Artemis Crypto Factor Model Analysis: April 2026 Update

An update on how beta, size, value, momentum, and fundamentals systematically drove crypto returns over the past month.

Executive Summary

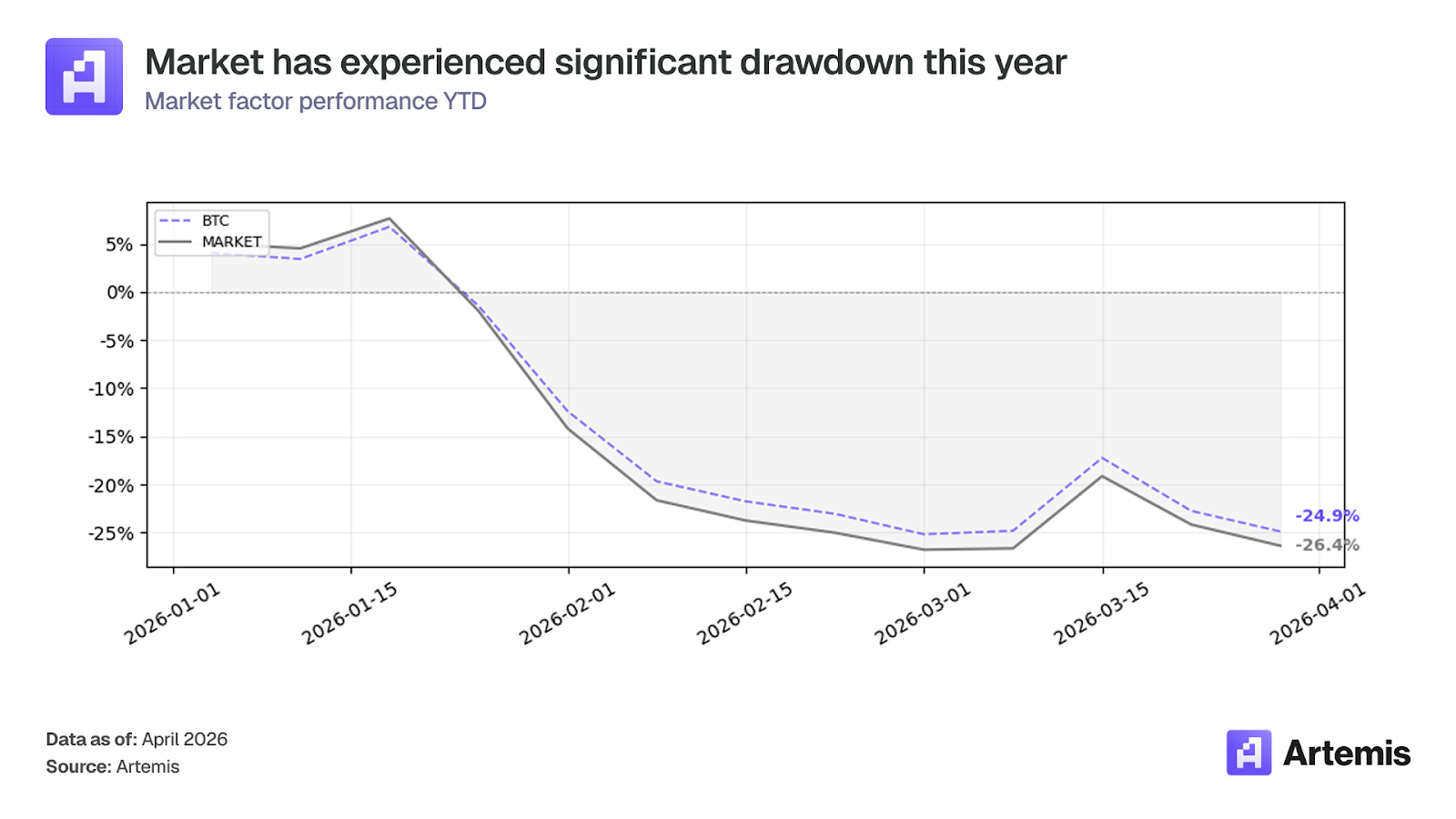

March was defined by the US-Israel war with Iran, which began February 28 and led to the closure of the Strait of Hormuz, disrupting 20% of global oil supplies and driving energy prices up 42%. Despite this, crypto was oddly resilient: the market factor fell just -1.81% while the S&P 500 dropped over 7%, suggesting much of the forced selling had already been flushed out in February’s -23.49% drawdown.

