capital, haircut assumptions determine whether an asset is “operationally usable” versus effectively dead weight on the balance sheet. Moving to a 2% haircut makes payment stablecoins viable working capital for broker-dealers in a way they weren’t before.

Enables real settlement/collateral workflows (for proprietary positions). If the firm can warehouse stablecoins without punitive capital charges, they become plausible for settlement, liquidity management, and intraday collateral movements — especially in tokenized securities / tokenized cash workflows that don’t map cleanly to legacy banking hours.

Signals “payment stablecoin” line-drawing. The FAQ is explicitly scoped to payment stablecoins and proprietary positions (not a blanket endorsement of all stablecoins, and not customer asset treatment). That’s important: it’s the SEC staff telling the market which category they’re willing to treat as money-like under specific conditions.

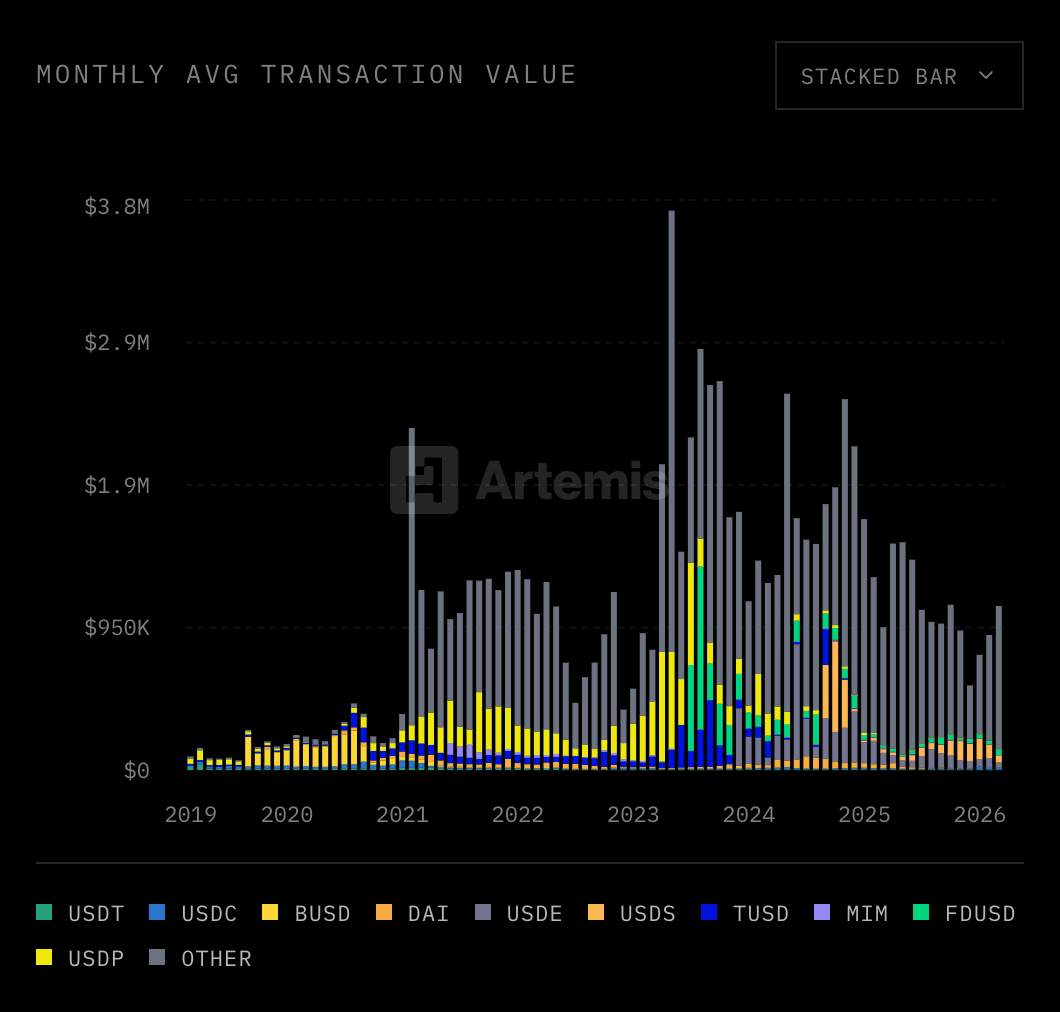

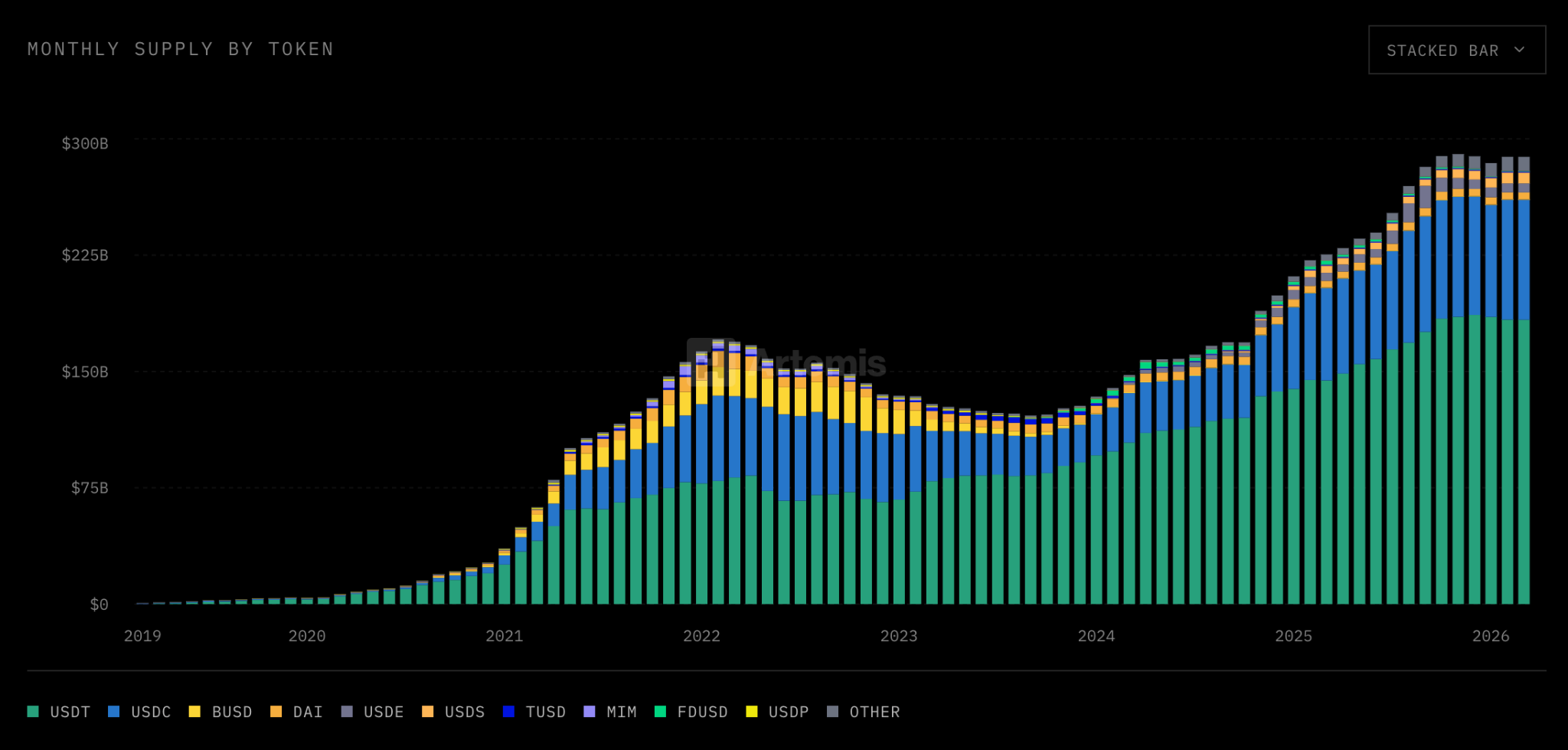

As institutions continue to involve themselves in stablecoins, specifically in payments and proprietary positions as outlined by the SEC’s latest clarifications, we anticipate two major data points will see significant changes.