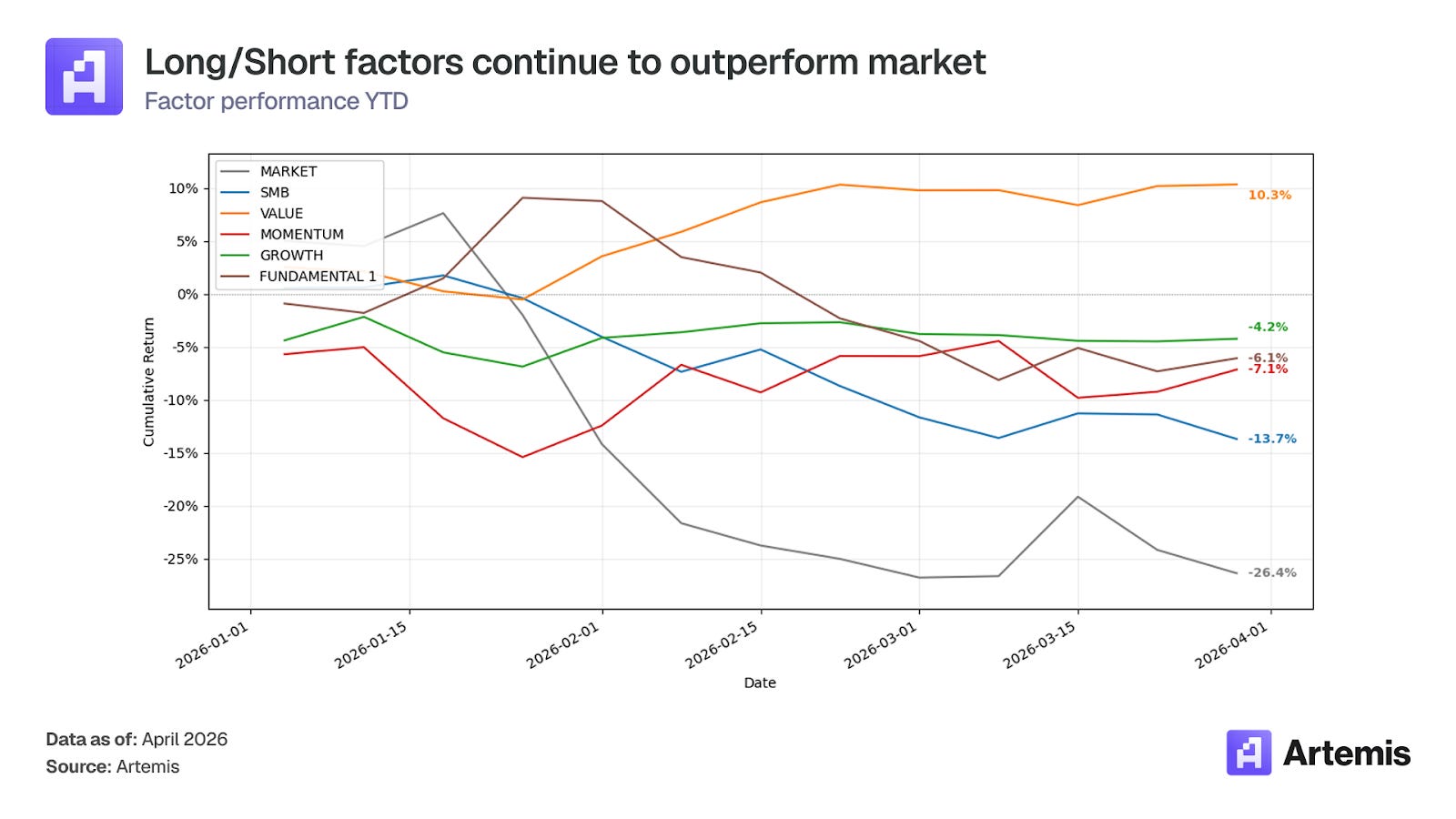

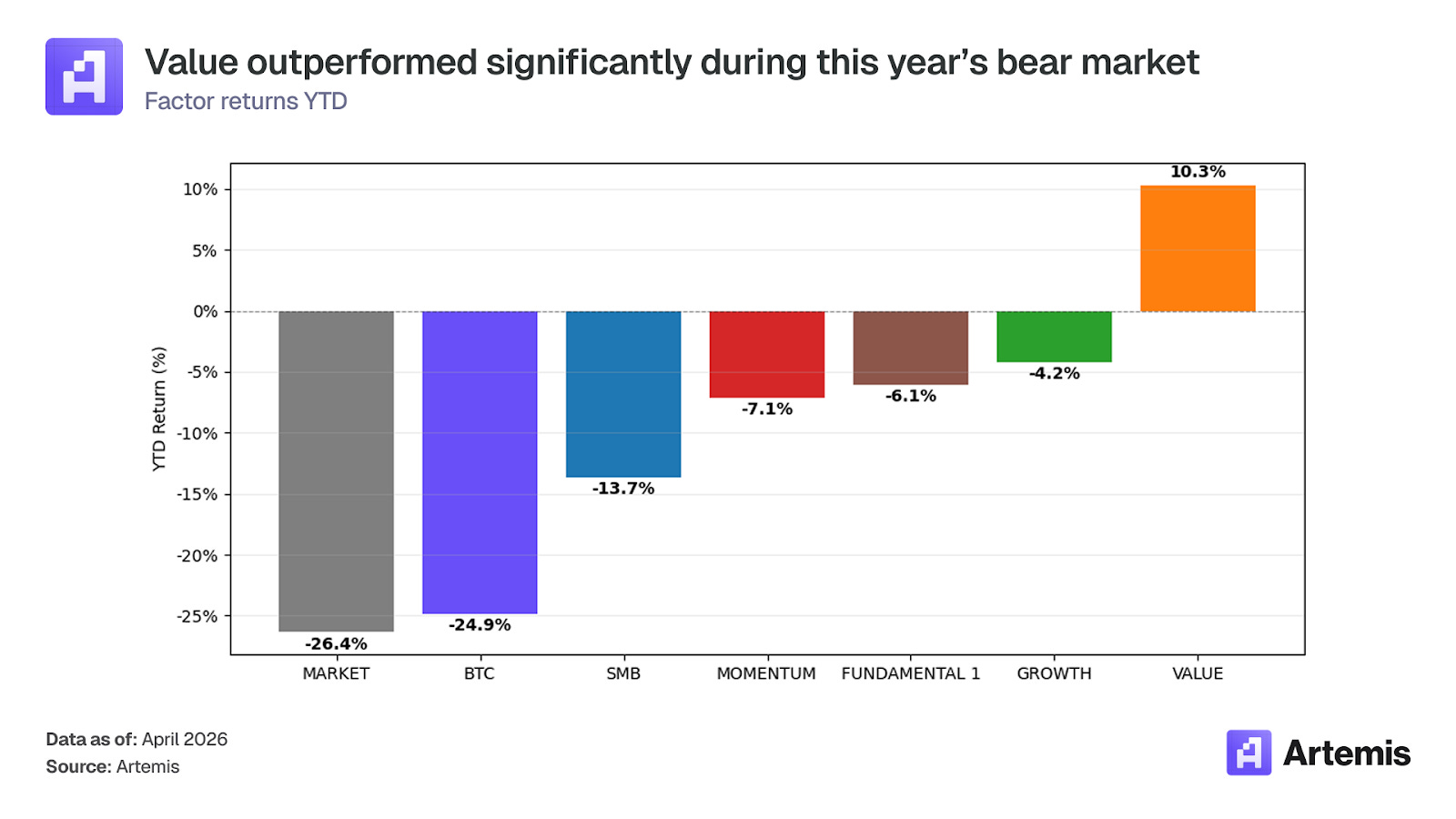

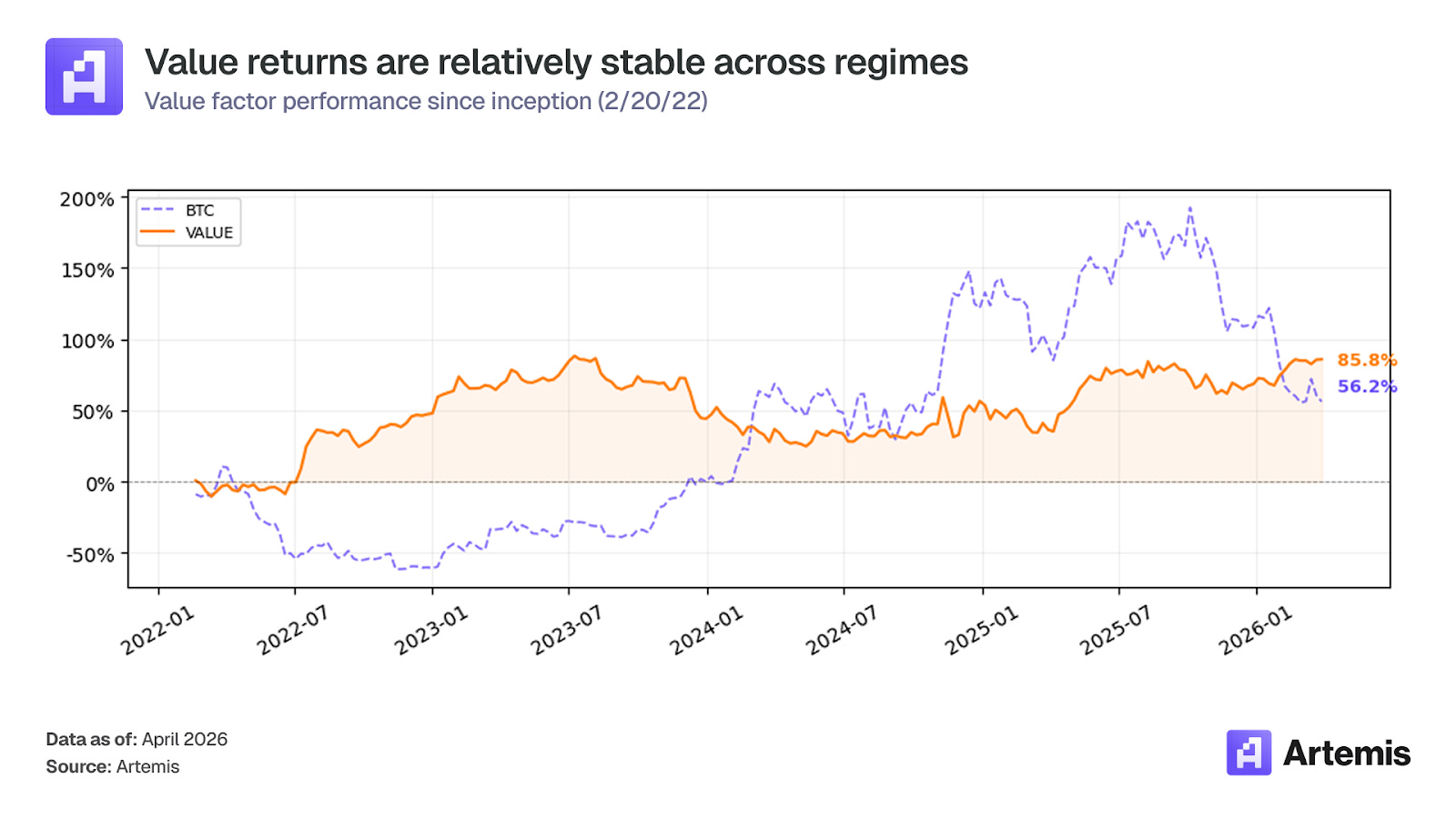

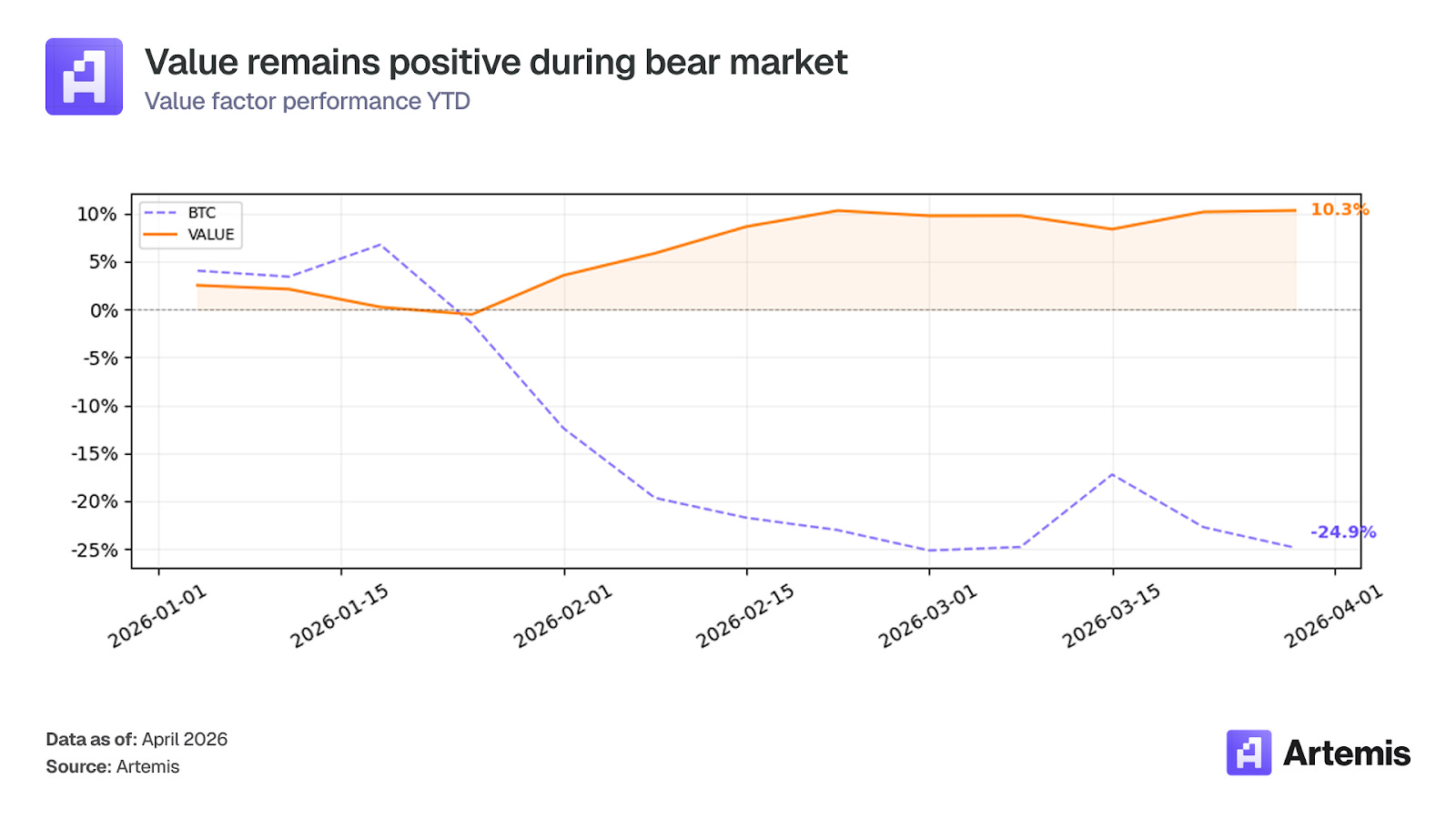

Value remains the strongest YTD performer among long-short factors at +10.33%, benefiting from its defensive profile as overvalued tokens in the short leg sold off harder than fundamentally cheap longs.

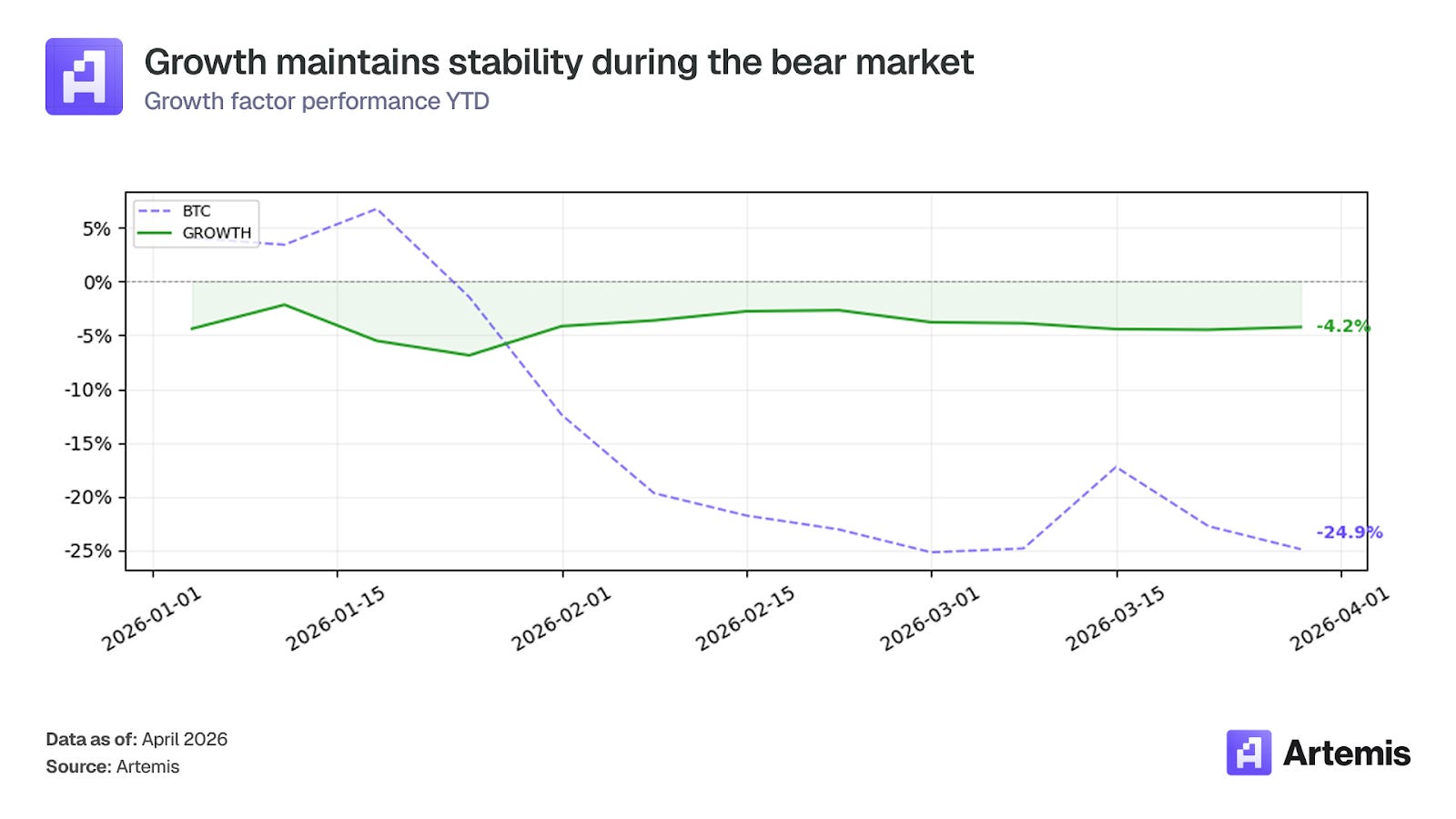

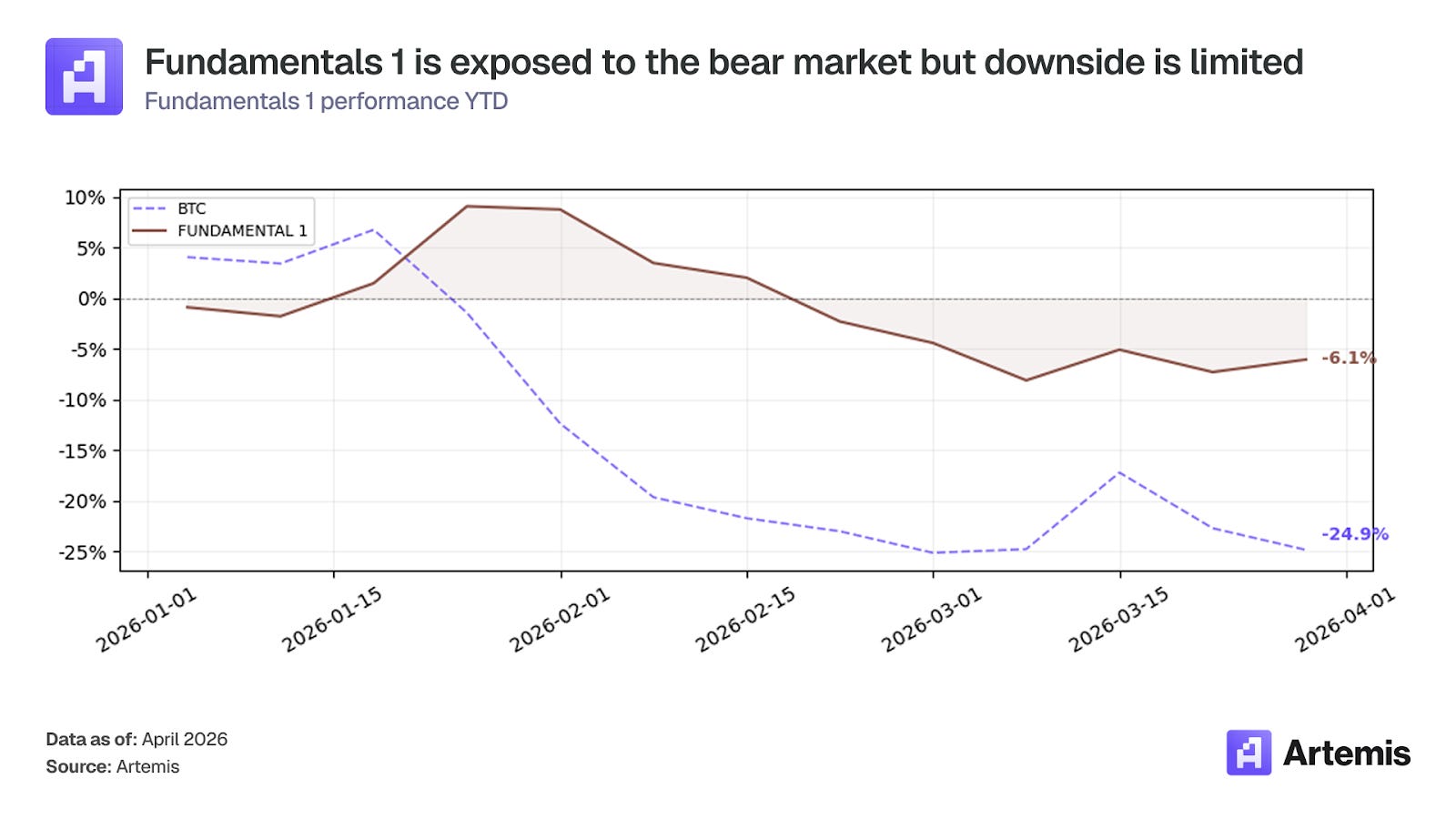

Even in a month where all five factors posted flat or negative returns, the long-short framework continues to significantly limit losses relative to passive exposure. YTD, the market factor is down -26.36% and BTC is down -24.9%, while Growth (-4.24%), Fundamentals 1 (-6.08%), and Momentum (-7.14%) have all preserved substantially more capital. The framework’s value is most apparent in drawdowns, not just in months where factors generate positive alpha.

The AI narrative was one of the few pockets of strength: NEAR rallied +25.32% after launching its “Confidential Intents” privacy upgrade and positioning itself as blockchain infrastructure for AI agents. TAO also surged, punishing short positions in SMB (-81.69%) and Fundamentals 1 (-73.81%).

DEXE was the single most impactful long position across factors, appearing as the top winner in both SMB and Momentum at +117.93%. On the short side, DeFi lending tokens AAVE, KMNO, and MORPHO all declined as a hawkish Fed hold at 3.5-3.75%, an unusual Aave liquidation event, and token unlock dilution pressured the sector.

Market Context

Sentiment around the past month has been mostly cautious as the war between US and Iran progressed. On February 28, the US and Israel launched surprise airstrikes on Iran, killing Supreme Leader Ali Khamenei. Iran retaliated with drone strikes and fighting has continued between the two countries. The Strait of Hormuz closed, disrupting 20% of global oil supplies, which drove energy and oil prices up 42% in March. The IEA agreed to release a record 400 million barrels of crude oil in response.

Despite the chaos, crypto was oddly resilient relative to equities. The crypto market failed to recover, but also didn’t dip further. The market fell -1.81% over March and BTC fell -2.39% over the month. Meanwhile, S&P fell over 7%, which could indicate that we’re at a bottom for the crypto market.

For a more in depth look into how each of the strategies were built, see our Crypto Factor Model Analysis and Analysis of Fundamentals 1 strategy. For a complementary guide on reading through this report, see our factors guide.