Firstly, institutions transact with higher average transaction values with stablecoins, leading us to anticipate much higher average transaction values, particularly for the stablecoins with the most liquidity or new entrants supported by said institutions.

Secondly, we anticipate that the market share dominance of USDT by Tether and USDC by Circle will slowly erode as institutionally-backed stablecoins begin to enter the market.

Charts of the Week

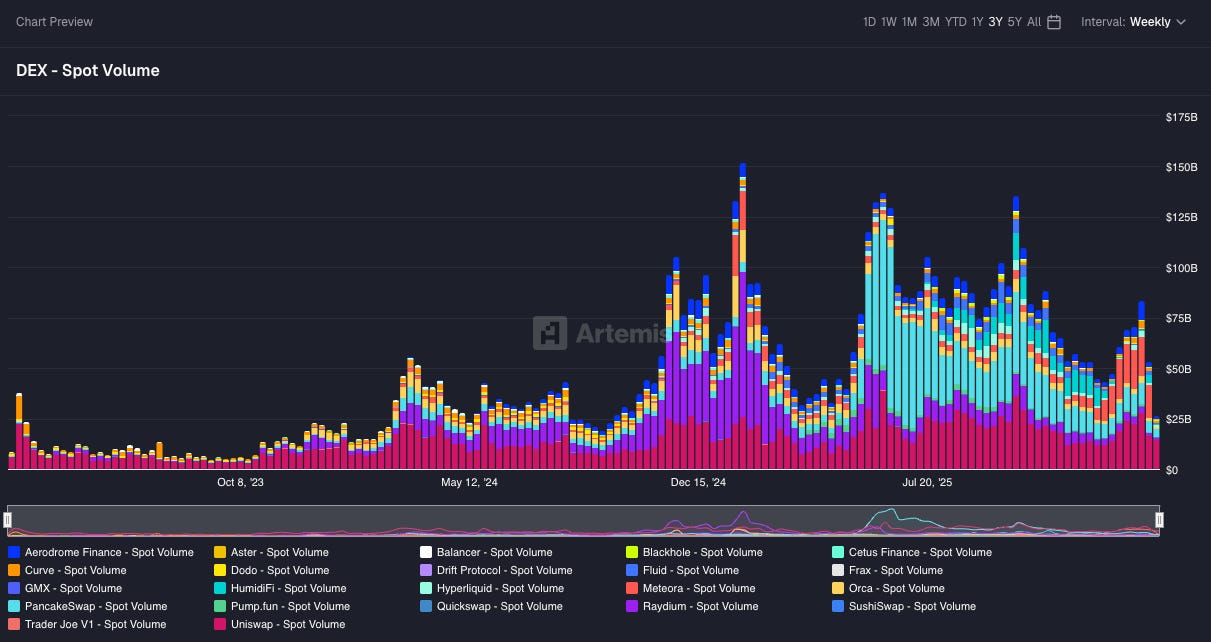

DEX Usage Continues to Drop Dramatically — After posting a YTD weekly high of $83.9B volume in the week ending February 8th, 2026, DEX volume across the industry has fallen nearly 68% as of February 22nd, 2026.