Performance Summary

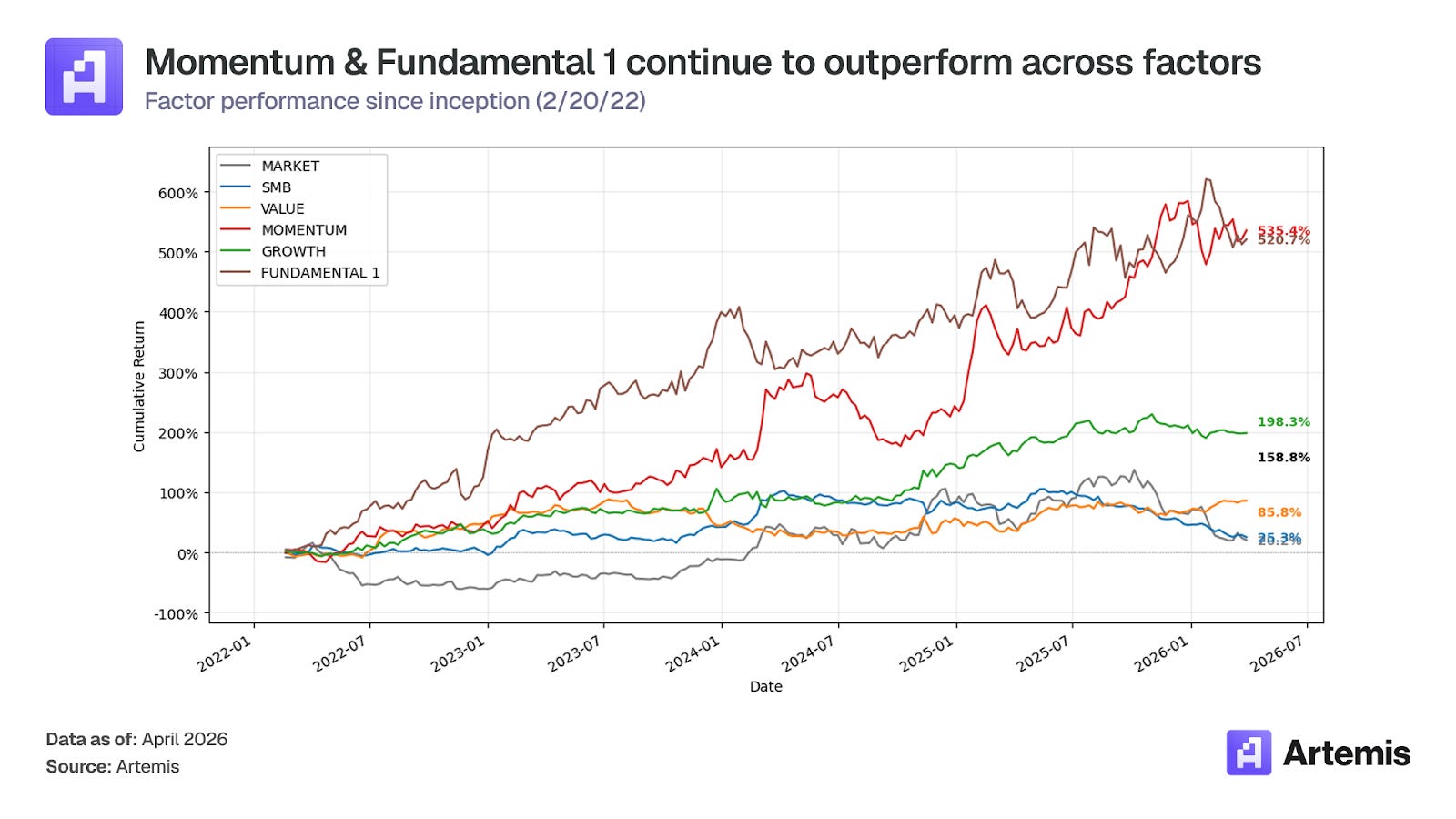

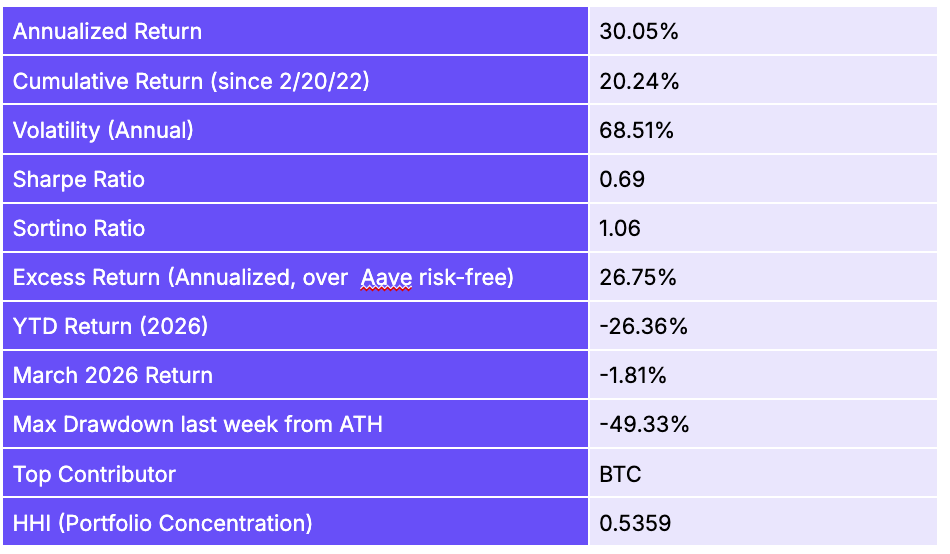

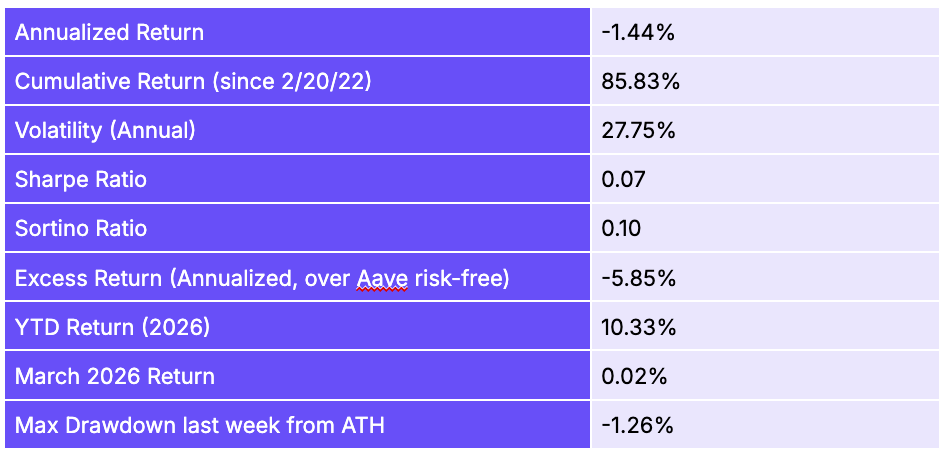

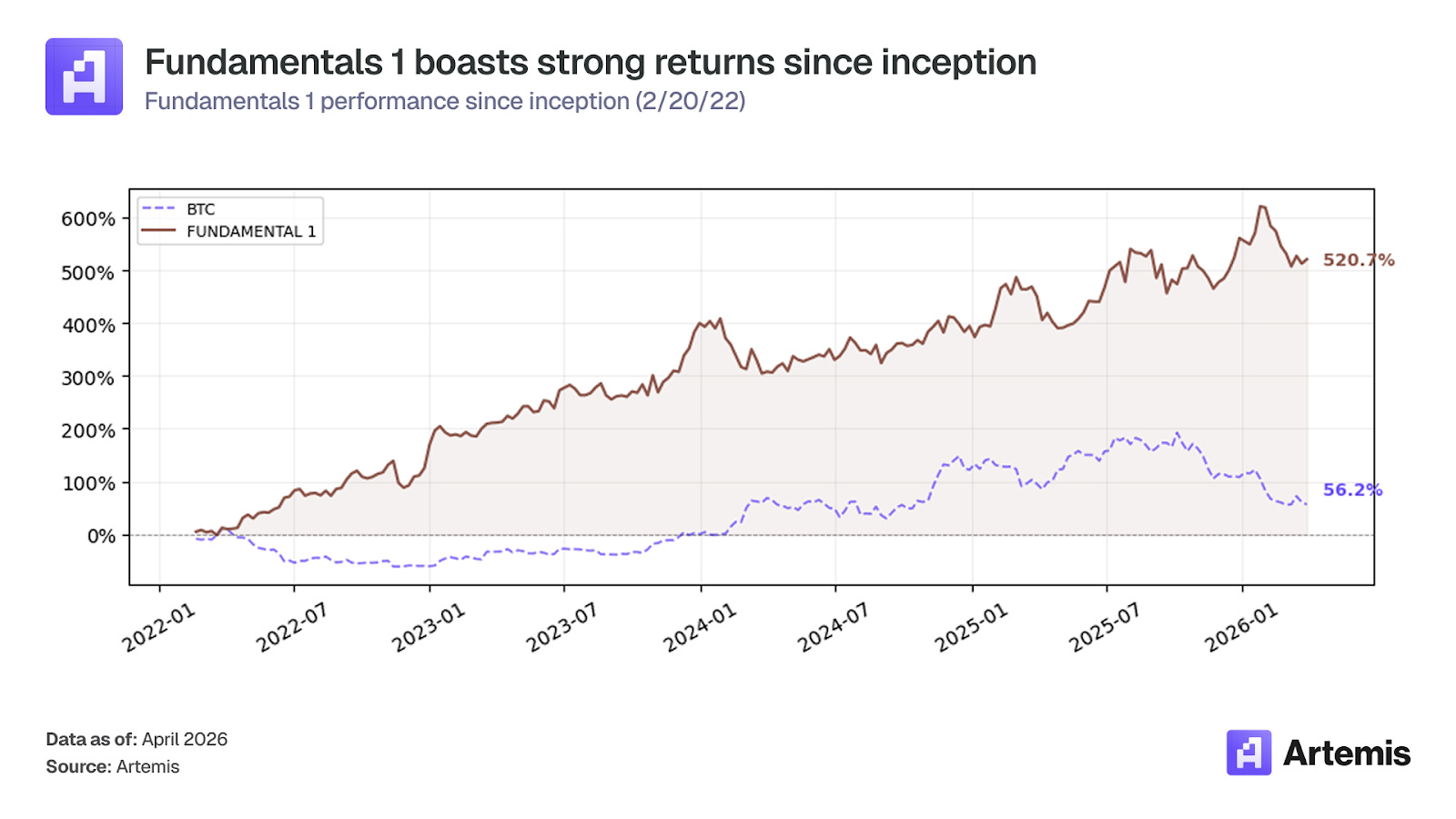

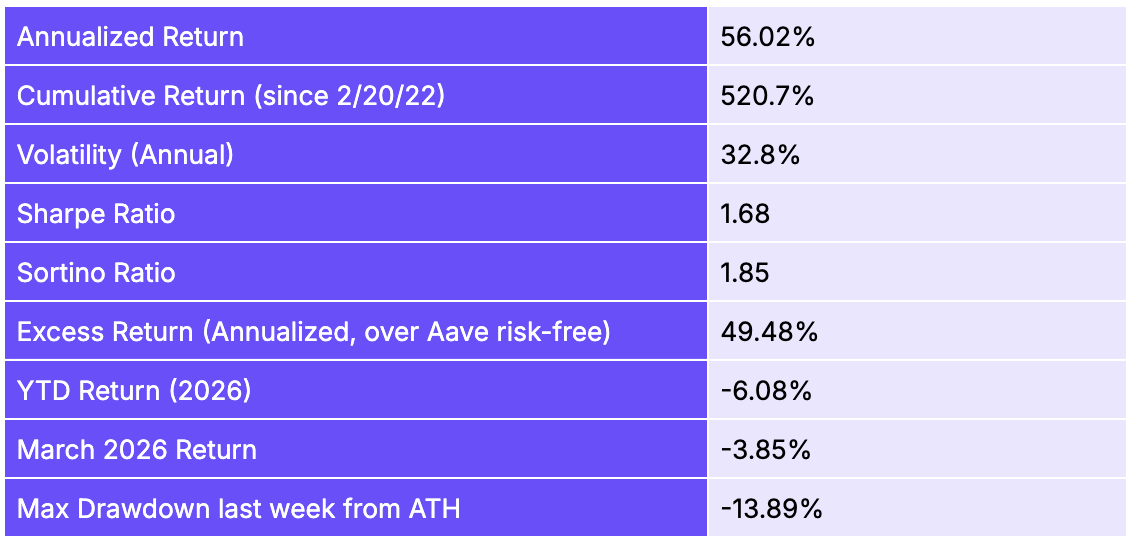

All metrics are calculated from inception (Feb 20, 2022).

Despite the broad stagnation of the market, the multi-factor framework continues to demonstrate its value. Value was near-flat in March (+0.02% return) and remains the strongest YTD performer among the long-short factors at +10.33%. The long-short construction across all factors limited drawdowns relative to long-only crypto exposure.

Market Risk Factor

Construction

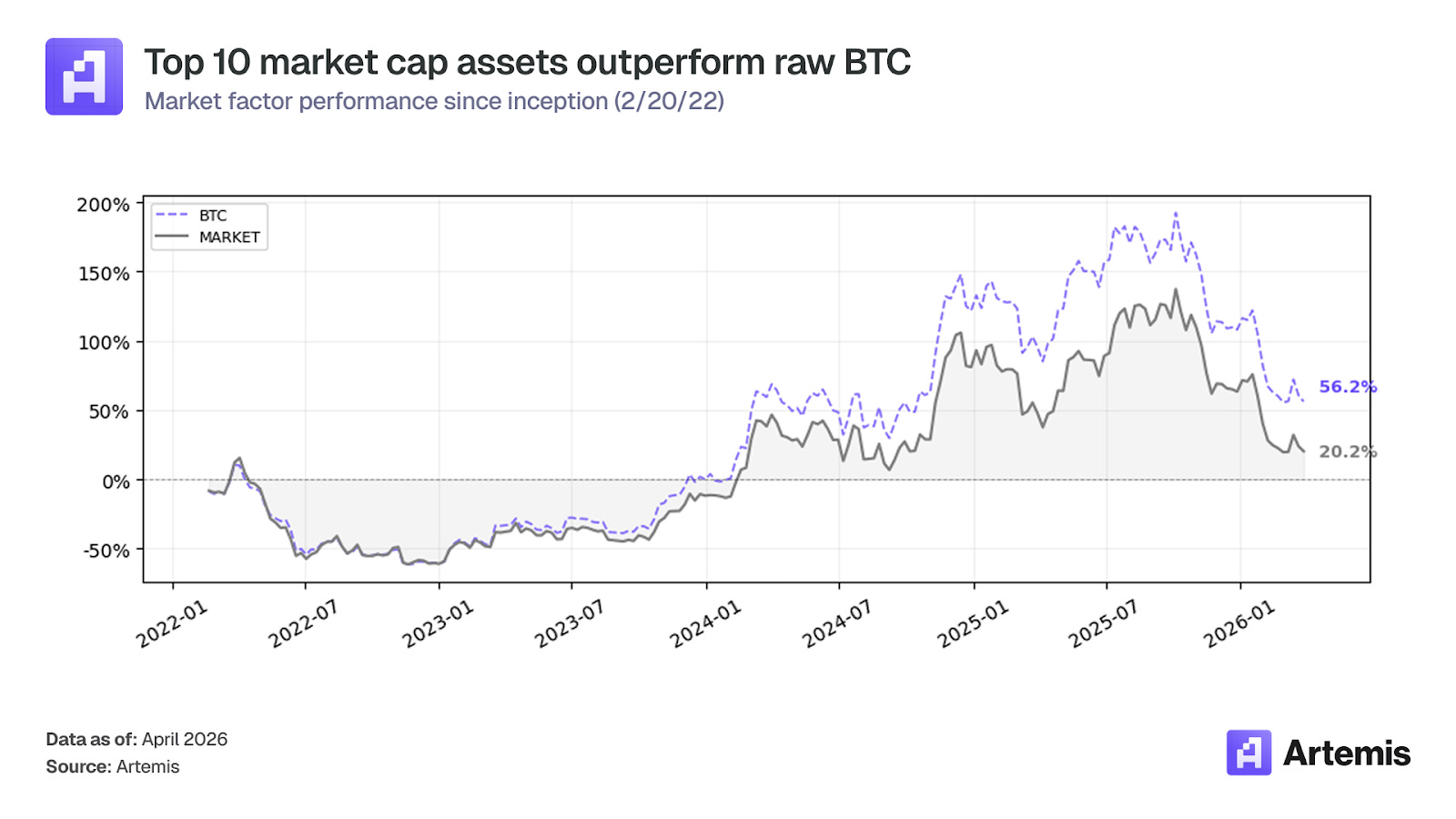

Long-only portfolio of the top 10 assets by market cap, market cap-weighted, rebalanced weekly. Captures broad crypto market exposure similar to a crypto index.

Current Holdings

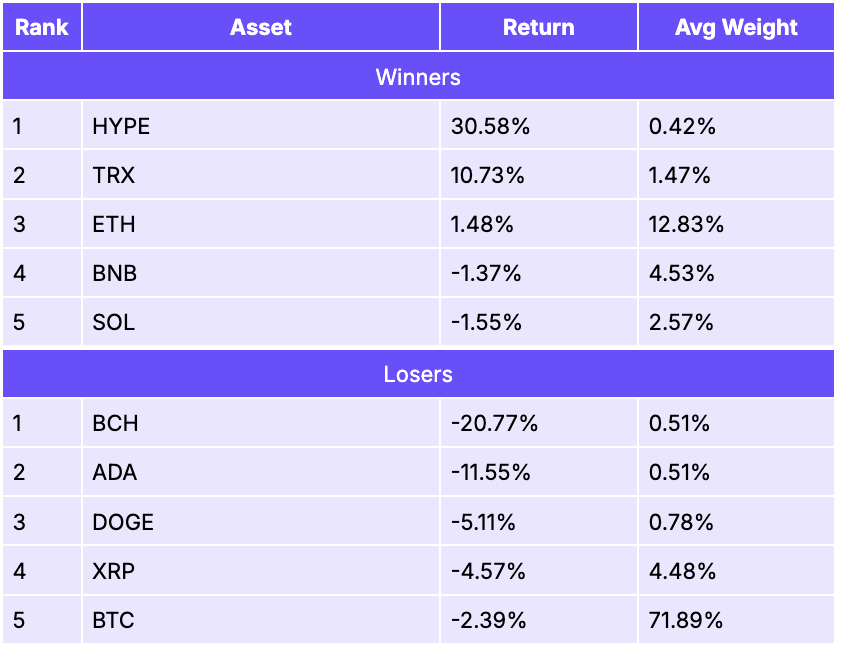

BTC (71.7%), ETH (13.0%), BNB (4.5%), XRP (4.4%), SOL (2.5%), TRX (1.7%), DOGE (0.8%), BCH (0.5%), HYPE (0.5%), ADA (0.5%)

Performance Metrics

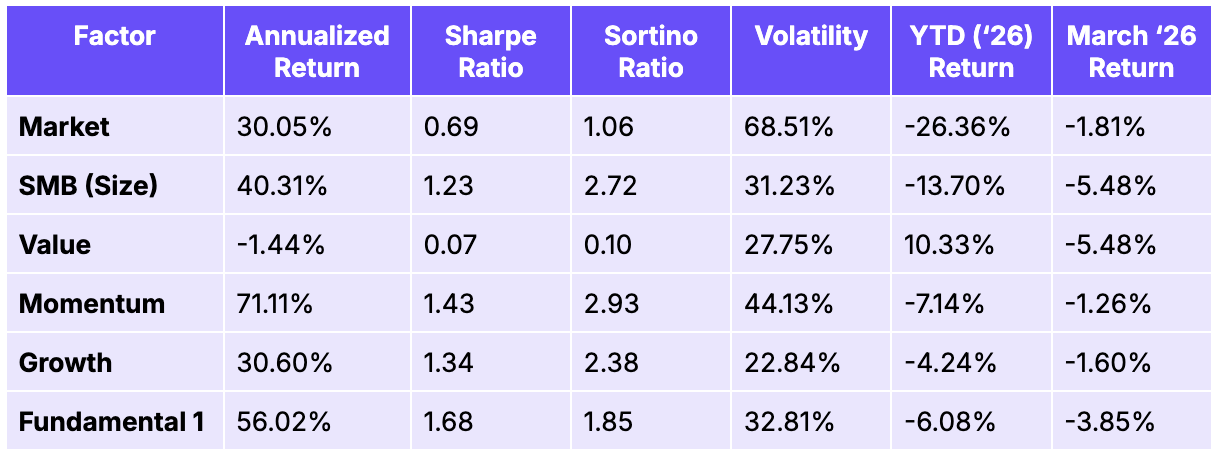

March was an uneventful month for the broad market factor, returning -1.81%. This was much less severe than February’s -23.49% drawdown, but the market remains -49.33% below its all-time high, and YTD losses stand at -26.36%. BTC continues to dominate the portfolio composition at 71.89% weight and its -2.39% return was the primary driver of the monthly decline.