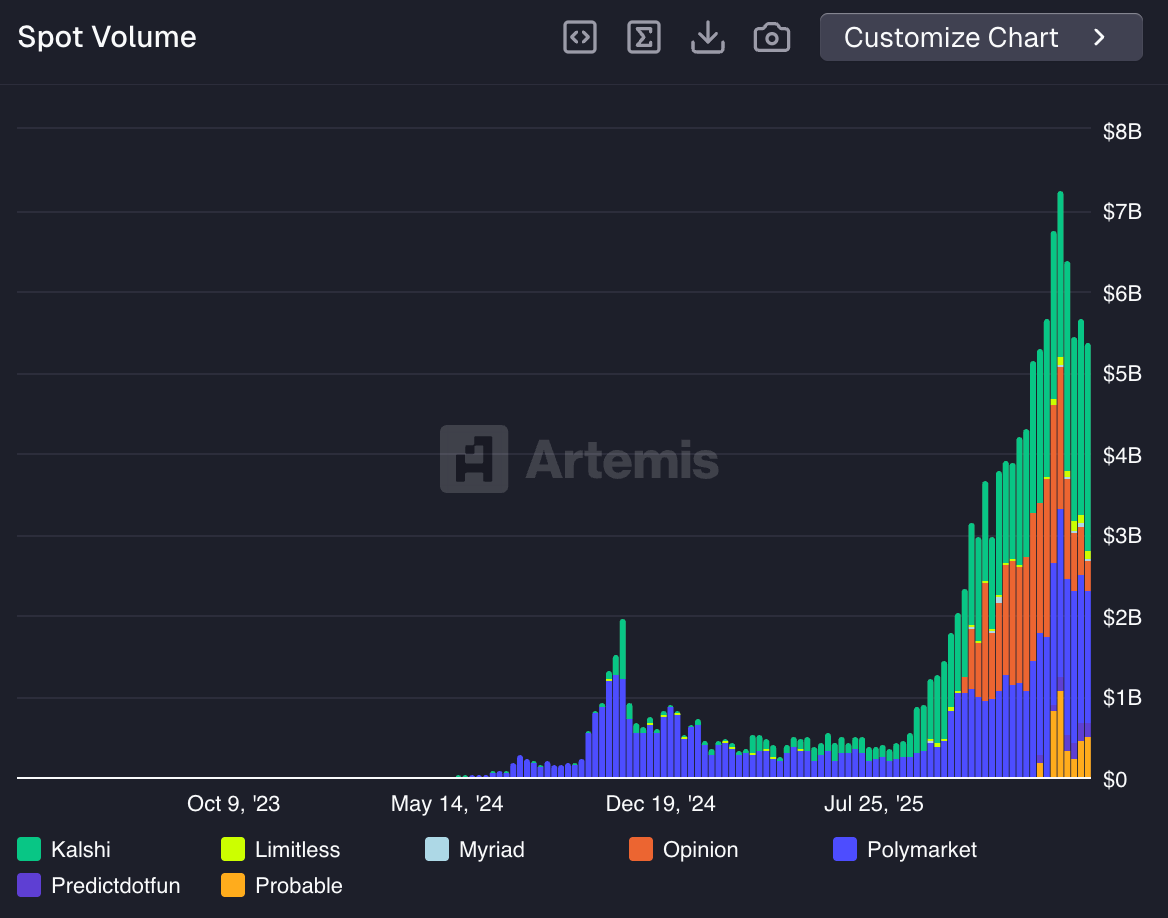

Prediction Market Volume Gradually Falls as NFL Season Ends — The NFL Season proved to be a significant driver of prediction market volume, as prediction market volume falls nearly 24% from the all-time highs of Super Bowl Weekend.

Other Notable News

Thanks for reading! Stay ahead this week by using the Artemis Terminal or pulling live data with =ART() in Excel.

Disclaimer: The authors of this content, as well as affiliates of Artemis Analytics, may have financial interests in the protocols or tokens mentioned. This does not constitute investment advice or a recommendation to buy, sell, or hold any asset. The information provided is for educational purposes only and should not be relied upon for financial, legal, or tax decisions. Readers should assess their own circumstances before making any financial choices. Views expressed may change without notice, and Artemis Analytics is not liable for any losses resulting from the use of this content.

LFG