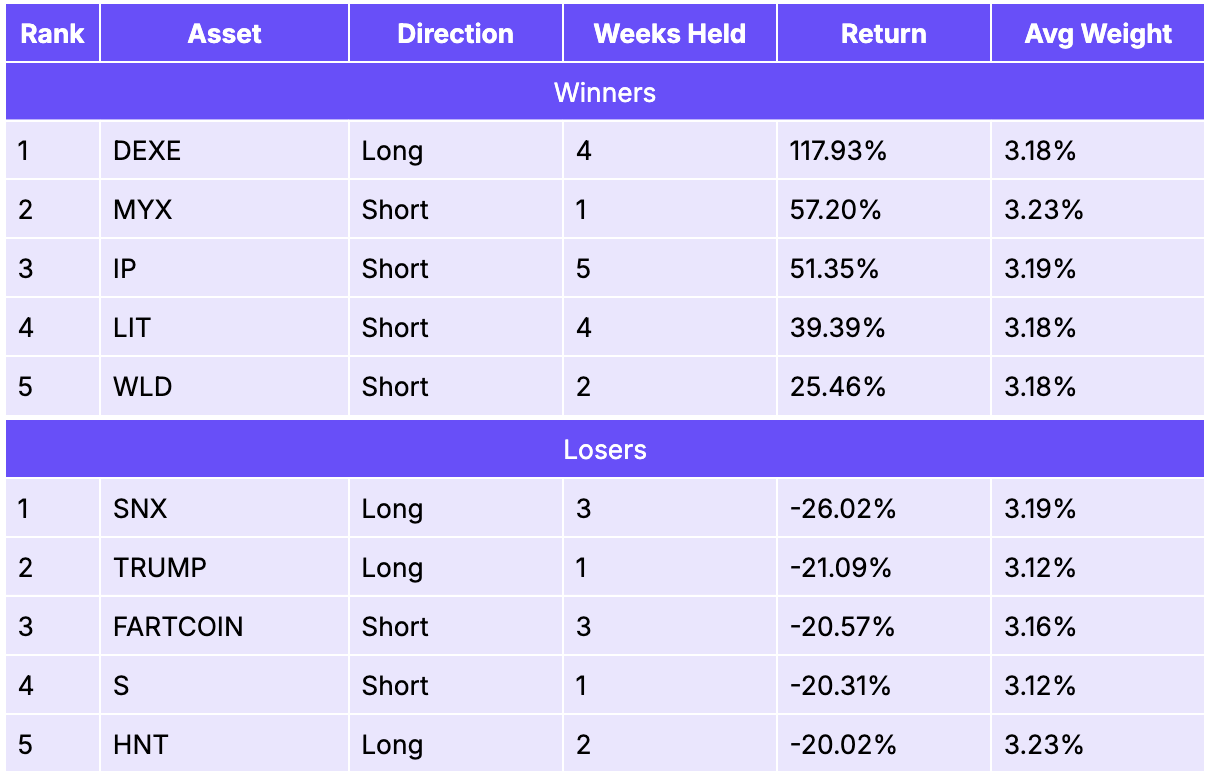

Top 5 Winners & Losers for March

HYPE was the standout performer at +30.58%, building on momentum of the exchange’s growing volumes and ecosystem expansion. TRX (+10.73%) continued to benefit from the stablecoin narrative as a primary rail for USDT transfers. ETH was essentially flat at +1.48%. On the losing side, BCH (-20.77%) led declines followed by ADA (-11.55%) and DOGE (-5.11%). Every asset in the top 5 losers is a long-only holding and losses were concentrated in the smaller-weight assets. BTC was the 5th largest loser, but at 71.89% weight, was the dominant contributor to the overall negative return.

Size Factor

Construction

Equal-weighted long-short factor: long the smallest 50% of eligible assets by market cap, short the largest 50%. Minimum 40 assets (20 per leg). Breakpoint: 50th percentile of market cap.

Performance Metrics

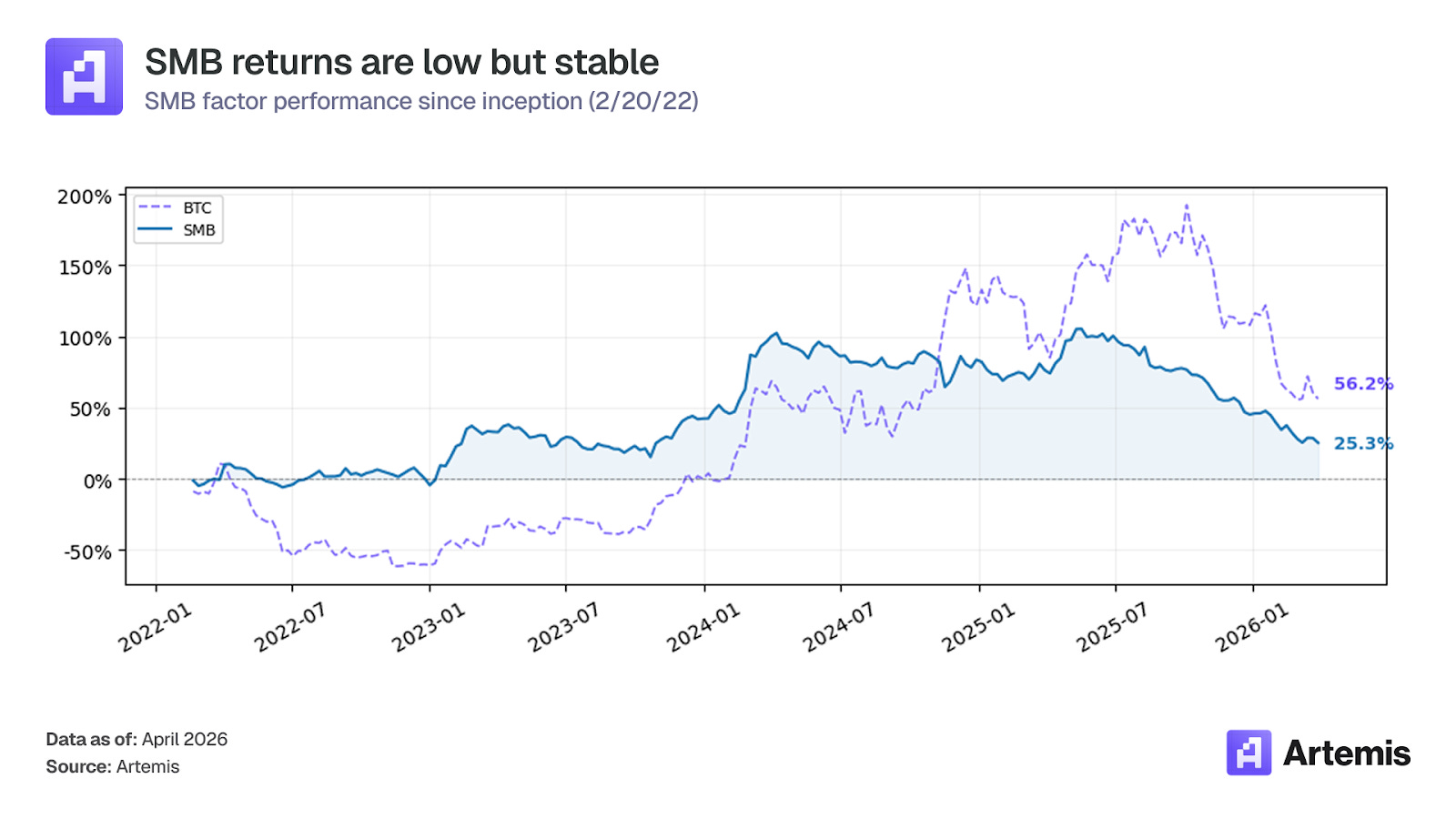

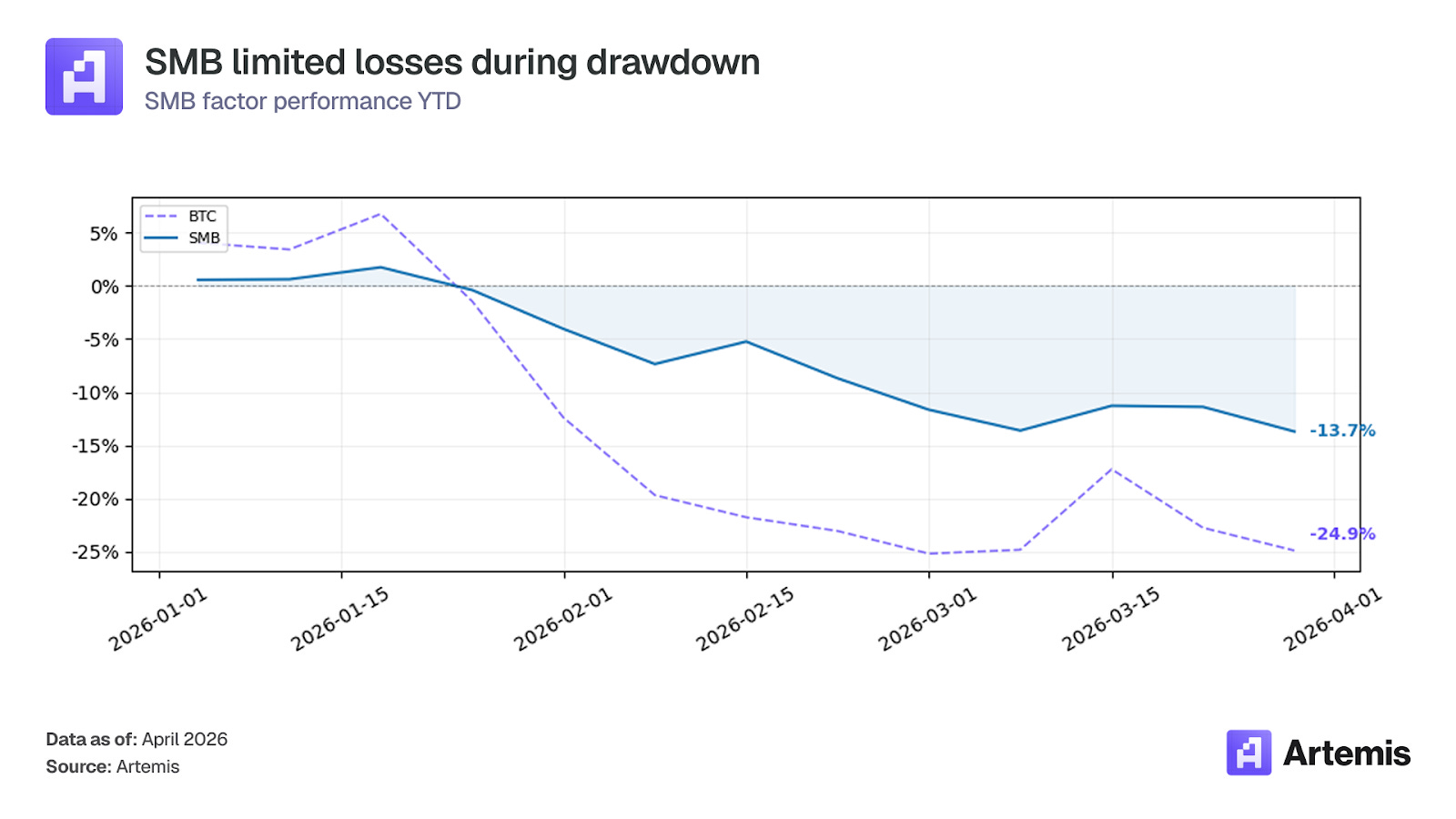

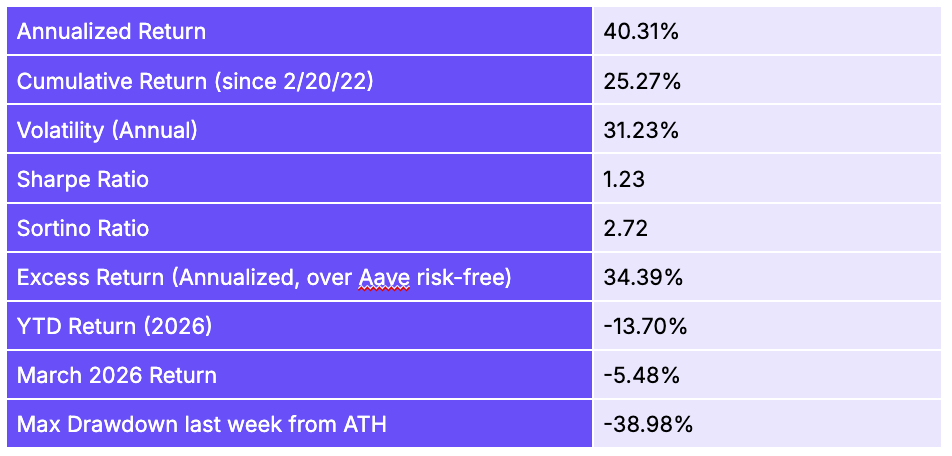

SMB returned -5.48% in March, making it the worst performing long-short factor for the month. YTD losses are now -13.70% and the max drawdown deepened to -38.98%. The continued underperformance of small caps relative to large caps is consistent with a risk-off environment where liquidity-driven selloffs hurt smaller, less liquid assets more. However, the factor’s annualized return of 40.31% and Sortino ratio of 2.72 indicate the size premium still remains over the full sample.

Top 5 Winners & Losers for March

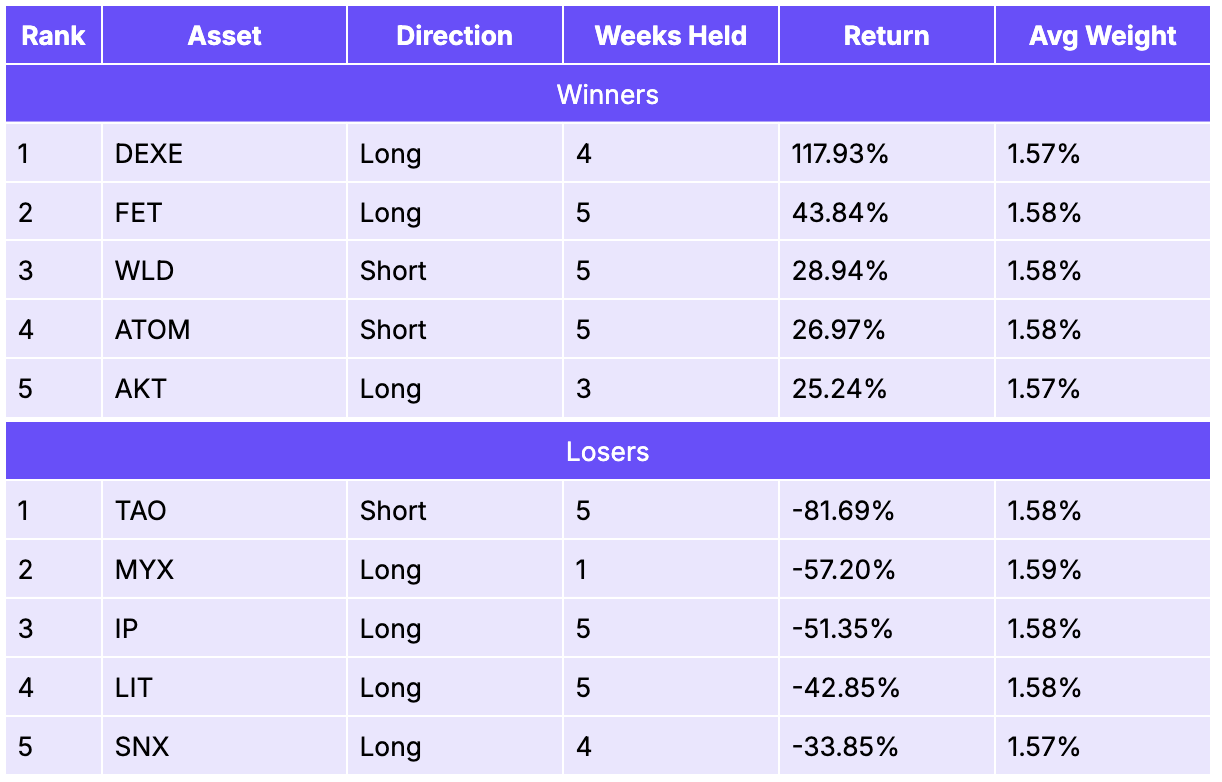

DEXE (+117.93% as a long) was by far the top contributor, driven by a surge in its governance token demand and staking activity. FET (+43.84% as a long) benefited from continued AI narrative momentum. WLD (+28.94% as a short) and ATOM (+26.97% as a short) contributed as short winners, reflecting weakness in large-cap infrastructure and interoperability tokens. On the losing side, TAO (-81.69% as a short) was the largest loss as the AI-focused token rallied sharply in March. MYX (-57.20% as a long) continued its trend from last month as a volatile position across factors. IP (-51.35% as a long) fell as token unlocks scheduled for March created supply overhang concerns, but these unlocks were later delayed to August. Additionally, PIP Labs, the core development team behind Story Protocol, reduced its staff by about 10% in early March 2026 as part of a broader wave of crypto layoffs. LIT (-42.85% as a long) is a low-liquidity micro-cap that gets pushed around by broad market moves, so was hurt by the general risk-off sentiment in March.

Value Factor

Construction

Equal-weighted long-short: long assets with the lowest Market Cap / Fees ratio (highest fundamental value), short assets with the highest MC / Fees ratio (most expensive). Minimum 30 assets (15 per leg).

Performance Metrics

Value was effectively flat in March, returning +0.02%. Despite this, the factor still has the best risk profile of all factors with a max drawdown of just -1.26% and YTD return of +10.33%. This continues from the pattern last month where Value benefits from risk-off environments as the speculative, expensive assets in the short leg sell off, offsetting any weakness in fundamentally cheap long positions.

Top 5 Winners & Losers for March

The short leg benefited from continued declines in overvalued tokens like IP (+38.30% as a short), which fell amid token unlock fears and a 10% staff reduction at its core dev team PIP Labs, and WLD (28.94% as a short) and ATOM (26.97% as a short), which continued to sell off as large-cap infrastructure tokens lost favor in the risk-off environment. Meanwhile, the long leg was dragged down by the broader DeFi selloff: MYX collapsed on thin liquidity, LIT (-42.85% as a long) continued its decline as a micro-cap token in the midst of a rebrand with negligible trading volume, and HNT (-24.14% as a long) and INJ (-20.26% as a long) fell alongside the broader altcoin drawdown driven by the Iran war shock and hawkish Fed hold.

Momentum Factor

Construction

Volatility-adjusted momentum: calculates 3-week rolling Sharpe-like score (mean return / std dev of daily return) for each asset. Long top 25% by filtered momentum, short bottom 25%. Equal-weighted, minimum 30 assets (15 per leg).

Performance Metrics

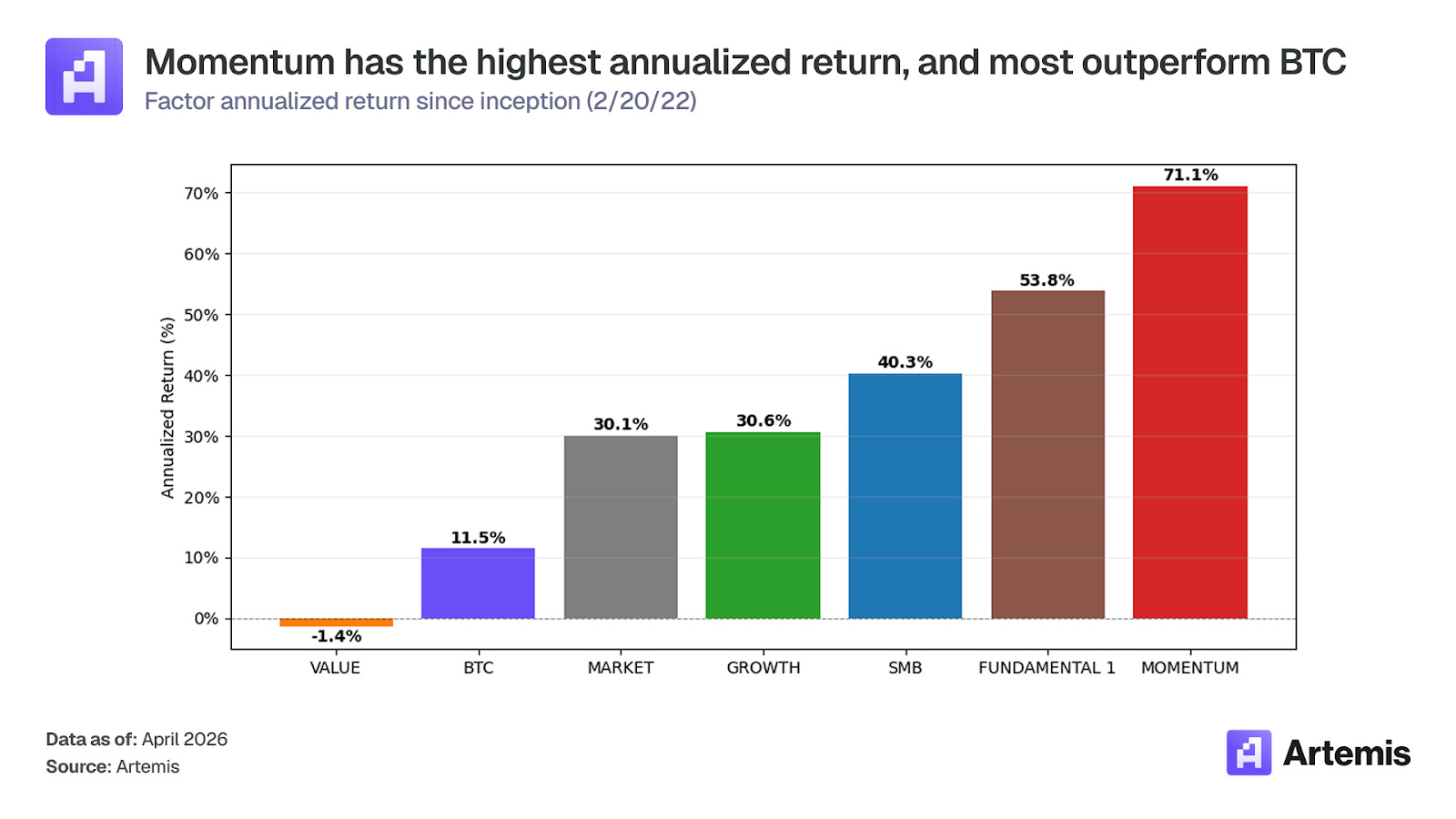

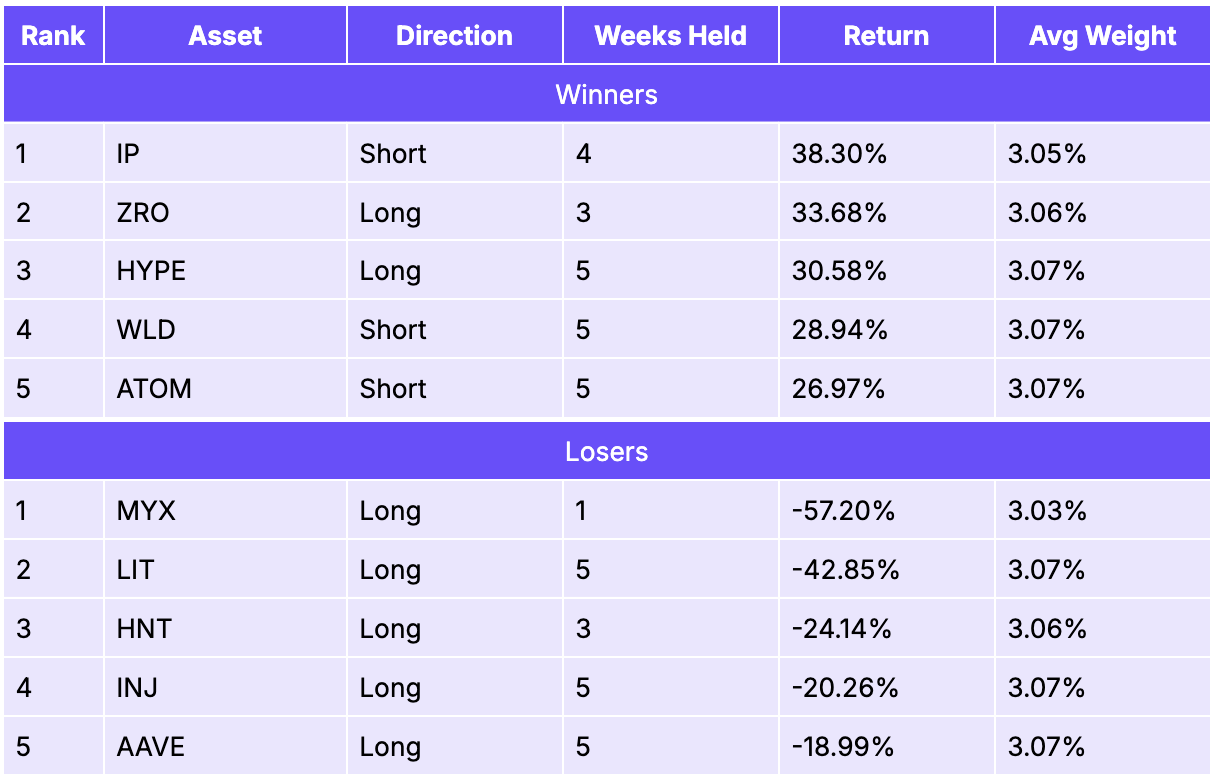

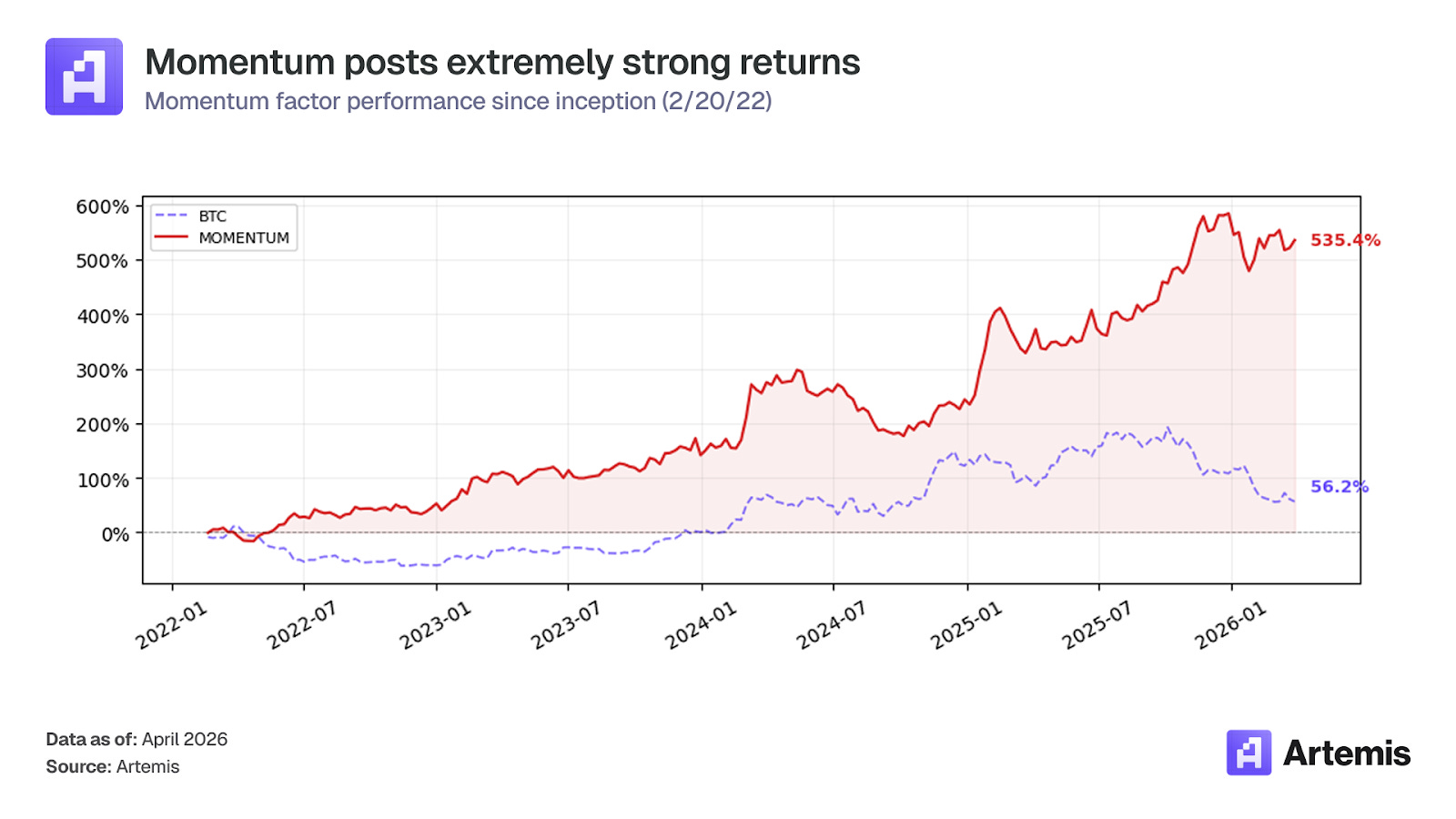

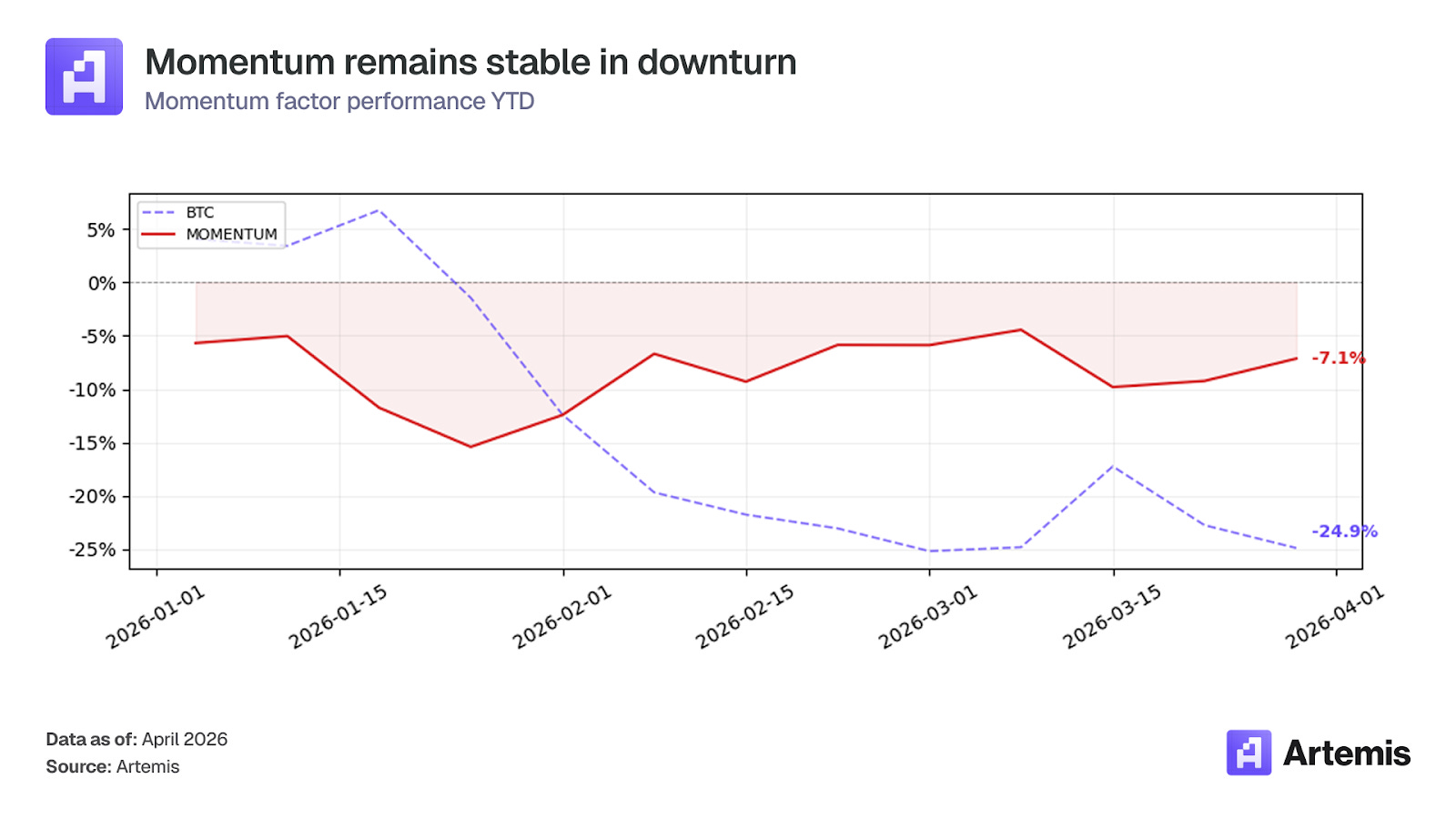

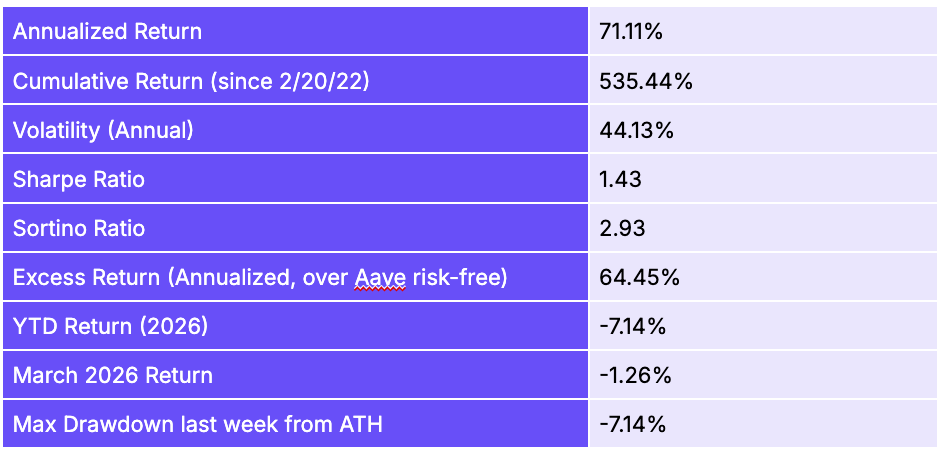

Momentum returned -1.26% in March, a reversal from February’s strong +11.27%. The factor’s YTD loss is -7.14% and the max drawdown from ATH is -7.14%. The negative monthly return reflects that trend persistence was less rewarded and reversals in positions offset gains in the short leg. Despite the underperformance this month, the factor still has the highest annualized return (71.11%) and a Sharpe ratio of 1.43 since inception.

Top 5 Winners & Losers for March

DEXE (+117.93% as a long) was the top contributor, with the momentum signal correctly identifying its strong uptrend. MYX (+57.20% as a short) was the second-best performer, with the factor correctly shorting the token as it continued to decline. IP (+51.35% as a short) and LIT (+39.39% as a short) also contributed as short winners. On the losing side, SNX (-26.02% as a long) was the biggest loss as the token initially had positive momentum that reversed sharply. TRUMP (-21.09% as a long) also hurt, entering the portfolio on a brief momentum signal before declining. FARTCOIN (-20.57% as a short) and S (-20.31% as a short) were short losers that rallied against the factor’s positioning, while HNT (-20.02% as a long) pulled back after its strong February performance.

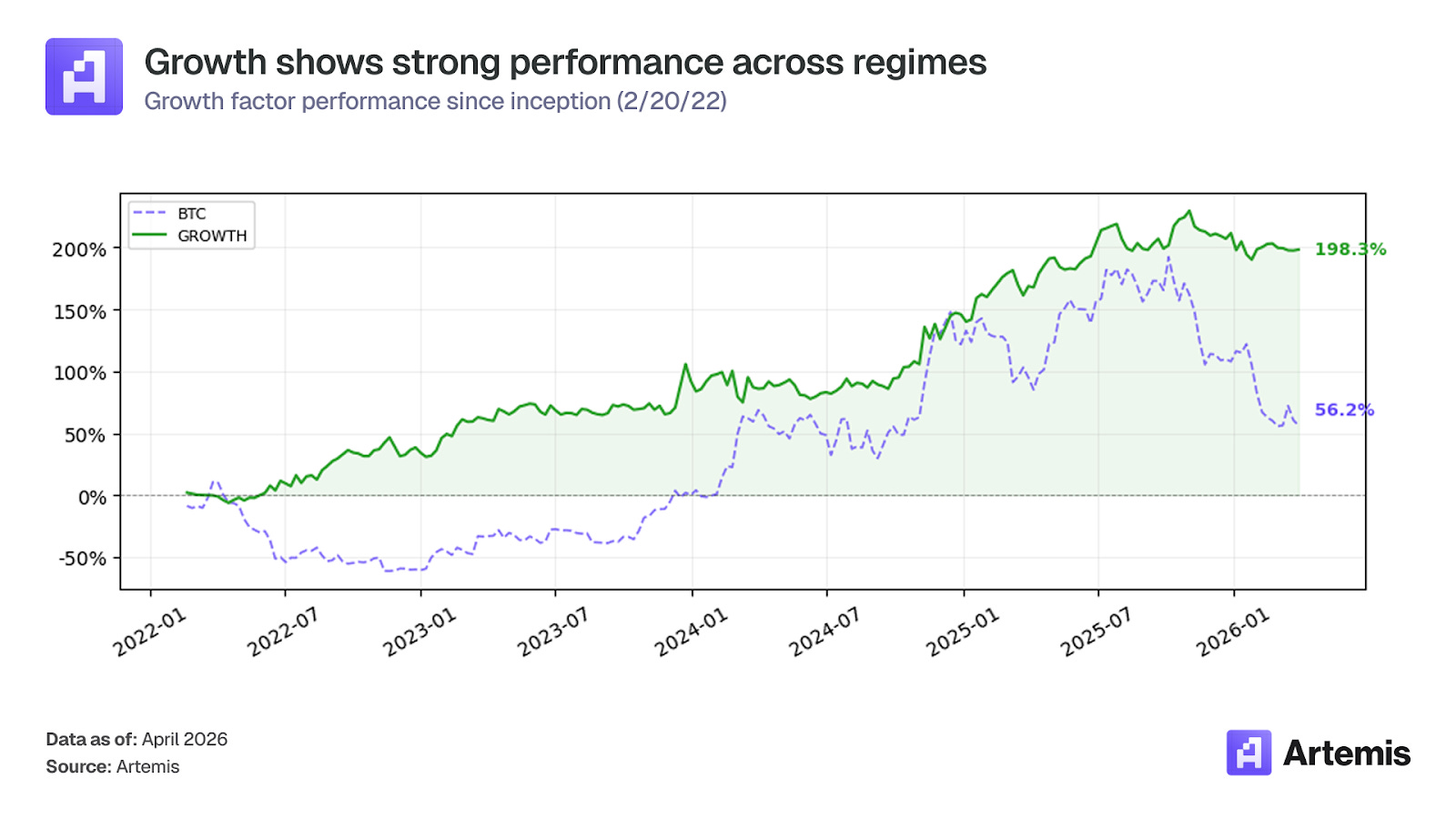

Growth

Construction

Equal-weighted long-short: composite score combining z-scores of 2-week trailing fee growth (pct change) and DAU growth (pct change). Long top 50% composite score, short bottom 50%. Eligibility requires DAU > 100 and weekly fees > $500. 30 assets (15 per leg).

Performance Metrics

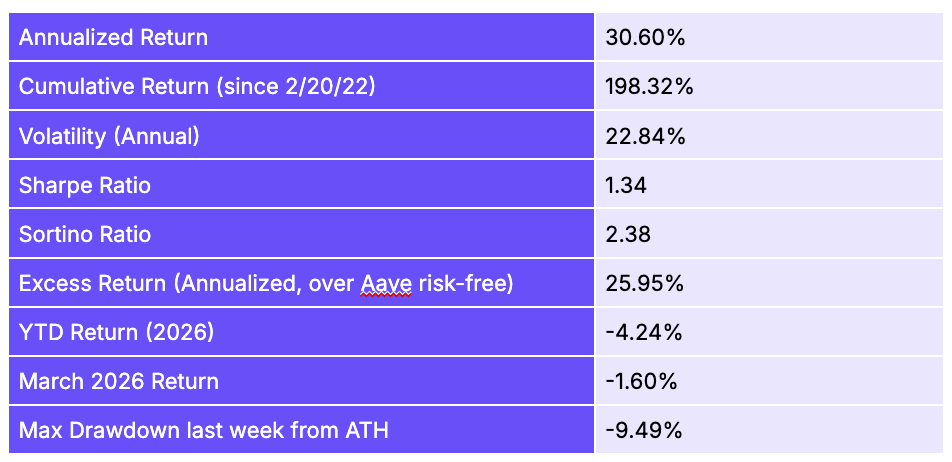

Growth returned -1.60% in March, bringing its YTD return to -4.24%. This factor continues to exhibit the lowest volatility of the long-short factors at 22.84% annualized. The negative monthly return reflects fundamental growth signals (fee growth and DAU growth) providing less differentiation between assets as the market unease compressed factor spreads.

Top 5 Winners & Losers for March

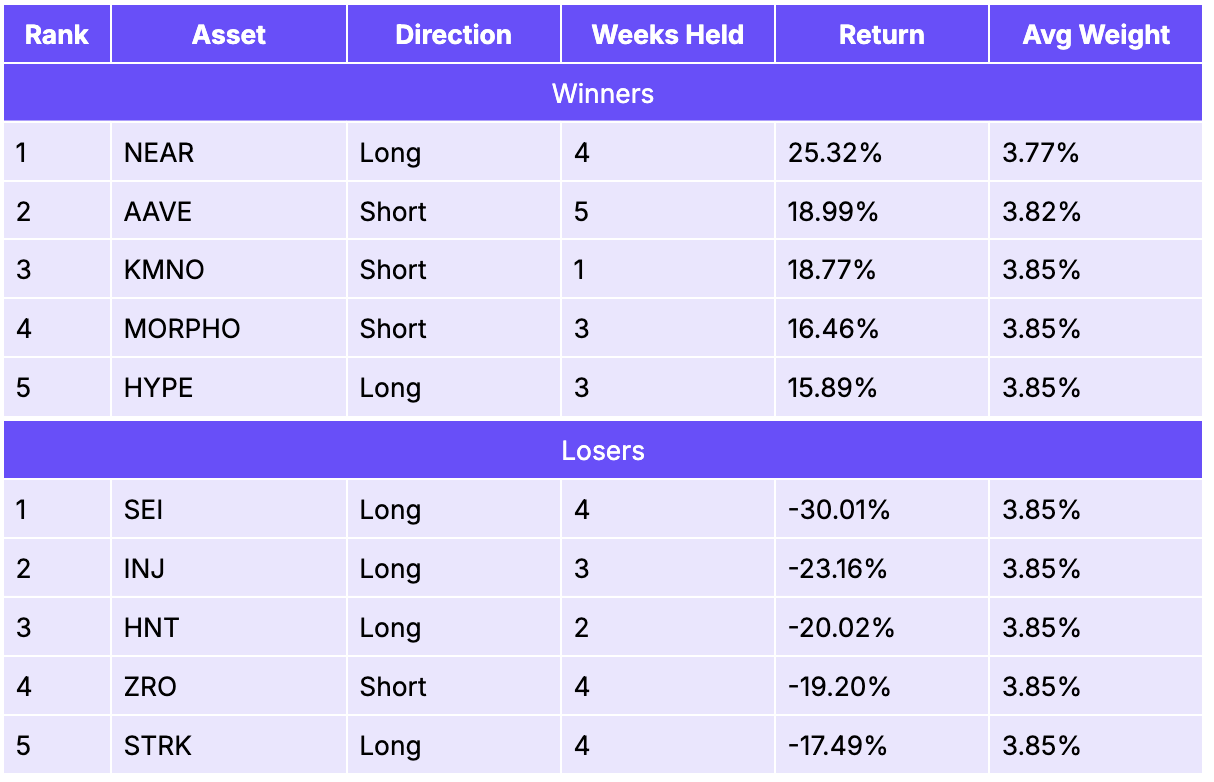

NEAR (+25.32% as a long) was the top contributor, with the growth signal correctly identifying accelerating on-chain activity. NEAR benefited from the AI narrative momentum as on March 3, co-founder Illia Polosukhin shared a vision of NEAR enabling AI agents on the blockchain and the protocol released a privacy upgrade called “Confidential Intents”. AAVE (+18.99% as a short) contributed as a short winner following an unusual liquidation event on March 10 due to a configuration problem in CAPO and broad DeFi selloff due to a hawkish Fed and the Iran War. KMNO (+18.77% as a short) and MORPHO (+16.46% as a short) also contributed from the short leg as part of the DeFi sell-off. HYPE (+15.89% as a long) confirmed its strong growth profile. On the losing side, SEI (-30.01% as a long) was the largest loser despite screening for positive growth metrics; it declined sharply alongside broader L2 weakness. ZRO (-19.20% as a short) was the most notable short loser as the price rallied following an announcement of its own Layer-1 blockchain backed by Citadel Securities, ARK Invest, and Google Cloud.

Fundamentals 1

Construction

Equal-weighted long-short quintile portfolio: composite score combining rank z-scores of DAU growth, inverted active revenue share, revenue stability, and MC/fees mean reversion. Long top quintile (~12 assets), short bottom quintile (~12 assets).

Performance Metrics

Fundamentals 1 returned -3.85% in March, bringing its YTD to -6.08%. Despite the difficult month, the factor retains the highest Sharpe ratio (1.68) and second-highest annualized return (56.0%) of any factor since inception. The max drawdown from ATH deepened to -13.89%, reflecting that the factor was actively exposed to the market throughout March. The factor’s composite signal, which combines DAU growth, revenue quality, revenue stability, and valuation mean reversion, struggled to generate positive spread in a month where geopolitical shocks overwhelmed fundamental differentiation.

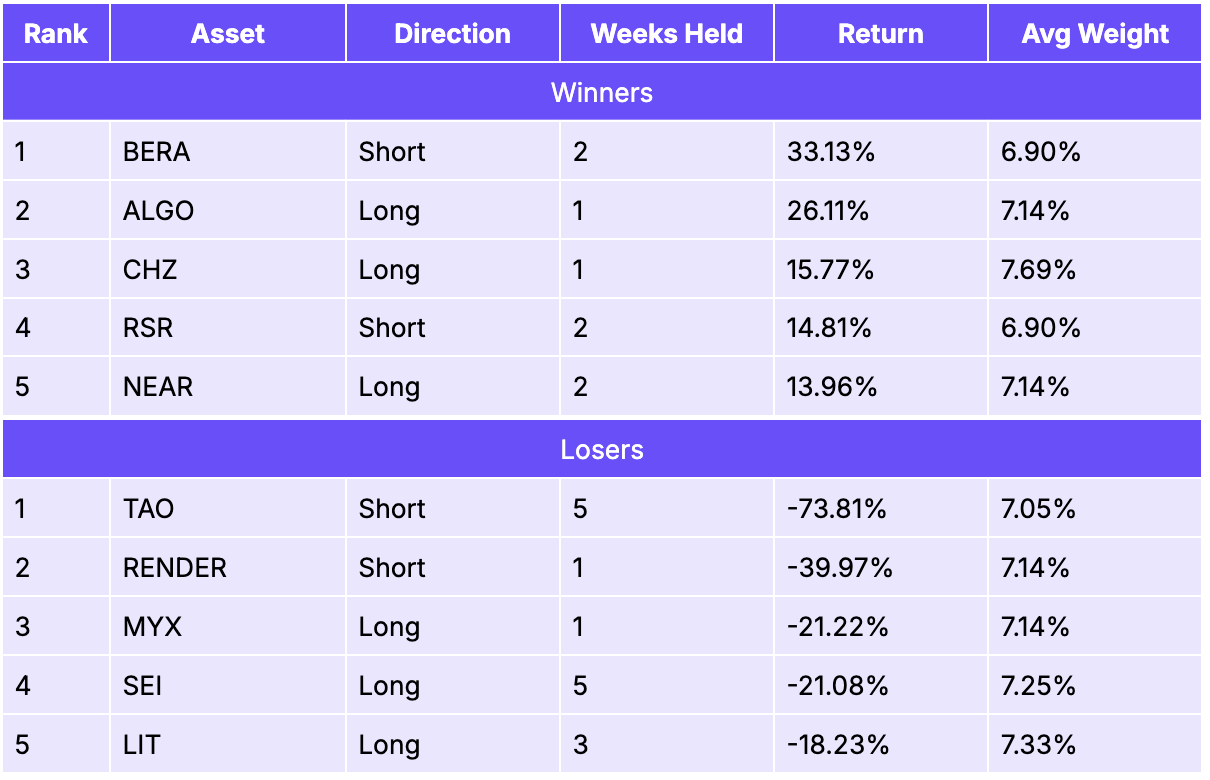

BERA (+33.13% as a short) was the top contributor to returns. Berachain is now trading 97% below its all-time high as its Proof-of-Liquidity model has struggled to generate sustained demand, and the risk-off environment accelerated the selloff. ALGO (+26.11% as a long) rallied after the SEC declared it a digital commodity, resolving years of regulatory uncertainty. CHZ (+15.77% as a long) benefited from momentum around the 2026 FIFA World Cup as Chiliz released its roadmap targeting omnichain fan tokens and CHZ buybacks. RSR (+14.81% as a short) continued to slide amid low adoption and broader altcoin weakness. NEAR (+13.96% as a long) was lifted by the AI narrative after its “Confidential Intents” launch and co-founder Illia Polosukhin’s vision of NEAR as infrastructure for AI agents. On the losing side, TAO (-73.81% as a short) was by far the largest loser as the AI narrative rallied. RENDER (-39.97% as a short) similarly rallied on the decentralized GPU computing narrative. MYX (-21.22% as a long) collapsed on thin liquidity, SEI (-21.08% as a long) declined alongside broader L1 weakness despite positive fundamental scores, and LIT (-18.23% as a long) fell as a micro-cap with negligible volume in the midst of rebranding to Heima.

Key Findings & Conclusion

March was a quiet month for crypto factor strategies, with the market returning -1.81% and no long-short factor generating meaningful positive returns. Factor spreads compressed as the Iran war shock drove correlated moves across assets, making it difficult for relative value signals to differentiate winners from losers.

Value continued to demonstrate its defensive properties, returning +0.02% and maintaining one of the lowest max drawdowns from ATH (-1.26%) across the factors. While the remaining long-short factors all posted negative returns in March, the YTD picture shows their value: the market factor is down -26.36% and BTC is down -24.9%, but Growth (-4.24%), Momentum (-7.14%), and Fundamentals 1 (-6.08%) have all significantly limited losses relative to passive crypto exposure. Even SMB, the worst-performing factor YTD at -13.70%, has cut the market’s drawdown roughly in half.

A few cross-factor themes stood out in March. The AI narrative drove selective strength: NEAR rallied on its Confidential Intents launch and AI agent vision, while TAO surged sharply, punishing short positions in multiple factors. DeFi lending was broadly weak: AAVE fell after a CAPO oracle misconfiguration triggered unusual liquidations, and both KMNO and MORPHO declined on token unlock pressure and the broader sector selloff. DEXE was the strongest single asset across the factor universe at +117.93%, appearing as the top contributor in both SMB and Momentum. Meanwhile, ZRO (LayerZero) showed how different signals can diverge on the same token: it rallied after announcing its own L1 blockchain backed by Citadel, ARK Invest, and Google Cloud, making it a winner in Value (correctly long) but a loser in Growth (incorrectly short).

In a month where broad crypto exposure lost -1.81% and the S&P 500 fell over 7%, the long-short factor framework limited losses across the board. The framework’s value is clearest in cumulative YTD numbers: while the market factor is down -26.36%, Value is up +10.33%.

If you have any questions, feel free to reach out to team@artemis.xyz or shoot us a DM on X.com at https://x.com/artemis

Disclosure: This material is provided for informational purposes only and does not constitute investment advice, financial advice, trading advice, or any other form of advice. The views expressed are those of the authors and should not be relied upon as a recommendation to buy, sell, or hold any asset. The authors or affiliated entities may hold positions in the assets discussed. You should conduct your own research and consult appropriate financial professionals before making any investment decisions.

| A guest post by

|